AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 1181:

ABC Industries conducts business in a number of different countries and is trying to evaluate its economic exposure to exchange rate risk. Which of the following statements is not correct?

A. ABC will suffer an economic loss in the event it has net cash outflows of a foreign currency and the foreign currency appreciates. B. ABC will enjoy an economic gain in the event it has net cash outflows of a foreign currency and the foreign currency depreciates. C. ABC will suffer an economic loss in the event it has net cash inflows of a foreign currency and the foreign currency appreciates. D. ABC will suffer an economic loss in the event it has net cash inflows of a foreign currency and the foreign currency depreciates.

C. ABC will suffer an economic loss in the event it has net cash inflows of a foreign currency and the foreign currency appreciates. Choice "c" is correct. ABC will benefit from an economic gain in the event that it has net cash inflows of a foreign currency and the foreign currency appreciates (the domestic currency depreciates). ABC will collect a more valuable currency that can buy more of its domestic currency. Choices "a", "b", and "d" are incorrect because they are correct statements.

Question 1182:

In a well designed internal control, employees in the same department most likely would approve purchase orders, and also:

A. Reconcile the open invoice file. B. Inspect goods upon receipt. C. Authorize requisitions of goods. D. Negotiate terms with vendors.

D. Negotiate terms with vendors. Choice "d" is correct. In a well designed internal control, employees in the purchasing department most likely would approve purchase orders and also negotiate terms with vendors. Choice "a" is incorrect. Personnel in the accounts payable department reconcile the open invoice file while the purchasing agent approves purchase orders. Choice "b" is incorrect. Employees in the receiving department inspect goods upon receipt while the purchasing agent approves purchase orders. Choice "c" is incorrect. The stores department (personnel in the raw materials inventory area) authorize requisition of goods while the purchasing agent approves purchase orders.

Question 1183:

ABC Co. had the following 1994 financial statement relationships: Asset turnover 5 Profit margin on sales 0.02

What was ABC's 1994 percentage return on assets?

A. 0.1 percent. B. 0.4 percent. C. 2.5 percent. D. 10.0 percent.

D. 10.0 percent. Explanation Explanation/Reference:Choice "d" is correct. Return on assets equals income divided by average assets. This formula can be further divided into the components of profit margin times asset turnover (referred to as the Dupont formula): Choices "a", "b", and "c" are incorrect, per the above calculation.

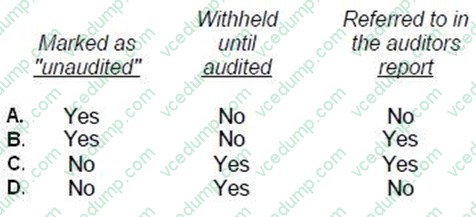

Question 1184:

When unaudited financial statements are presented in comparative form with audited financial statements in a document filed with the Securities and Exchange Commission, such statements should be:

A. Option A B. Option B C. Option C D. Option D

A. Option A Choice "a" is correct. When unaudited financial statements (generally the first quarter of the following year in an annual report) are presented in comparative form with audited financial statements in documents filed with the SEC, such statements should be clearly marked as "unaudited," but should not be referred to in the auditor's report. The statements need not be withheld until audited. Choices "b", "c", and "d" are incorrect, based on explanation above.

Question 1185:

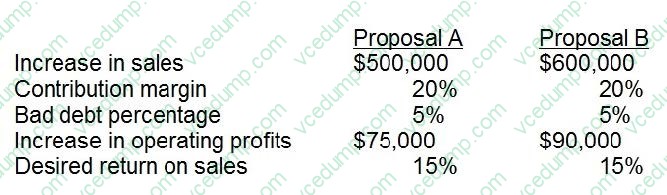

The sales manager at ABC Company feels confident that if the credit policy at ABC's was changed, sales would increase and, consequently, the company would utilize excess capacity. The two credit proposals being considered are as follows:

Currently, payment terms are net 30. The proposal payment terms for Proposal A and Proposal B are net 45 and net 90, respectively. An analysis to compare these two proposals for the change in credit policy would include all of the following factors, except the:

A. Cost of funds for ABC. B. Current bad debt experience. C. Impact on the current customer base of extending terms to only certain customers. D. Bank loan covenants on days sales outstanding.

B. Current bad debt experience. Choice "b" is correct. Because the bad debt percentage is the same under either of the two proposals, there is no differential cost associated with bad debt. Because it is not a differential cost, it is not considered in comparing the two alternatives. Choice "a" is incorrect. Because Proposal A and B have different net collection dates, Proposal B will cause a greater amount of accounts receivable with a corresponding increase in working capital. The cost to fund this will be greater for Proposal B, so this is a legitimate concern. Choice "c" is incorrect. Customers may feel they should be given the extended terms. If this is granted, the additional working capital need will be even greater. Choice "d" is incorrect. Banks may require that days sales outstanding cannot exceed a certain number of days. If so, it will be harder to meet this covenant with Proposal B.

Question 1186:

Determining the appropriate level of working capital for a firm requires:

A. Changing the capital structure and dividend policy of the firm. B. Maintaining short-term debt at the lowest possible level because it is generally more expensive than long-term debt. C. Offsetting the benefit of current assets and current liabilities against the probability of technical insolvency. D. Maintaining a high proportion of liquid assets to total assets in order to maximize the return on total investments.

C. Offsetting the benefit of current assets and current liabilities against the probability of technical insolvency. Choice "c" is correct. Determining the appropriate level of working capital for a firm requires offsetting the benefit of current assets and current liabilities against the probability of technical insolvency. Choice "a" is incorrect. Changing the capital structure (common stock vs. preferred stock vs. long-term debt) and dividend policy has nothing to do with the level of working capital required for day-to-day operations of the business. Choice "b" is incorrect. The relative interest cost of short-term vs. long-term debt does not determine the appropriate level of working capital. Choice "d" is incorrect. Because profitability varies inversely with liquidity, maximizing the return on total investments would require a low (not high) level of liquid assets and a high level of liquid assets does nothing to determine the required level of working capital.

Question 1187:

On December 2, 20X1, ABC Corp.'s board of directors voted to discontinue operations of its frozen food division and to sell the division's assets on the open market as soon as possible. The division reported net operating losses of $20,000 in December and $30,000 in January. On February 26, 20X2, sale of the division's assets resulted in a gain of $90,000. Assuming that the frozen foods division qualifies as a component of the business and ignoring income taxes, what amount of gain/loss from discontinued operations should ABC recognize in its income statement for 20X2?

A. $0 B. $40,000 C. $60,000 D. $90,000

C. $60,000 Choice "c" is correct. The $60,000 gain from discontinued operations would be reported in ABC's 20X2 income statement. The operating loss for January would offset the gain from disposal in February, and the net amount would be reported as a gain (in this case) from discontinued operations. The operating losses for December would have been reported in ABC's 20X1 income statement. Choice "a" is incorrect per the above. It would be correct if all of the gains and losses were included in 20X1 instead of 20X2. However, gains and losses from discontinued operations are included in the year they occur. Choice "b" is incorrect. It includes the operating loss for December, 20X1 in with the 20X2 amounts. Choice "d" is incorrect. It ignores the January operating loss. Operating losses are included in gain/loss from discontinued operations, along with impairment losses and gains/losses on disposal.

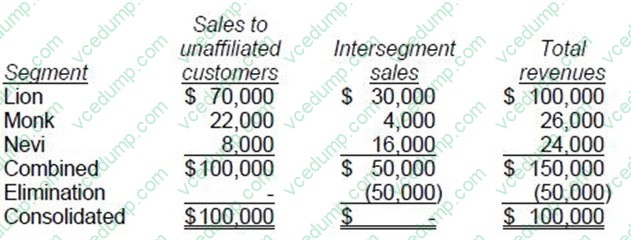

Question 1188:

ABC Co.'s total revenues from its three operating segments were as follows:

Which operating segment(s) is (are) deemed to be reportable segments?

A. None. B. Lion only. C. Lion and Monk only. D. Lion, Monk, and Nevi.

D. Lion, Monk, and Nevi. Choice "d" is correct. A reportable operating segment is one having 10% of all revenue, including revenue from unaffiliated sales and from intersegment sales: Lion's revenue percentage is 66.7% [$100,000/150,000]. Monk's revenue percentage is 17.3% [$26,000/150,000]. Nevi's revenue percentage is 16% [$24,000/150,000]. Thus, all three segments meet the 10% of total revenues test and are reportable as operating segments. SFAS 14 para. 10 and 15 as amended by SFAS 131 Choice "a" is incorrect. All segments with revenue percentages exceeding 10% of total revenues are reportable operating segments. Choice "b" is incorrect. Lion is not the only segment with revenue percentages exceeding 10% of total revenues. Choice "c" is incorrect. Nevi has a revenue percentage exceeding 10% of total revenues.

Question 1189:

Berry, Drake, and Flanigan are partners in a general partnership. The partners made capital contributions as follows: Berry, $150,000; Drake, $100,000; and Flanigan, $50,000. Drake made a loan of $50,000 to the partnership. The partnership agreement specifies that Flanigan will receive a 50% share of profits, and Drake and Berry each will receive a 25% share of profits. Under the Revised Uniform Partnership Act and in the absence of any partnership agreement to the contrary, which of the following statements is correct regarding the sharing of losses?

A. The partners will share equally in any partnership losses. B. The partners will share in losses on a pro rata basis according to the capital contributions. C. The partners will share in losses on a pro rata basis according to the capital contributions and loans made to the partnership. D. The partners will share in losses according to the allocation of profits specified in the partnership agreement.

D. The partners will share in losses according to the allocation of profits specified in the partnership agreement. Choice "d" is correct. Under the Revised Uniform Partnership Act, unless agreed otherwise, partners share losses in the same manner that they share profits. Choice "a" is incorrect. Under the Revised Uniform Partnership Act, unless agreed otherwise, partners share losses in the same manner that they share profits. Here, the partners agreed to share profits in a 2:1:1 ratio. Thus, losses will be shared in that manner rather than equally. Choice "b" is incorrect. Under the Revised Uniform Partnership Act, unless agreed otherwise, partners share losses in the same manner that they share profits. They are not shared in accordance with the partners' capital contributions. Choice "c" is incorrect. Under the Revised Uniform Partnership Act, unless agreed otherwise, partners share losses in the same manner that they share profits. They are not shared in accordance with the partners' capital contributions or loans.

Question 1190:

On November 1, 20X2, ABC Co. contracted to dispose of an industry segment. Throughout 20X2 the segment had operating losses. These losses were expected to continue until the segment's disposition. If a loss is projected on final disposition, how much of the operating losses should be included in the loss from discontinued operations reported in ABC's 20X2 income statement?

A. Operating losses for the period January 1 to October 31, 20X2. II. Operating losses for the period November 1 to December 31, 20X2. III. Estimated operating losses for the period January 1 to February 28, 20X3. B. II only. C. II and III only. D. I and III only. E. I and II only.

D. I and III only. Choice "d" is correct. The operating losses to be included in ABC's 20X2 income statement would be the total 20X2 operating losses, regardless of whether those losses occurred before or after the date the decision to dispose of the component was made, and not any 20X3 operating losses. Projected operating losses are not anticipated and accrued. Choice "a" is incorrect. The operating losses to be included in ABC's 20X2 income statement would be the total 20X2 operating losses, regardless of whether those losses occurred before or after the date the decision to dispose of the component was made, and not any 20X3 operating losses. Choice "b" is incorrect. The operating losses to be included in ABC's 20X2 income statement would be the total 20X2 operating losses, regardless of whether those losses occurred before or after the date the decision to dispose of the component was made, and not any 20X3 operating losses. Choice "c" is incorrect. The operating losses to be included in ABC's 20X2 income statement would be the total 20X2 operating losses, regardless of whether those losses occurred before or after the date the decision to dispose of the component was made, and not any 20X3 operating losses.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.