AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

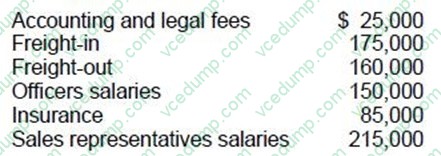

Question 761:

The following costs were incurred by ABC Co., a manufacturer, during 1992: What amount of these costs should be reported as general and administrative expenses for 1992?

A. $260,000 B. $550,000 C. $635,000 D. $810,000

A. $260,000 Explanation Explanation/Reference:Choice "a" is correct. General and administrative expenses include: Freight-in is part of cost of sales; freight-out is a selling expense; and sales salaries are selling expenses. Choice "b" is incorrect. Freight-in is part of cost of inventory; freight-out is a selling expense; and sales salaries are selling expenses. Choice "c" is incorrect. Freight-in is part of cost of inventory; freight-out is a selling expense; and sales salaries are selling expenses. Choice "d" is incorrect. Freight-in is part of cost of inventory; freight-out is a selling expense; and sales salaries are selling expenses.

Question 762:

Which of the following matters would an auditor most likely consider to be a significant deficiency in internal control to be communicated to management and those charged with governance?

A. Management's failure to renegotiate unfavorable long-term purchase commitments. B. Recurring operating losses that may indicate going concern problems. C. Evidence of a lack of objectivity by those responsible for accounting decisions. D. Management's current plans to reduce its ownership equity in the entity.

C. Evidence of a lack of objectivity by those responsible for accounting decisions. Choice "c" is correct. A lack of objectivity by those responsible for accounting decisions represents a significant internal control deficiency because it may result in financial statements that are biased rather than being presented fairly. Choice "a" is incorrect. Management's failure to renegotiate unfavorable long-term purchase commitments does not represent a significant deficiency in internal control. Choice "b" is incorrect. Going concern problems do not represent a significant deficiency in internal control. Choice "d" is incorrect. Management's plan to reduce its ownership equity in the entity does not represent a significant deficiency in internal control.

Question 763:

Which of the following factors most likely would cause an auditor not to accept a new audit engagement?

A. An inadequate understanding of the entity's internal control. B. The close proximity to the end of the entity's fiscal year. C. Concluding that the entity's management probably lacks integrity. D. An inability to perform preliminary analytical procedures before accepting the engagement.

C. Concluding that the entity's management probably lacks integrity. Choice "c" is correct. A conclusion that management lacks integrity would probably cause the auditor not to accept a new engagement. Choice "a" is incorrect. Inadequate understanding of the client's internal control would not prevent the auditor from accepting the engagement, since that understanding could be obtained later. Choice "b" is incorrect. Proximity to year-end would not prevent an auditor from accepting a new audit engagement. Choice "d" is incorrect. While analytical procedures are required during planning, this generally occurs subsequent to accepting the engagement.

Question 764:

In any competitive market, an equal increase in both demand and supply can be expected to always:

A. Increase both price and market-clearing quantity. B. Increase market-clearing quantity. C. Increase price. D. Decrease price.

B. Increase market-clearing quantity. Choice "b" is correct. As illustrated above, a shift outward (increase) in supply increases quantity supplied at equilibrium. As illustrated, this is true even when demand increases. Choice "a" is incorrect. As illustrated, price may stay the same but quantity will increase. Draw the graph! Choices "c" and "d" are incorrect. Price may remain the same, but quantity will "always" increase.

Question 765:

Which of the following statements is correct with respect to a limited partnership?

A. A limited partner may not be an unsecured creditor of the limited partnership. B. A general partner may not also be a limited partner at the same time. C. A general partner may be a secured creditor of the limited partnership. D. A limited partnership can be formed with limited liability for all partners.

C. A general partner may be a secured creditor of the limited partnership. Choice "c" is correct. In a limited partnership, a general partner may be a secured creditor of the limited partnership. Choice "a" is incorrect. In a limited partnership, a limited partner may be an unsecured creditor of the limited partnership. Choice "b" is incorrect. In a limited partnership, a general partner may also be a limited partner at the same time. Choice "d" is incorrect. In a limited partnership, only the limited partners will have limited liability. A limited partnership must have at least one general partner and general partners have unlimited liability. The word "all" makes this option wrong.

Question 766:

Mead, CPA, had substantial doubt about ABC Co.'s ability to continue as a going concern when reporting on ABC's audited financial statements for the year ended June 30, 19X4. That doubt has been removed in 19X5. What is Mead's reporting responsibility if ABC is presenting its financial statements for the year ended June 30, 19X5, on a comparative basis with those of 19X4?

A. The explanatory paragraph included in the 19X4 auditor's report should not be repeated. B. The explanatory paragraph included in the 19X4 auditor's report should be repeated in its entirety. C. A different explanatory paragraph describing Mead's reasons for the removal of doubt should be included. D. A different explanatory paragraph describing Tech's plans for financial recovery should be included.

A. The explanatory paragraph included in the 19X4 auditor's report should not be repeated. Choice "a" is correct. If substantial doubt about the entity's ability to continue as a going concern has been removed in the current period, the explanatory paragraph included in the prior period auditor's report should not be repeated, and no description of the reasons or plans for recovery need be included. Choice "b" is incorrect. If doubt about the going concern assumption has been removed in the current period, it is not appropriate to include the explanatory paragraph from the prior year in the auditor's report for the current year. Choice "c" is incorrect. If doubt about the going concern assumption has been removed in the current period, no explanatory paragraph is required since the situation no longer exists. The auditor does not have to explain the reason for the change. Choice "d" is incorrect. If doubt about the going concern assumption has been removed in the current period, no explanatory paragraph is required since the situation no longer exists. The entity does not have to describe its plans for the future.

Question 767:

In connection with a proposal to obtain a new client, an accountant in public practice is asked to prepare a written report on the application of accounting principles to a specific transaction. The accountant's report should include a statement that:

A. Any difference in the facts, circumstances, or assumptions presented may change the report. B. The engagement was performed in accordance with Statements on Standards for Consulting Services. C. The guidance provided is for management use only and may not be communicated to the prior or continuing auditors. D. Nothing came to the accountant's attention that caused the accountant to believe that the accounting principles violated GAAP.

A. Any difference in the facts, circumstances, or assumptions presented may change the report. Choice "a" is correct. The accountant's report on the application of accounting principles should include a statement that should any facts or circumstances differ from those presented to the accountant, the accountant's conclusions may change. Choice "b" is incorrect. The report should state that the engagement was performed in accordance with "AICPA Standards," not statements on Standards for Consulting Services. Choice "c" is incorrect. The report's use is restricted to "specified parties," which may include parties other than management (e.g., the board of directors). Also, the preparers of the financial statements and the reporting accountant should consult with the entity's continuing accountant. Choice "d" is incorrect. The report does not provide negative assurance with respect to GAAP; rather, it may describe the appropriate accounting principles to be applied.

Question 768:

If a publicly held company issues financial statements that purport to present its financial position and results of operations but omits the statement of cash flows, the auditor ordinarily will express a(an):

A. Disclaimer of opinion. B. Qualified opinion. C. Review report. D. Unqualified opinion with a separate explanatory paragraph.

B. Qualified opinion. Choice "b" is correct. If a company issues financial statements that purport to present financial position and results of operations but omits the related statement of cash flows, the auditor will normally conclude that the omission requires qualification of the opinion. Choice "a" is incorrect. If the company fails to present its statement of cash flows, this is considered inadequate disclosure. The auditor would not issue a disclaimer of opinion for inadequate disclosure. Choice "c" is incorrect. The auditor would not issue a review report when performing an audit. Choice "d" is incorrect. The auditor cannot issue an unqualified report if the client omits a statement of cash flows from the financial statements.

Question 769:

Monopolistic competition is characterized by:

A. A relatively large group of sellers who produce differentiated products. B. A relatively small group of sellers who produce differentiated products. C. One or two companies producing similar products. D. A relatively large group of sellers who produce a homogeneous product.

A. A relatively large group of sellers who produce differentiated products. Choice "a" is correct. Monopolistic competition is characterized by a relatively large number of sellers who produce differentiated products. There are few barriers to entry and firms exert some influence over the price and the market. Best examples are brand name consumer products. Choice "b" is incorrect. Relatively few sellers with differentiated products would indicate an oligopoly. Choice "c" is incorrect. One company would be a monopoly, two - an oligopoly. Choice "d" is incorrect. A relatively large number of sellers and a standardized product indicates perfect competition.

Question 770:

Comfort letters ordinarily are signed by the client's:

A. Independent auditor. B. Underwriter of securities. C. Audit committee. D. Senior management.

A. Independent auditor. Choice "a" is correct. A comfort letter is a letter containing a negative assurance from the CPA to the underwriter or certain other requesting parties just before the registration of the client's securities. Choice "b" is incorrect. The comfort letter is sent to the underwriter. Choice "c" is incorrect. The audit committee does not sign a comfort letter. Choice "d" is incorrect. Senior management may sign a client representation letter, not a comfort letter.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.