AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

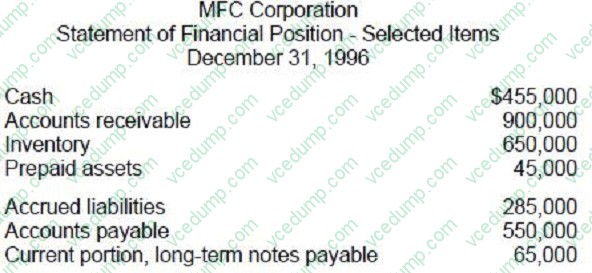

Question 191:

ABC Corporation has 100,000 shares of stock outstanding. Below is part of ABC's Statement of Financial Position for the last fiscal year.

What is the maximum amount ABC can pay in cash dividends per share and maintain a minimum current ratio of 2 to 1? Assume that all accounts other than cash remain unchanged.

A. $2.05 B. $2.50 C. $3.35 D. $3.80

B. $2.50 Explanation Explanation/Reference:Choice "b" is correct. The current ratio is found by dividing current assets by current liabilities. Presently current assets are: Because current liabilities must be two times current liabilities, the current assets cannot go below $1,800,000. Thus, current assets can go down: On a per share basis, this is $250,000 / 100,000 shares or $2.50 per share. Choices "a", "c", and "d" are incorrect, per the above calculation.

Question 192:

To decrease the money supply, the Fed might:

A. Sell government securities on the open market. B. Buy government securities on the open market. C. Decrease the required reserve ratio. D. Lower the discount rate.

A. Sell government securities on the open market. Choice "a" is correct. To decrease the money supply, the Fed can: (1) sell government securities in the open market, (2) increase the discount rate, and (3) increase the required reserve ratio. Choice "b" is incorrect. The Fed should sell (not buy) securities on the open market. Choice "c" is incorrect. The Fed should increase (not decrease) the required reserve ratio. Choice "d" is incorrect. The Fed should increase (not decrease) the discount rate.

Question 193:

Among which of the following related parties are losses from sales and exchanges not recognized for tax purposes?

A. Father-in-law and son-in-law. B. Brother-in-law and sister-in-law. C. Grandfather and granddaughter. D. Ancestors, lineal descendants, and all in-laws.

C. Grandfather and granddaughter. Choice "c" is correct. Losses from sales and exchanges are not recognized for tax purposes between grandfather and granddaughter. Rule: Losses are disallowed on sales between related parties. "Related" includes brothers and sisters, husband-wife, lineal descendants (father, son, grandfather), and entities that are more than 50% owned by individuals, corporations, trusts and/or partnerships. Choices "a", "b", and "d" are incorrect, because losses from sales and exchanges are recognized for all "in-laws."

Question 194:

Which of the following might be considered the most expansionary set of fiscal policies?

A. Increase government purchases, increase in taxes. B. Increase government purchases, decrease in taxes. C. Decrease in taxes, increase in the money supply. D. Increase in government purchases, increase in the money supply.

B. Increase government purchases, decrease in taxes. Choice "b" is correct. Expansionary fiscal policy involves increasing government purchases and/or decreasing taxes. Both increases in government spending and decreases in taxes cause the aggregate demand curve to shift right and thus cause real GDP (output) to increase. Choice "a" is incorrect. An increase in taxes is an example of contractionary fiscal policy. Choice "c" is incorrect. An increase in the money supply is expansionary monetary policy (not fiscal policy). Choice "d" is incorrect per above Explanation.

Question 195:

Which one of the following would cause the demand curve for a commodity to shift to the left?

A. A rise in the price of a substitute product. B. A rise in average household income. C. A rise in the price of a complementary commodity. D. A rise in the population.

C. A rise in the price of a complementary commodity. Choice "c" is correct. A rise in the price of a complementary commodity would cause a shift to the left in any demand curve (representing decrease in demand, at all price levels, for that product). With respect to complementary goods, the demand for the primary product is directly impacted by the demand (and hence the price changes) for the complementary goods. For instance, if the price of gasoline goes up, the demand for cars will decrease, causing the demand curve for cars to shift left. Choice "a" is incorrect. A rise in the price of a substitute product will make the demand curve shift to the right. Choice "b" is incorrect. A rise in average household income would make the demand curve shift to the right, representing an increase in demand. Choice "d" is incorrect. A rise in population, or a change in consumers' tastes in favor of the commodity are also changes that may cause an increase in demand, making the demand curve shift to the right.

Question 196:

ABC Co. processes payroll transactions for a retailer. Cook, CPA, is engaged to express an opinion on a description of ABC's internal controls placed in operation as of a specific date. These controls are relevant to the retailer's internal control, so Cook's report may be useful in providing the retailer's independent auditor with information necessary to plan a financial statement audit. Cook's report should:

A. Contain a disclaimer of opinion on the operating effectiveness of ABC's controls. B. State whether ABC's controls were suitably designed to achieve the retailer's objectives. C. Identify ABC's controls relevant to specific financial statement assertions. D. Disclose Cook's assessed level of control risk for ABC.

A. Contain a disclaimer of opinion on the operating effectiveness of ABC's controls. Choice "a" is correct. There are two types of reports on the processing of transactions by service organizations: "reports on controls placed in operation" and "reports on controls placed in operation and tests of operating effectiveness." The former do not include tests of operating effectiveness and, therefore, are not intended to provide the user auditor with a basis for reducing the assessment of control risk. Accordingly, such reports should include a disclaimer of opinion regarding the operating effectiveness of the controls. Choice "b" is incorrect. The report should contain an indication that the controls were suitably designed to achieve specified control objectives, but it does not provide any assurance regarding the achievement of the user organization's (in this case, the retailer's) objectives. Choice "c" is incorrect. The service auditor (Cook) is not required to identify the service organization's (i.e., ABC's) controls relevant to specific financial statement assertions because this is not a financial statement audit. Choice "d" is incorrect. The service auditor (Cook) is not required to disclose the assessed level of control risk for the service organization (ABC).

Question 197:

Which of the following is not a valuation technique that can be used to measure the fair value of an asset or liability?

A. The market approach. B. The impairment approach. C. The income approach. D. The cost approach.

B. The impairment approach. Choice "b" is correct. The impairment approach is not used to measure the fair value of an asset or liability. Instead, when an entity is determining whether an asset has been impaired, the entity will use the market approach, the income approach or the cost approach to determine the fair value of the asset. Choice "a" is incorrect. The market approach is an accepted method of fair value measurement in which price and other market information from identical or comparable assets or liabilities is used to measure fair value. Choice "c" is incorrect. The income approach is an accepted method of fair value measurement in which future cash flows or earnings are discounted to determine fair value. Choice "d" is incorrect. The cost approach is an accepted method of fair value measurement in which current replacement cost is used to determine the fair value of an asset.

Question 198:

ABC Co. depreciated a $12,000 asset over five years, using the straight-line method with no salvage value. At the beginning of the fifth year, it was determined that the asset will last another four years. What amount should ABC report as depreciation expense for year 5?

A. $600 B. $900 C. $1,500 D. $2,400

A. $600 Choice "a" is correct. Over the first 4 years, the asset would be depreciated down to $2,400. Once it was determined that the asset would last for another 4 years, $600 would be depreciated each year of that 4 year period. This change is a change in accounting estimate (the estimate being the life of the asset). Changes is accounting estimate are accounted for in the current year and future years if the change affects both. Choice "b" is incorrect. This answer is the annual difference between the depreciation expense IF depreciation expense had been retroactively restated ($24,000 / 8 = $1,500) and the correct depreciation expense. Retroactive restatement is not appropriate for changes in accounting estimate. Choice "c" is incorrect. This answer is the depreciation expense IF depreciation had been retroactively restated ($24,000 / 8 = $1,500). Retroactive restatement is not appropriate for changes in accounting estimate. Choice "d" is incorrect. This answer is the undepreciated amount at the beginning of the fifth year or the amount of the annual depreciation expense for each of the first 4 years. Either way, it certainly is not going to be the depreciation expense for that year because the remaining cost will depreciated over the remaining period.

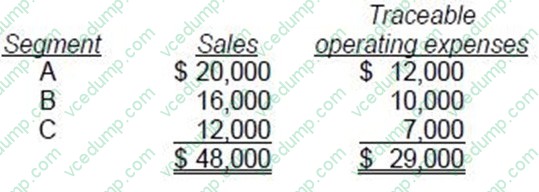

Question 199:

ABC Corp. discloses supplemental industry segment information. The following information is available for 1992:

Additional 1992 expenses, not included above, are as follows:

A. $5,000 Explanation Explanation/Reference:Choice "a" is correct. $5,000 operating profit for Segment C. Rule: Operating profit by segments is based on the measure of profit reported to the "Chief Operating Decision Maker." Interest expense, income taxes, and general corporate expenses are not allocated to the divisions solely for the purposes of segment disclosures; they may be allocated if that is how the segments report to the "Chief Operating Decision Maker."

Question 200:

An auditor should obtain sufficient knowledge of an entity's information system relevant to financial reporting to understand the:

A. Safeguards used to limit access to computer facilities. B. Process used to prepare significant accounting estimates. C. Procedures used to assure proper authorization of transactions. D. Policies used to detect the concealment of irregularities.

B. Process used to prepare significant accounting estimates. Choice "b" is correct. An auditor is responsible for evaluating the reasonableness of significant accounting estimates made by management. An entity's information system may affect the quality of such estimates and therefore should be considered by the auditor. Choices "a", "c", and "d" are incorrect. Control activities such as those designed to limit access, ensure proper authorization, and discover fraud are not directly related to the information system relevant to financial reporting.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.