AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 1161:

Within the framework of the aggregate demand/aggregate supply model, an increase in short run aggregate supply will cause:

A. Real output to expand and the price level to fall. B. Real output to decline and the price level to rise. C. Real output to expand and the price level to rise. D. Real output to decline and the price level to fall.

A. Real output to expand and the price level to fall. Explanation Explanation/Reference: Choice "a" is correct. A shift right in short run aggregate supply causes output to increase and the price level to fall. Choice "b" is incorrect. Real output would rise, not fall. Choice "c" is incorrect. The price level would fall, not rise. Choice "d" is incorrect. Real output would rise, not fall.

Question 1162:

An auditor obtains knowledge about a new client's business and its industry to:

A. Make constructive suggestions concerning improvements to the client's internal control. B. Develop an attitude of professional skepticism concerning management's financial statement assertions. C. Evaluate whether the aggregation of known misstatements causes the financial statements taken as a whole to be materially misstated. D. Understand the events and transactions that may have an effect on the client's financial statements.

D. Understand the events and transactions that may have an effect on the client's financial statements. Choice "d" is correct. The auditor should obtain knowledge of the client's business and its industry in order to determine the effect of transactions, events, and practices on the client's financial statements. Choice "a" is incorrect. Constructive suggestions concerning improvements in the new client's internal control are generally made after the study and evaluation of the client's internal control, performed subsequent to planning. Knowledge about the new client's business and its industry is generally obtained during planning. Choice "b" is incorrect. The auditor should have an attitude of professional skepticism in conducting the engagement, but this attitude is not necessarily related to the auditor's knowledge of the new client's business and its industry. Choice "c" is incorrect. The auditor should evaluate whether the aggregation of known misstatements materially affects the financial statements, but this is done near the audit's conclusion. Knowledge about the new client's business and its industry is generally obtained during planning.

Question 1163:

A market with many independent firms, low barriers to entry, and product differentiation is best classified as:

A. A natural monopoly. B. Monopolistic competition. C. An oligopoly. D. Pure competition.

B. Monopolistic competition. Choice "b" is correct. A market with many independent firms, low barriers to entry, and product differentiation is best classified as monopolistic competition. There are few barriers to entry and firms exert some influence over price in such a market. Best examples are brand name consumer products. Choice "a" is incorrect. A natural monopoly exists when economic and technical conditions permit only one efficient supplier. Choice "c" is incorrect. The presence of only one company indicates a monopoly; the presence of a few companies would indicate an oligopoly. Choice "d" is incorrect. Market conditions characterizing pure competition include homogeneous, not differentiated, products.

Question 1164:

An increase (shift right) in aggregate demand causes:

A. An increase in the price level and a decrease in real GDP. B. A decrease in the price level and an increase in real GDP. C. An increase in the price level and an increase in real GDP. D. A decrease in the price level and a decrease in real GDP.

A. An increase in the price level and a decrease in real GDP. Explanation Explanation/Reference: Choice "c" is correct. As shown above, an increase in aggregate demand causes the equilibrium price level to rise and equilibrium output (real GDP) to increase. Choice "a" is incorrect. As shown above, equilibrium output increases, not decreases. Choice "b" is incorrect. As shown above, the equilibrium price level increases, not decreases. Choice "d" is incorrect. As shown above, the equilibrium price level increases, not decreases.

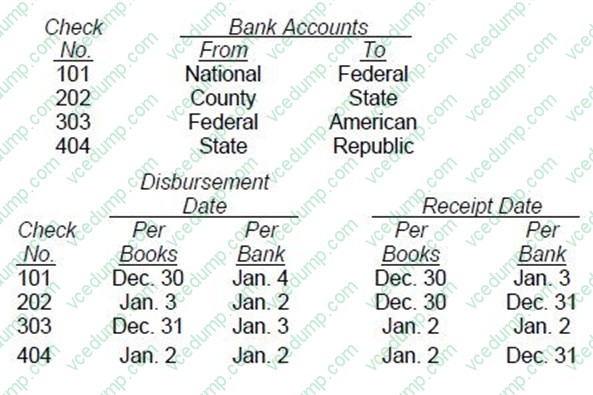

Question 1165:

The information below was taken from the bank transfer schedule prepared during the audit of ABC Co.'s financial statements for the year ended December 31, 20X1. Assume all checks are dated and issued on December 30, 20X1.

Which of the following checks might indicate kiting?

A. #101 and #303. B. #202 and #404. C. #101 and #404. D. #202 and #303.

B. #202 and #404. Choice "b" is correct. Kiting is concealing a cash shortage by depositing in one bank an unrecorded check of another disbursement bank, so that the deposit is recorded in both banks. An auditor would most likely detect kiting by reviewing the bank transfer schedule and following-up on all transfers for which the receipt date per bank is recorded in the accounting period before the disbursement date. Checks #202 and #404 both meet this criterion and therefore might indicate kiting. Choices "a", "c", and "d" are incorrect, based on the above .

Question 1166:

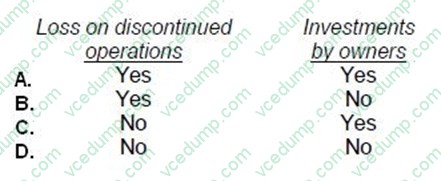

According to the FASB conceptual framework, comprehensive income includes which of the following?

A. Option A B. Option B C. Option C D. Option D

B. Option B Choice "b" is correct. Comprehensive income is the change in equity of a business during a period from transactions and other events and circumstances from non-owner sources. It includes all changes in equity except those resulting from investments by owners and distributions to owners. SFAC 6 para 70.

Question 1167:

According to the FASB conceptual framework, the objectives of financial reporting for business enterprises are based on:

A. Generally accepted accounting principles. B. Reporting on management's stewardship. C. The need for conservatism. D. The needs of the users of the information.

D. The needs of the users of the information. Choice "d" is correct. The FASB conceptual framework states that the objectives of financial reporting stem from the informational needs of the external users of the information. SFAC 1 para. 28. Choice "a" is incorrect. Generally accepted accounting principles (GAAP) are derived from and based on the objectives of financial reporting, not the other way around. Choice "b" is incorrect. Information concerning management's stewardship is only one aspect of the information financial statements are intended to provide. SFAC 1 para. 50. Choice "c" is incorrect. Conservatism is an underlying concept for financial accounting but is not the basis for the objectives. SFAC 2 para. 91-97.

Question 1168:

Government price regulations in competitive markets that set maximum or ceiling prices below the equilibrium price will in the short run:

A. Cause demand to increase. B. Cause supply to increase. C. Create shortages of that product. D. Produce a surplus of the product.

C. Create shortages of that product. Choice "c" is correct. Government price regulations in competitive markets that set maximum or ceiling prices below the equilibrium price will create shortages of that product in the short run because quantity supplied will be less than quantity demanded at that price. Choice "a" is incorrect. Quantity demand will increase at the lower price. Choice "b" is incorrect. Quantity supplied will decrease at the lower price. Choice "d" is incorrect. A price set below the market's equilibrium price causes shortages, not surpluses, per the graph above.

Question 1169:

An auditor would be most likely to identify a contingent liability by obtaining a (an):

A. Accounts payable confirmation. B. Transfer agent confirmation. C. Standard bank confirmation. D. Related party transaction confirmation.

C. Standard bank confirmation. Choice "c" is correct. An auditor would be most likely to identify a contingent liability by obtaining a standard bank confirmation, which has an "exceptions and comments" box that specifically discloses contingent liabilities as endorser of loans, for open letters of credit, etc. Choice "a" is incorrect. Confirmations of accounts payable relate to existing liabilities, not to contingent liabilities. They are not always performed and rarely disclose contingencies. Choice "b" is incorrect. Transfer agent confirmations relate to purchase and sale of securities. They are not always used and rarely disclose contingencies. Choice "d" is incorrect. Confirmations of related party transactions relate to transactions that have already occurred. They are not always used and rarely disclose contingencies.

Question 1170:

An auditor may report on condensed financial statements that are derived from complete financial statements if the:

A. Condensed financial statements are distributed to stockholders along with the complete financial statements. B. Auditor describes the additional procedures performed on the condensed financial statements. C. Auditor indicates whether the information in the condensed financial statements is fairly stated in all material respects in relation to the complete financial statements from which it has been derived. D. Condensed financial statements are presented in comparative form with the prior year's condensed financial statements.

C. Auditor indicates whether the information in the condensed financial statements is fairly stated in all material respects in relation to the complete financial statements from which it has been derived. Choice "c" is correct. An auditor may report on condensed financial statements that are derived from financial statements that he or she has audited, indicating (1) that he or she has audited and expressed an opinion on the complete financial statements, (2) the date of the auditor's report, (3) the type of opinion expressed, and (4) that the information contained in the condensed financial statements is fairly stated in all material respects in relation to the complete financial statements from which it has been derived. Choice "a" is incorrect. The condensed financial statements do not have to be distributed to the stockholders. Choice "b" is incorrect. The audit report on condensed financial statements does not require that additional procedures be described. Choice "d" is incorrect. Condensed financial statements do not need to be presented in comparative form with the prior year's financial statements.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.