AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 851:

When there has been a change in accounting principles, but the effect of the change on the comparability of the financial statements is not material, the auditor should:

A. Refer to the change in an explanatory paragraph. B. Explicitly concur that the change is preferred. C. Not refer to consistency in the auditor's report. D. Refer to the change in the opinion paragraph.

C. Not refer to consistency in the auditor's report. Choice "c" is correct. If an accounting change has no material effect on the comparability of the financial statements, the auditor does not need to recognize the change in the current year's audit report. Choice "a" is incorrect. The change would only be referred to in an explanatory paragraph if the effect were material. Choice "b" is incorrect. The auditor does not explicitly concur with the change in the report. Choice "d" is incorrect. Even if the change had a material effect, the opinion paragraph would not be affected. The explanatory paragraph would follow the opinion paragraph.

Question 852:

In planning an audit of a new client, an auditor most likely would consider the methods used to process accounting information because such methods:

A. Influence the design of internal control. B. Affect the auditor's preliminary judgment about materiality levels. C. Assist in evaluating the planned audit objectives. D. Determine the auditor's acceptable level of audit risk.

A. Influence the design of internal control. Choice "a" is correct. The auditor should consider the methods the entity uses to process accounting information in planning the audit because such methods influence the design of internal control. The extent to which computer processing is used in significant accounting applications, as well as the complexity of the processing, may also influence the nature, timing, and extent of audit procedures. Choice "b" is incorrect. Materiality is a matter of professional judgment and is influenced by the auditor's perceptions of the needs of a reasonable person. It would not be affected by the methods used to process accounting information. Choice "c" is incorrect. The auditor develops specific audit objectives based on financial statement assertions. The methods used to process accounting information would not be relevant to the development of objectives. Choice "d" is incorrect. Audit risk is the risk that the auditor may unknowingly fail to modify the opinion on financial statements that are materially misstated. The acceptable level of audit risk is a matter of auditor judgment, but it would not be affected by the methods used to process accounting information.

Question 853:

Which of the following characteristics most likely would be indicative of check kiting?

A. High turnover of employees who have access to cash. B. Many large checks that are recorded on Mondays. C. Low average balance compared to high level of deposits. D. Frequent ATM checking account withdrawals.

C. Low average balance compared to high level of deposits. Choice "c" is correct. Kiting occurs when a check drawn on one bank is deposited in another bank and no record is made of the disbursement in the balance of the first bank. Frequent kiting may result in a high level of deposits coupled with a low average balance. Choice "a" is incorrect. High turnover of employees who have access to cash may be normal in certain industries, or it may be indicative of poor hiring policies, but it would not be indicative of check kiting. Choice "b" is incorrect. More checks may arrive on Mondays simply because Monday's mail includes the mail from over the weekend. This characteristic is not particularly indicative of check kiting. Choice "d" is incorrect. Frequent ATM checking account withdrawals indicate a frequent need for cash, but this situation is not particularly indicative of check kiting.

Question 854:

An internal auditor's work would most likely affect the nature, timing, and extent of an independent CPA's auditing procedures when the internal auditor's work relates to assertions about the:

A. Existence of contingencies. B. Valuation of intangible assets. C. Existence of fixed asset additions. D. Valuation of related party transactions.

C. Existence of fixed asset additions. Choice "c" is correct. In making judgments about the extent of the effect of the internal auditor's work on the auditor's procedures, the auditor considers the materiality of financial statement amounts, the risk of material misstatement of the assertions related to these financial statement amounts, and the degree of subjectivity involved in the evaluation of the audit evidence gathered in support of the assertions. As the degree of subjectivity increases, the need for the auditor to perform tests of the assertions increases. Testing the existence of fixed asset additions involves very little subjectivity, and thus work performed by the internal auditor may reduce the auditor's testing in this area. Choice "a" is incorrect. Testing the existence of contingencies involves much subjectivity, and should, therefore, be performed by the auditor. Choice "b" is incorrect. Testing the valuation of intangible assets involves much subjectivity, and should, therefore, be performed by the auditor. Choice "d" is incorrect. Testing the valuation of related party transactions involves much subjectivity, and should, therefore, be performed by the auditor.

Question 855:

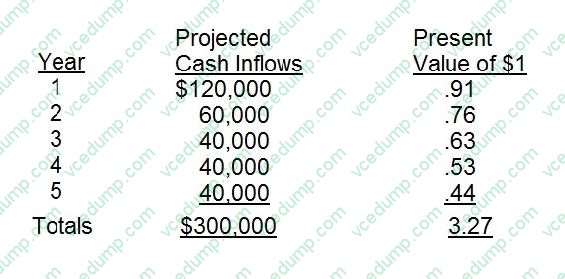

The ABC Company is planning a $200,000 equipment investment, which has an estimated five-year life with no estimated salvage value. The company has projected the following annual cash flows for the investment.

The net present value for the investment is:

A. $18,800 B. $196,200 C. $(3,800) D. $91,743

A. $18,800 Explanation Explanation/Reference:Choice "a" is correct. $18,800 net present value. The net present value of an investment is calculated as the present value of the cash inflows minus the present value of the cash outflows. In this case, there is only one cash outflow (at the purchase date), and that amount ($200,000) is already at present value (or, is multiplied by a present value factor of 1.0).

Question 856:

For a cash basis taxpayer, gain or loss on a year-end sale of listed stock arises on the:

A. Trade date. B. Settlement date. C. Date of receipt of cash proceeds. D. Date of delivery of stock certificate.

A. Trade date. Choice "a" is correct. Trade date. Gain or loss on a year-end sale of listed stock arises on the trade date. Rule: Whether on the cash or accrual method of accounting taxpayers who sell stock or securities on an established securities market must recognize gains and losses on the trade date, rather than on the settlement date. Choices "b", "c", and "d" are incorrect, per the above rule.

Question 857:

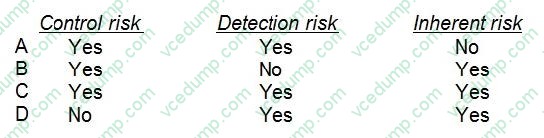

Which of the following risks may be assessed in nonquantitative terms?

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. Both the risk of material misstatement (including control risk and inherent risk) and detection risk may be assessed in quantitative terms such as percentages or in nonquantitative terms that range, for example, from a minimum to a maximum. Choices "a", "b", and "d" are incorrect, based on the above explanation.

Question 858:

Which of the following procedures would an auditor most likely perform in planning a financial statement audit?

A. Inquiring of the client's legal counsel concerning pending litigation. B. Comparing the financial statements to anticipated results. C. Examining computer generated exception reports to verify the effectiveness of internal controls. D. Searching for unauthorized transactions that may aid in detecting unrecorded liabilities.

B. Comparing the financial statements to anticipated results. Choice "b" is correct. A requirement during planning is to perform analytical procedures, which involve comparisons of recorded amounts to expectations. Choice "a" is incorrect. Inquiry of the client's legal counsel is typically performed near the end of fieldwork. Choice "c" is incorrect. Tests of controls are performed after audit planning is complete. Choice "d" is incorrect. The search for unrecorded liabilities is generally performed at or after year-end.

Question 859:

Which one of the following statements is most correct if a seller extends credit to a purchaser for a period of time longer than the purchaser's operating cycle? The seller:

A. Will have a lower level of accounts receivable than those companies whose credit period is shorter than the purchaser's operating cycle. B. Is, in effect, financing more than just the purchaser's inventory needs. C. Is, in effect, financing the purchaser's long-term assets. D. Has no need for a stated discount rate or credit period.

B. Is, in effect, financing more than just the purchaser's inventory needs. Choice "b" is correct. If a seller extends credit to a purchaser for a period of time longer than the purchaser's operating cycle, the seller is, in effect, financing more than just the purchaser's inventory needs. Choice "a" is incorrect. Accounts receivable would be higher than those companies whose credit period is shorter than the purchaser's operating cycle. Choice "c" is incorrect. Seller is financing the purchaser, but not necessarily long-term assets. Choice "d" is incorrect. It is appropriate for the seller to have stated policies for discount rate and credit periods.

Question 860:

An auditor would least likely initiate a discussion with those charged with governance concerning:

A. The methods used to account for significant unusual transactions. B. The maximum dollar amount of misstatements that could exist without causing the financial statements to be materially misstated. C. Indications of fraud and illegal acts committed by a corporate officer that were discovered by the auditor. D. Disagreements with management as to accounting principles that were resolved during the current year's audit.

B. The maximum dollar amount of misstatements that could exist without causing the financial statements to be materially misstated. Choice "b" is correct. The auditor's consideration of materiality is a matter of professional judgment and is influenced by the auditor's perception of the needs of a reasonable person who will rely on the financial statements. Materiality assessments are not typically discussed with those charged with governance. Choice "a" is incorrect. The auditor should communicate with those charged with governance about the appropriateness of significant accounting policies, such as the methods used to account for significant unusual transactions. Choice "c" is incorrect. The auditor should inform those charged with governance of illegal acts that come to the auditor's attention during the course of the audit. Fraud involving senior management should also be reported directly to those charged with governance. Choice "d" is incorrect. The auditor should discuss with those charged with governance any disagreements with management, whether or not they were satisfactorily resolved, about matters that individually or in the aggregate could be significant to the entity's financial statements or the auditor's report.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.