CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 1151:

The segment margin of an investment center after deducting the imputed interest on the assets used by the investment center is known as:

A. Return on investment.

B. Residual income.

C. Operating income.

D. Return on assets. -

Question 1152:

When the federal government imposes health and safety regulations on certain products, one of the most likely results is:

A. Greater consumption of the product.

B. Lower prices for the product.

C. Higher prices for the product.

D. Increased supply of the product. -

Question 1153:

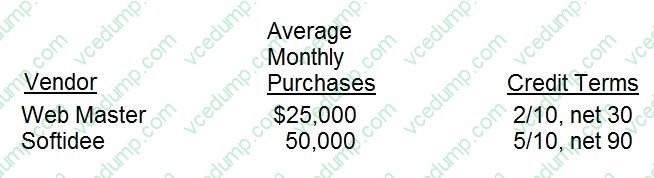

ABC outlet, a relatively new store, is a cafe that offers customers the opportunity to browse the Internet or play computer games at their tables while they drink coffee. The customer pays a fee based on the amount of time spent signed on to the computer. The store also sells books, tee shirts, and computer accessories. ABC has been paying all of its bills on the last day of the payment period, thus forfeiting all supplier discounts. Shown below are data on ABC's two major vendors, including average monthly purchases and credit terms.

Assuming a 360-day year and that ABC continues paying on the last day of the credit period, the company's weighted annual interest rate for trade credit (ignoring the effects of compounding) for these two vendors is:

A. 27.0 percent.

B. 28.0 percent.

C. 29.3 percent.

D. 30.2 percent. -

Question 1154:

In 1990, ABC Corp., a closely held corporation, was formed by Adams, Frank, and Berg as incorporators and stockholders. Adams, Frank, and Berg executed a written voting agreement which provided that they would vote for each other as directors and officers. In 1994, stock in the corporation was offered to the public. This resulted in an additional 300 stockholders. After the offering, Adams holds 25%, Frank holds 15%, and Berg holds 15% of all issued and outstanding stock. Adams, Frank, and Berg have been directors and officers of the corporation since the corporation was formed. Regular meetings of the board of directors and annual stockholders meetings have been held. For this question refer to the formation of ABC Corp. and the rights and duties of its stockholders, directors, and officers. ABC Corp.'s directors are elected by its:

A. Officers.

B. Outgoing directors.

C. Stockholders. -

Question 1155:

Several sources of GAAP consulted by an auditor are in conflict as to the application of an accounting principle. Which of the following should the auditor consider the most authoritative?

A. FASB Technical Bulletins.

B. AICPA Accounting Interpretations.

C. FASB Statements of Financial Accounting Concepts.

D. AICPA Technical Practice Aids. -

Question 1156:

Pell, CPA, decides to serve as principal auditor in the audit of the financial statements of ABC, Inc. Smith, CPA, audits one of ABC's subsidiaries. In which situation(s) should Pell make reference to Smith's audit?

A. Pell reviews Smith's audit documentation and assumes responsibility for Smith's work, but expresses a qualified opinion on ABC's financial statements. II. Pell is unable to review Smith's audit documentation; however, Pell's inquiries indicate that Smith has an excellent reputation for professional competence and integrity.

B. I only.

C. II only.

D. Both I and II.

E. Neither I nor II. -

Question 1157:

Auditor confirmation of accounts payable balances at the balance sheet date may be unnecessary because:

A. This is a duplication of cutoff tests.

B. Accounts payable balances at the balance sheet date may not be paid before the audit is completed.

C. Correspondence with the audit client's attorney will reveal all legal action by vendors for nonpayment.

D. There is likely to be other reliable external evidence available to support the balances. -

Question 1158:

When evaluating capital budgeting analysis techniques, the payback period emphasizes:

A. Liquidity.

B. Profitability.

C. Net income.

D. The accounting period. -

Question 1159:

In order to sell at the rate of output in markets controlled by monopolists, price is set where:

A. Price equals marginal cost.

B. Marginal revenue equals marginal cost.

C. Marginal revenue equals average total cost.

D. Price equals average total cost. -

Question 1160:

A perfectly inelastic supply curve in a competitive market:

A. Means the equilibrium price must be zero.

B. Implies a vertical demand curve.

C. Exists when firms cannot vary input usage.

D. Says the market supply curve is horizontal.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.