AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 981:

Capital budgeting decisions include all but which of the following?

A. Selecting among long-term investment alternatives. B. Financing short-term working capital needs. C. Making investments that produce returns over a long period of time. D. Financing large expenditures.

B. Financing short-term working capital needs. Choice "b" is correct. Capital budgeting decisions do not include the financing of short-term working capital needs, which are more operational in nature. Choices "a", "c", and "d" are incorrect, as these are all types of capital budgeting decisions.

Question 982:

An auditor's program to examine long-term debt should include steps that require:

A. Examining bond trust indentures. B. Inspecting the accounts payable subsidiary ledger. C. Investigating credits to the bond interest income account. D. Verifying the existence of the bondholders.

A. Examining bond trust indentures. Choice "a" is correct. Examination of bond trust indentures should be included in audit program of longterm debt to assure that the client was not in violation of any covenants in the indentures. Choice "b" is incorrect. Inspecting the accounts payable subsidiary ledger relates to accounts payable, a current liability. Choice "c" is incorrect. Long-term debt generates interest expense, not interest income. Choice "d" is incorrect. Generally, the existence of the bondholders of debt is not verified.

Question 983:

Which of the following is not a required procedure in an engagement to review the interim financial information of a publicly held entity?

A. Obtaining corroborating evidence about the entity's ability to continue as a going concern. B. Comparing disaggregated revenue data for the current interim period with that of comparable prior periods. C. Obtaining evidence that the interim financial information reconciles with the accounting records. D. Inquiring of management about their knowledge of fraud or suspected fraud.

A. Obtaining corroborating evidence about the entity's ability to continue as a going concern. Choice "a" is correct. A review of interim financial information is not designed to provide information regarding an entity's ability to continue as a going concern. Even if such information comes to the accountant's attention, the accountant is not required to corroborate it. Choice "b" is incorrect. As part of a review, the accountant is required to compare disaggregated revenue data for the current interim period with that of comparable prior periods. Choice "c" is incorrect. As part of a review, the accountant is required to obtain evidence that the interim financial information reconciles with the accounting records. Choice "d" is incorrect. As part of a review, the accountant is required to inquire of management about their knowledge of fraud, suspected fraud, or allegations of fraud.

Question 984:

The scope of an audit is not restricted when an attorney's response to an auditor as a result of a client's letter of audit inquiry limits the response to:

A. Matters to which the attorney has given substantive attention in the form of legal representation. B. An evaluation of the likelihood of an unfavorable outcome of the matters disclosed by the entity. C. The attorney's opinion of the entity's historical experience in recent similar litigation. D. The probable outcome of asserted claims and pending or threatened litigation.

A. Matters to which the attorney has given substantive attention in the form of legal representation. Choice "a" is correct. The scope of an audit is not restricted when an attorney's response is limited to matters to which the attorney has given substantive attention in the form of legal representation. The attorney may also limit his or her response to matters that are considered individually or collectively to be material. Choices "b", "c", and "d" are incorrect. The scope of an audit may be restricted when an attorney's response is limited to: 1. An evaluation of the likelihood of an unfavorable outcome of the matter disclosed by the entity. (The attorney's response should also address the nature of the claim, the progress to date, and the intended response.) 2. The attorney's opinion of the entity's historical experience in recent similar litigation. (The attorney's response should address the current situation, which may not parallel historical experience). 3. The probable outcome of asserted claims and pending or threatened litigation. (The attorney's response should also address the nature of the claim, the progress to date, and the intended response, as well as unasserted claims).

Question 985:

ABC Products has announced that it plans to finance future investments so that the firm will achieve an optimum capital structure. Which one of the following corporate objectives is consistent with the announcement?

A. Maximize earnings per share. B. Minimize the cost of debt. C. Maximize the net worth of the firm. D. Minimize the cost of equity.

C. Maximize the net worth of the firm. Choice "c" is correct. The optimal capital structure is the financial structure that would theoretically maximize shareholder wealth by maximizing the net worth of the company. Choices "a", "b", and "d" are incorrect. Strategies (not objectives) for creating an optimal capital structure to maximize net worth include: 1. Maximizing earnings per share (choice "a"). 2. Minimizing the cost of debt (choice "b"). 3. Minimizing the cost of equity (choice "d"). 4. Maximizing cash flow (choice not given).

Question 986:

Davidson, CPA, is performing a review under auditing standards of Gold's interim financial information. As part of planning, Davidson reads the audit documentation from the preceding year's annual audit. Which of the following is least likely to affect Davidson's review?

A. A summary of both corrected and uncorrected misstatements. B. Identified risks of material misstatement due to fraud. C. Significant weaknesses in internal control. D. Scope limitations that were overcome through acceptable alternative procedures.

D. Scope limitations that were overcome through acceptable alternative procedures. Choice "d" is correct. Scope limitations relate to problems in performing the audit, and, especially since they were overcome, they would bear little relationship to procedures performed in a review. Choice "a" is incorrect. The nature of corrected misstatements should be considered, as they may be indicative of an ongoing problem. Uncorrected misstatements must also be considered as misstatements in one period often affect subsequent periods. Choice "b" is incorrect. Identified risks of material misstatement due to fraud help the accountant to identify the types of material misstatements that may occur in the interim financial information, and to consider the likelihood of their occurrence. Choice "c" is incorrect. Consideration of significant weaknesses in internal control helps the accountant identify the types of material misstatements that may occur in the interim financial information, and to consider the likelihood of their occurrence.

Question 987:

All of the following are complementary goods, except:

A. Margarine and butter. B. Gas and motor oil. C. Cameras and rolls of film. D. VCRs and video cassettes.

A. Margarine and butter. Choice "a" is correct. Margarine and butter are substitute goods. If the price of one goes up, demand for the substitute increases. Choices "b", "c", and "d" are incorrect. They are complements. Two goods are complements if they are used together or their demand curves move together (breakfast cereal and milk, e.g., or tennis balls and tennis racquets). Thus, if the price of one complement goes up, demand for the other good goes down.

Question 988:

Which one of the following will result in an accruable expense for an accrual-basis taxpayer?

A. An invoice dated prior to year end but the repair completed after year end. B. A repair completed prior to year end but not invoiced. C. A repair completed prior to year end and paid upon completion. D. A signed contract for repair work to be done and the work is to be completed at a later date.

B. A repair completed prior to year end but not invoiced. RULE: An accruable expense is one that the services have been received/performed but have not been paid for by the end of the reporting period. Choice "b" is correct. The facts indicate that a repair was completed prior to year end but not yet invoiced. If it has not yet been invoiced, it is assumed that it has also not yet been paid for. Therefore, this is a situation in which the repair expense would be accrued at year end. Services have been performed, but they have not been paid for, as they have not even been invoiced yet. Choice "a" is incorrect. If the repair was completed after year end, then the expense is not accruable, as the benefit of the services hasn't been received as of year end. The fact that the repair was invoiced prior to year end does not impact the situation. Choice "c" is incorrect. If a repair was completed and paid for prior to year end, no accrual is appropriate. On the accrual basis, the expense is taken in the year the repair is completed and the benefit is received. In this case, the account payable was also paid in the same year, but this has no effect on the expense. Choice "d" is incorrect. The facts indicate that the work is to be completed at a date later than year end. Therefore, the expense is not accruable at year end, as the benefit of the repair hasn't been received as of year end. It is reasonable that a signed contract for the repair work exists, but this has no effect on the accrual.

Question 989:

Karen Parker wants to establish an environmental testing company that would specialize in evaluating the quality of water found in rivers and streams. However, Parker has discovered that she needs either certification or approval from five

separate local and state government agencies before she can commence business. Also, the necessary equipment to begin would cost several million dollars. However, Parker believes that if she is able to obtain capital resources, she can

gain market share from the two major competitors.

The market structure Karen Parker is attempting to enter is best described as:

A. Pure competition. B. A natural monopoly. C. An oligopoly. D. Monopolistic competition.

C. An oligopoly. Choice "c" is correct. Major competitors and substantial capital requirements (high barriers to entry) are oligopolistic market conditions. Choice "a" is incorrect. Pure competition has small barriers to entry and numerous suppliers. Choice "b" is incorrect. A natural monopoly suggests that economic conditions allow only one supplier for efficiency purposes. Choice "d" is incorrect. Monopolistic competition has easier barriers to entry and more firms competing to supply the market than oligopoly.

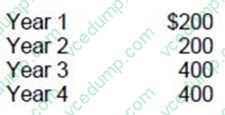

Question 990:

A project has an initial outlay of $1,000. The projected cash inflows are:

What is the investment's payback period?

A. 4.0 years. B. 3.5 years. C. 3.4 years. D. 3.0 years.

B. 3.5 years. Choice "b" is correct. The payback period is computed as the number of years required to fully recover the original investment without respect to the time value of money. With uneven cash flows, the payback period is computed by development of a cumulative payback balance converted to years as follows: Choice "a" is incorrect. Although the payback occurs in the fourth year, only half the year is required. The payback period is 3.5, not 4.0 years. Choice "c" is incorrect. Although the payback occurs in the fourth year, half the year is required. The payback period is 3.5, not 3.4 years. Choice "d" is incorrect. The payback occurs in the fourth year. The payback period is 3.5, not 3.0 years. Strategies for Short-term and Long-term Financing.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.