CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 1101:

If demand is price inelastic:

A. An increase in price will result in a decrease in total revenue.

B. An increase in price will result in an increase the quantity demanded that is more than the increase in price.

C. An increase in price will result in an increase in total revenue.

D. An increase in price will have no effect on total revenue. -

Question 1102:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent. Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

During 1994, the Moores received a $2,500 federal tax refund and a $1,250 state tax refund for 1993 overpayments. In 1993, the Moores were not subject to the alternative minimum tax and were not entitled to any credit against income tax. The Moores' 1993 adjusted gross income was $80,000 and itemized deductions were $1,450 in excess of the standard deduction. The state tax deduction for 1993 was $2,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 K. $10,000 L. $25,000 M. $50,000 N. $55,000 O. $75,000 -

Question 1103:

A CPA's report on agreed-upon procedures related to management's assertion about an entity's compliance with specified requirements should contain:

A. A statement of limitations on the use of the report.

B. An opinion about whether management's assertion is fairly stated.

C. Negative assurance that control risk has not been assessed.

D. An acknowledgment of responsibility for the sufficiency of the procedures. -

Question 1104:

Doug was the sole general partner in ABC, Limited Partnership. While driving to work one morning, Doug died in a car accident. The limited partnership:

A. Continues to exist as it was before Doug's death.

B. Dissolves by operation of law as a result of Doug's death.

C. Dissolves only by attaining a judicial decree.

D. Converts to a general partnership and all former limited partners become general partners. -

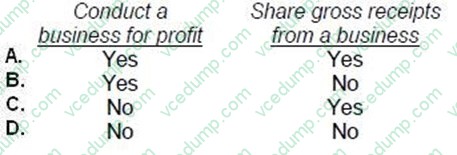

Question 1105:

When parties intend to create a partnership that will be recognized under the Revised Uniform Partnership Act, they must agree to:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 1106:

Strategy is a broad term that usually means the selection of overall objectives. Strategic analysis would generally exclude the:

A. Trends that will affect the entity's markets.

B. Target product mix and production schedule to be maintained during the year.

C. Forms of organizational structure that would best serve the entity.

D. Best ways to invest in research, design, production, distribution, marketing, and administrative activities. -

Question 1107:

The most reliable procedure for an auditor to use to test the existence of a client's inventory at an outside location would be to:

A. Observe physical counts of the inventory items.

B. Trace the total on the inventory listing to the general ledger inventory account.

C. Obtain a confirmation from the client indicating inventory ownership.

D. Analytically compare the current-year inventory balance to the prior-year balance. -

Question 1108:

An auditor of a nonpublic company must conduct the audit in accordance with:

A. ASB standards. II. PCAOB standards.

B. I.

C. Both I and II.

D. Either I or II, but not both.

E. II. -

Question 1109:

Which one of the following is most relevant to a manufacturing equipment replacement decision?

A. Original cost of the old equipment.

B. Disposal price of the old equipment.

C. Gain or loss on the disposal of the old equipment.

D. A lump-sum write-off amount from the disposal of the old equipment. -

Question 1110:

During a period when an enterprise is under the direction of a particular management, its financial statements will directly provide information about:

A. Both enterprise performance and management performance.

B. Management performance but not directly provide information about enterprise performance.

C. Enterprise performance but not directly provide information about management performance.

D. Neither enterprise performance nor management performance.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.