CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 1091:

The objective of performing analytical procedures in planning an audit is to identify the existence of:

A. Unusual transactions and events.

B. Illegal acts that went undetected because of internal control weaknesses.

C. Related party transactions.

D. Recorded transactions that were not properly authorized. -

Question 1092:

Which of the following accurately depicts the auditor's responsibility with respect to Statements on Auditing Standards?

A. The auditor is required to follow the guidance provided by the Standards, without exception.

B. The auditor is generally required to follow the guidance provided by Standards with which he or she is familiar, but will not be held responsible for departing from provisions of which he or she was unaware.

C. The auditor is generally required to follow the guidance provided by the Standards, unless following such guidance would result in an audit that is not cost-effective.

D. The auditor is generally required to follow the guidance provided by the Standards, and should be able to justify any departures. -

Question 1093:

On August 31, 1992, ABC Co. decided to change from the FIFO periodic inventory system to the weighted average periodic inventory system. ABC is on a calendar year basis. The cumulative effect of the change is determined:

A. As of January 1, 1992.

B. As of August 31, 1992.

C. During the eight months ending August 31, 1992, by a weighted average of the purchases.

D. During 1992 by a weighted average of the purchases. -

Question 1094:

This question will represent a statement, question, excerpt, or comment taken from various parts of an auditor's documentation file. Letter choices A-P represent a list of the likely sources of the statement, question, excerpt, or comment.

Select, as the best answer for each item, the most likely source. Select only one source for each item.

As discussed in Note 4 to the financial statements, the company experienced a net loss for the year ended July 31, 20XX, and is currently in default under substantially all of its debt agreements. In addition, on September 25, 20XX, the

company filed a prenegotiated voluntary petition for relief under Chapter 11 of the U.S. Bankruptcy Code. These matters raise substantial doubt about the company's ability to continue as a going concern.

A. Practitioner's report on management's assertion about an entity's compliance with specified requirements.

B. Auditor's communications on significant deficiencies in internal control.

C. Audit inquiry letter to legal counsel.

D. Lawyer's response to audit inquiry letter.

E. Communication from those charged with governance to the auditor.

F. Auditor's communication to those charged with governance (other than with respect to significant deficiencies in internal control).

G. Report on the application of accounting principles.

H. Auditor's engagement letter.

I. Letter for underwriters.

J. Accounts receivable confirmation request. K. Request for bank cutoff statement. L. Explanatory paragraph of an auditor's report on financial statements. M. Partner's engagement review notes. N. Management representation letter. O. Successor auditor's communication with predecessor auditor. P. Predecessor auditor's communication with successor auditor. -

Question 1095:

In the hierarchy of generally accepted accounting principles, APB Opinions have the same authority as AICPA:

A. Statements of Position.

B. Industry Audit and Accounting Guides.

C. Issues Papers.

D. Accounting Research Bulletins. -

Question 1096:

If a nation has many rival domestic firms which are all competitive in the global marketplace for a product, which of the four major factors that Michael Porter has indicated impact the global competitive environment would allow this nation to fare better with respect to global competitive advantage?

A. Conditions of the factors of production.

B. Conditions of domestic demand.

C. Related and supporting industries.

D. Firm strategy, structure, and rivalry. -

Question 1097:

An auditor who wishes to capture an entity's data as transactions are processed and continuously test the entity's computerized information system most likely would use which of the following techniques?

A. Snapshot application.

B. Embedded audit module.

C. Integrated data check.

D. Test data generator. -

Question 1098:

Under FASB Statement of Financial Accounting Concepts #5, which of the following items would cause earnings to differ from comprehensive income for an enterprise in an industry not having specialized accounting principles?

A. Unrealized loss on investments in noncurrent marketable equity securities available for sale.

B. Unrealized loss on investments in current marketable equity securities held for trading.

C. Loss on exchange of nonmonetary assets without commercial substance.

D. Loss on exchange of nonmonetary assets with commercial substance. -

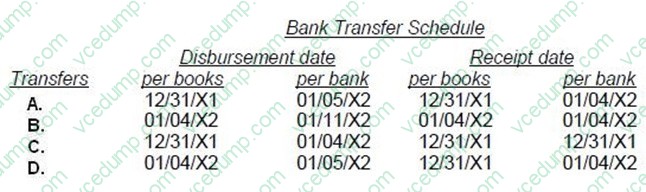

Question 1099:

Which of the following cash transfers results in a misstatement of cash at December 31, 20X1?

A. Option A

B. Option B

C. Option C

D. Option D -

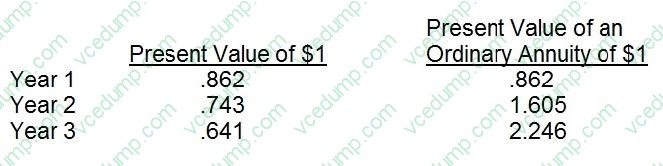

Question 1100:

ABC Inc. is considering the purchase of a new machine that will cost $150,000. The machine has an estimated useful life of three years. Assume for simplicity that the equipment will be fully depreciated 30, 40, and 30 percent in each of the three years, respectively. The new machine will have a $10,000 resale value at the end of its estimated useful life. The machine is expected to save the company $85,000 per year in operating expenses. ABC uses a 40 percent estimated income tax rate and a 16 percent hurdle rate to evaluate capital projects.

Discount rates for a 16 percent rate are as follows.

What is the net present value of this project?

A. $15,842

B. $13,278

C. $9,432

D. $(35,454)

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.