AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 1121:

When purchasing temporary investments, which one of the following best describes the risk associated with the ability to sell the investment in a short period of time without significant price concessions?

A. Interest rate risk. B. Purchasing power risk. C. Financial risk. D. Liquidity risk.

D. Liquidity risk. Choice "d" is correct. Liquidity risk is associated with the ability to sell the temporary investment in a short period of time without significant price concessions. Choice "a" is incorrect. Interest rate risk is the fluctuation in the value of a "financial asset" when interest rates change. Choice "b" is incorrect. Purchasing power risk is the risk that price levels will change and affect asset values (mostly real estate). Choice "c" is incorrect. Financial risk is a general category of risk that includes: ?Interest rate risk ?Market risk ?Purchasing power risk ?Liquidity risk ?Default risk

Question 1122:

Under a $150,000 insurance policy on her deceased father's life, May Green is to receive $12,000 per year for 15 years. Of the $12,000 received in 1987, the amount subject to income tax is:

A. $0 B. $1,000 C. $2,000 D. $12,000

C. $2,000 Choice "c" is correct. $2,000.

Question 1123:

When reporting on conditions relating to an entity's internal control observed during an audit of the financial statements of a nonissuer, the auditor should include a:

A. Description of tests performed to search for material weaknesses. B. Statement of positive assurance on internal control. C. Paragraph describing the inherent limitations of internal control. D. Restriction on the use of the report.

D. Restriction on the use of the report. Choice "d" is correct. When reporting on conditions relating to an entity's internal control observed during an audit of the financial statements, the auditor should include a restriction on the use of the report. Choice "a" is incorrect. The auditor would not include a description of tests performed to search for material weaknesses since the auditor is not in fact obligated to search for them. Choices "b" and "c" are incorrect. An auditor would make a statement of positive assurance on internal control and include a paragraph describing the inherent limitations of internal control in conjunction with an engagement to report on internal control. These comments would not be made when reporting on an entity's internal control in conjunction with an audit of the financial statements of a nonissuer.

Question 1124:

Which of the following statements is correct regarding the division of profits in a general partnership when the written partnership agreement only provides that losses be divided equally among the partners?

Profits are to be divided:

A. Based on the partners' ratio of contribution to the partnership. B. Based on the partners' participation in day-to-day management. C. Equally among the partners. D. Proportionately among the partners.

C. Equally among the partners. Choice "c" is correct. Rule: When the partnership agreement is silent as to how profits are to be divided, they are divided equally. Note also that when the agreement is silent, losses are treated similar to profits, there is no reverse rule that profits are treated like losses. Choices "a", "b", and "d" are incorrect, per the above rule.

Question 1125:

A company has two divisions. Division A has operating income of $500 and total assets of $1,000. Division B has operating income of $400 and total assets of $1,600. The required rate of return for the company is 10%. The company's residual income would be which of the following amounts?

A. $0 B. $260 C. $640 D. $900

C. $640 Choice "c" is correct. Residual income is the difference between net income and the required return. The required return is net book value (total assets) times the hurdle rate (required rate of return). The calculations are as follows: Choice "a" is incorrect. Residual income would certainly not be $0 in this question because the operating income is greater than the required return for both Division A and Division B. Choice "b" is incorrect. The $260 is the total required return, not the total residual income. Choice "d" is incorrect. The $900 is the total operating income, not the total residual income.

Question 1126:

The three elements needed to estimate the cost of equity capital for use in determining a firm's weighted average cost of capital are:

A. Current dividends per share, expected growth rate in earnings per share, and current market price per share of common stock. B. Current earnings per share, expected growth rate in dividends per share, and current market price per share of common stock. C. Current earnings per share, expected growth rate in earnings per share, and current book value per share of common stock. D. Current dividends per share, expected growth rate in dividends per share, and current market price per share of common stock.

D. Current dividends per share, expected growth rate in dividends per share, and current market price per share of common stock. Choice "d" is correct. The three elements needed to estimate the cost of equity capital are: 1. Current dividends per share (D) 2. Expected growth rate in dividends (g) and 3. Current market price per share of common stock (P) The question asks the candidate to identify the three elements needed to estimate the cost of equity capital for use in determining a firm's weighted average cost of capital. The cost of equity capital is defined by the following mathematical expression where the cost of capital or return (R) is: R = D/P + g Choice "d" is consistent with our text, theand the Gordon Growth Model. Use of earnings per share, as suggested by choice "a" is sometimes referred to as the constant growth model and assumes that all earnings per share are either ultimately distributed or reinvested for the benefit of the shareholder. Earnings are anticipated to grow to infinity.

Question 1127:

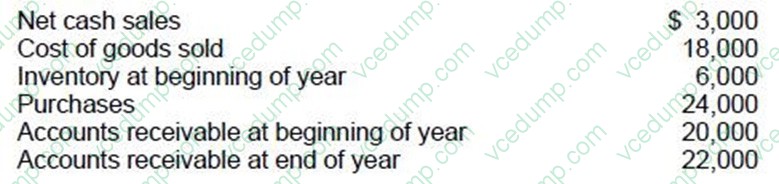

Selected data pertaining to ABC Co. for the calendar year 20X4 is as follows:

The accounts receivable turnover for 20X4 was 5.0 times. What were ABC's 20X4 net credit sales?

A. $105,000 B. $107,000 C. $110,000 D. $210,000

A. $105,000 Choice "a" is correct. The accounts receivable turnover ratio equals net credit sales divided by average accounts receivable. 5.0 = net credit sales / [($20,000 + $22,000)/2]. Net credit sales equal $105,000. Choice "b" is incorrect. The accounts receivable turnover ratio equals net credit sales divided by average accounts receivable. Choice "c" is incorrect. The accounts receivable turnover ratio equals net credit sales divided by average accounts receivable, not by year-end accounts receivable. Choice "d" is incorrect. The accounts receivable turnover ratio equals net credit sales divided by average accounts receivable, not by the sum of beginning and ending accounts receivable.

Question 1128:

Suppose the equilibrium wage for low skilled workers in California is $6.00 an hour. If the government increases the minimum wage to $7.00 an hour, what would be the effect on the market for low skilled labor?

A. An excess demand for labor would result. B. An excess supply of labor would result. C. The demand for labor would decrease. D. The supply of labor would increase.

B. An excess supply of labor would result. Choice "b" is correct. A minimum wage that is set above the equilibrium wage will result in an excess supply (or surplus) of labor. Choice "a" is incorrect, since the quantity demanded of labor at $7 is less than the quantity supplied, implying an excess supply not an excess demand. Choice "c" is incorrect. An increase in the minimum wage causes a decrease in quantity demanded of labor, not a decrease in the demand (shift in demand) for labor. Choice "d" is incorrect, per the above Explanation.

Question 1129:

Which tool would most likely be used to determine the best course of action under conditions of uncertainty?

A. Cost-volume-profit analysis. B. Expected value (EV). C. Program evaluation and review technique (PERT). D. Scattergraph method.

B. Expected value (EV). Choice "b" is correct. Probability and expected value formulate quantitative models to address the issue of appropriate course of action in an environment of uncertainty. The expected value is a weighted average of all values and variables. The course of action with the highest expected monetary value should be selected. Choice "a" is incorrect. Cost-volume profit analysis is a method used to evaluate operating decisions. Choice "c" is incorrect. PERT is a technique used in project management that focuses on the time required to complete each step in a project. It allows a project manager to monitor a project's progress and identify potential bottlenecks or delays that will postpone the completion date. Choice "d" is incorrect. The scattergraph method is used in statistical analysis to plot relationships between variables to determine a line function that best describes those relationships.

Question 1130:

Which of the following procedures would an auditor most likely include in the initial planning of a financial statement audit?

A. Obtaining a written representation letter from the client's management. B. Examining documents to detect illegal acts having a material effect on the financial statements. C. Considering whether the client's accounting estimates are reasonable in the circumstances. D. Determining the extent of involvement of the client's internal auditors.

D. Determining the extent of involvement of the client's internal auditors. Choice "d" is correct. The auditor considers several factors in planning the nature, timing and extent of auditing procedures. One of these factors is the extent of involvement of the client's internal auditors. Choice "a" is incorrect. Representation letters are obtained by the auditor at the end of the audit. The representation letter should not be dated earlier than the date of the auditor's report. Choice "b" is incorrect. The auditor does not perform tests to detect illegal acts during the planning process. Choice "c" is incorrect. The auditor does obtain and evaluate evidence to support significant accounting estimates, but this occurs subsequent to initial planning.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.