CPA-REGULATION Exam Details

-

Exam Code

:CPA-REGULATION -

Exam Name

:CPA Regulation -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:69 Q&As -

Last Updated

:Jul 14, 2026

Test Prep CPA-REGULATION Online Questions & Answers

-

Question 61:

DAC Foundation awarded Kent $75,000 in recognition of lifelong literary achievement. Kent was not required to render future services as a condition to receive the $75,000. What condition(s) must have been met for the award to be excluded from Kent's gross income?

I. Kent was selected for the award by DAC without any action on Kent's part.

II.

Pursuant to Kent's designation, DAC paid the amount of the award either to a governmental unit or to a charitable organization.

A. I only.

B. II only.

C. Both I and II.

D. Neither I nor II.

I. Kent was selected for the award by DAC without any action on Kent's part. II. Pursuant to Kent's designation, DAC paid the amount of the award either to a governmental unit or to a charitable organization. -

Question 62:

Conner purchased 300 shares of Zinco stock for $30,000 in 1980. On May 23, 1994, Conner sold all the stock to his daughter Alice for $20,000, its then fair market value. Conner realized no other gain or loss during 1994. On July 26, 1994,

Alice sold the 300 shares of Zinco for $25,000.

What was Alice's recognized gain or loss on her sale?

A. $0

B. $5,000 long-term gain.

C. $5,000 short-term loss.

D. $5,000 long-term loss. -

Question 63:

Barkley owns a vacation cabin that was rented to unrelated parties for 10 days during the year for $2,500. The cabin was used personally by Barkley for three months and left vacant for the rest of the year. Expenses for the cabin were as follows:

Real estate taxes $1,000 Maintenance and utilities $2,000

How much rental income (loss) is included in Barkley's adjusted gross income?

A. $0

B. $500

C. $(500)

D. $(1,500) -

Question 64:

Clark bought Series EE U.S. Savings Bonds after 1989. Redemption proceeds will be used for payment of college tuition for Clark's dependent child. One of the conditions that must be met for tax exemption of accumulated interest on these bonds is that the:

A. Purchaser of the bonds must be the sole owner of the bonds (or joint owner with his or her spouse).

B. Bonds must be bought by a parent (or both parents) and put in the name of the dependent child.

C. Bonds must be bought by the owner of the bonds before the owner reaches the age of 24.

D. Bonds must be transferred to the college for redemption by the college rather than by the owner of the bonds. -

Question 65:

Darr, an employee of Sorce C corporation, is not a shareholder. Which of the following would be included in a taxpayer's gross income?

A. Employer-provided medical insurance coverage under a health plan.

B. A $10,000 gift from the taxpayer's grandparents.

C. The fair market value of land that the taxpayer inherited from an uncle.

D. The dividend income on shares of stock that the taxpayer received for services rendered. -

Question 66:

Doris and Lydia are equal partners in the capital and profits of Agee and Nolan, but are otherwise unrelated. The following information pertains to 300 shares of Mast Corp. stock sold by Lydia to Agee and Nolan:

The amount of long-term capital loss that Lydia realized in 1988 on the sale of this stock was:

A. $5,000

B. $3,000

C. $2,500

D. $0 -

Question 67:

Elm Corp. is an accrual-basis calendar-year C corporation with 100,000 shares of voting common stock issued and outstanding as of December 28, 1996. On Friday, December 29, 1996, Hall surrendered 2,000 shares of Elm stock to Elm in exchange for $33,000 cash. Hall had no direct or indirect interest in Elm after the stock surrender. Additional information follows: What amount of income did Hall recognize from the stock surrender?

A. $33,000 dividend.

B. $25,000 dividend.

C. $18,000 capital gain.

D. $17,000 capital gain. -

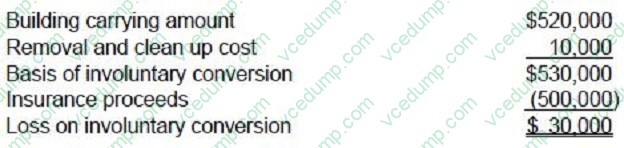

Question 68:

On December 31, 1989, a building owned by Pine Corp. was totally destroyed by fire. The building had fire insurance coverage up to $500,000. Other pertinent information as of December 31, 1989 follows:

During January 1990, before the 1989 financial statements were issued, Pine received insurance proceeds of $500,000. On what amount should Pine base the determination of its loss on involuntary conversion?

A. $520,000

B. $530,000

C. $550,000

D. $560,000 -

Question 69:

Among which of the following related parties are losses from sales and exchanges not recognized for tax purposes?

A. Father-in-law and son-in-law.

B. Brother-in-law and sister-in-law.

C. Grandfather and granddaughter.

D. Ancestors, lineal descendants, and all in-laws.

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-REGULATION exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.