CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 771:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

In 1994, Joan received $1,300 in unemployment compensation benefits. Her employer made a $100 contribution to the unemployment insurance fund on her behalf.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 K. $10,000 L. $25,000 M. $50,000 N. $55,000 O. $75,000 -

Question 772:

At December 31, 1998, ABC Co. changed its method of accounting for demo costs from writing off the costs over two years to expensing the costs immediately. ABC made the change in recognition of an increasing number of demos placed with customers that did not result in sales. ABC had deferred demo costs of $500,000 at December 31, 1997, $300,000 of which were to be written off in 1998 and the remainder in 1999. ABC's income tax rate is 30%. In its 1998 financial

statements, what amount should ABC report as cumulative effect of change in accounting principle?

A. $0

B. $200,000

C. $350,000

D. $500,000 -

Question 773:

An increase in the quantity demanded for a product would be associated with a(n):

A. Increase in the price of a complementary product.

B. Increase in average household income.

C. Decrease in the price of that product.

D. Decrease in the price of a substitute product. -

Question 774:

The internal rate of return is the:

A. Rate of interest that equates the present value of cash outflows and the present value of cash inflows.

B. Risk-adjusted rate of return.

C. Required rate of return.

D. Weighted average rate of return generated by internal funds. -

Question 775:

The local video store's business increased by 12 percent after the movie theater raised its prices from $6.50 to $7.00. This is an example of:

A. Substitute goods.

B. Superior goods.

C. Complementary goods.

D. Independent goods. -

Question 776:

ABC Corp., a publicly-owned corporation, is subject to the requirements for segment reporting. In its income statement for the year ended December 31, 1991, ABC reported revenues of $50,000,000, operating expenses of $47,000,000, and

net income of $3,000,000. Operating expenses include payroll costs of $ 15,000,000. ABC's combined identifiable assets of all industry segments at December 31, 1991, were $40,000,000.

In its 1991 financial statements, ABC should disclose major customer data if sales to any single customer amount to at least:

A. $300,000

B. $1,500,000

C. $4,000,000

D. $5,000,000 -

Question 777:

Knox, president of ABC Corp., contracted with XYZ, Inc. to supply ABC's stationery on customary terms and at a cost less than that charged by any other supplier. Knox later informed ABC's board of directors that Knox was a majority stockholder in XYZ. Quick's contract with XYZ is:

A. Void because of Knox's self-dealing.

B. Void because the disclosure was made after execution of the contract.

C. Valid because of Knox's full disclosure.

D. Valid because the contract is fair to ABC. -

Question 778:

If information accompanying the basic financial statements in an auditor-submitted document has been subjected to auditing procedures, the auditor may include in the auditor's report on the financial statements an opinion that the accompanying information is fairly stated in:

A. Accordance with generally accepted auditing standards.

B. Conformity with generally accepted accounting principles.

C. All material respects in relation to the basic financial statements taken as a whole.

D. Accordance with attestation standards expressing a conclusion about management's assertions. -

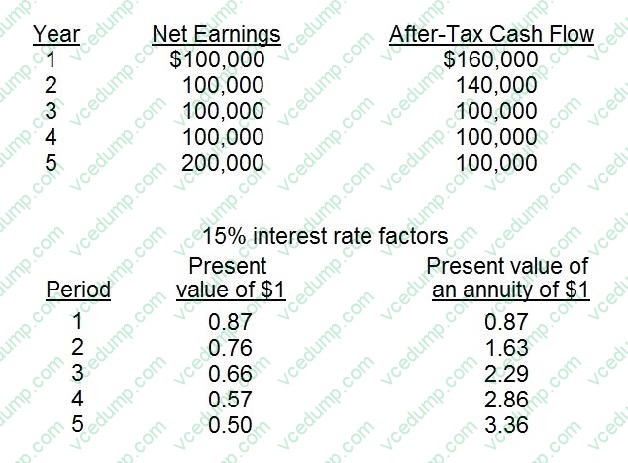

Question 779:

ABC, Inc. has a cost of capital of 15 percent and is considering the acquisition of a new machine, which costs $400,000 and has a useful life of five years. ABC projects that earnings and cash flow will increase as follows.

The net present value of this investment is:

A. Negative, $64,000

B. Negative, $14,000

C. Positive, $18,600

D. Positive, $200,000 -

Question 780:

Under the Uniform Partnership Act, which of the following statements is(are) correct regarding the effect of the assignment of an interest in a general partnership?

A. The assignee is personally responsible for the assigning partner's share of past and future partnership debts. II. The assignee is entitled to the assigning partner's interest in partnership profits and surplus on dissolution of the partnership.

B. I only.

C. II only.

D. Both I and II.

E. Neither I nor II.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.