CPA-REGULATION Exam Details

-

Exam Code

:CPA-REGULATION -

Exam Name

:CPA Regulation -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:69 Q&As -

Last Updated

:Jul 14, 2026

Test Prep CPA-REGULATION Online Questions & Answers

-

Question 31:

An individual had the following capital gains and losses for the year:

What will be the net gain (loss) reported by the individual and at what applicable tax rate(s)?

A. Long-term gain of $16,000 at the 15% rate.

B. Short-term loss of $3,000 at the ordinary rate and long-term capital gain of $86,000 at the 15% rate.

C. Long-term capital gain of $3,000 at the 15% rate, collectibles gain of $10,000 at the 28% rate, and Section 1250 gain of $56,000 at the 25% rate.

D. Short-term loss of $3,000 at the ordinary rate, long-term capital gain of $10,000 at the 15% rate, collectibles gain of $10,000 at the 28% rate, and Section 1250 gain of $56,000 at the 25% rate. -

Question 32:

On December 1, 1997, Krest, a self-employed cash basis taxpayer, borrowed $200,000 to use in her business. The loan was to be repaid on November 30, 1998. Krest paid the entire interest amount of $24,000 on December 1, 1997. What amount of interest was deductible on Krest's 1997 income tax return?

A. $0

B. $2,000

C. $22,000

D. $24,000 -

Question 33:

Smith made a gift of property to Thompson. Smith's basis in the property was $1,200. The fair market value at the time of the gift was $1,400. Thompson sold the property for $2,500. What was the amount of Thompson's gain on the disposition?

A. $0

B. $1,100

C. $1,300

D. $2,500 -

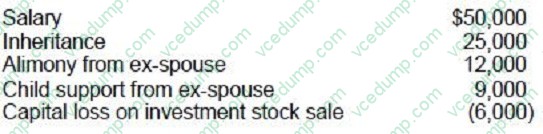

Question 34:

In the current year Jensen had the following items:

What is Jensen's AGI for the current year?

A. $44,000

B. $59,000

C. $62,000

D. $84,000 -

Question 35:

On December 1, 1992, Michaels, a self-employed cash basis taxpayer, borrowed $100,000 to use in her business. The loan was to be repaid on November 30, 1993. Michaels paid the entire interest of $12,000 on December 1, 1992. What amount of interest was deductible on Michaels' 1993 income tax return?

A. $12,000

B. $11,000

C. $1,000

D. $0 -

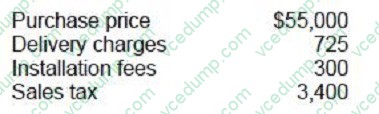

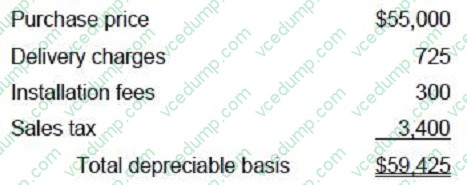

Question 36:

Starr, a self-employed individual, purchased a piece of equipment for use in Starr's business. The costs associated with the acquisition of the equipment were:

What is the depreciable basis of the equipment?

A. $55,000

B. $58,400

C. $59,125

D. $59,425 -

Question 37:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

The Moores received a stock dividend in 1994 from Ace Corp. They had the option to receive either cash or Ace stock with a fair market value of $900 as of the date of distribution. The par value of the stock was $500.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 -

Question 38:

Freeman, a single individual, reported the following income in the current year:

Guaranteed payment from services rendered to a partnership $50,000 Ordinary income from a S corporation $20,000

What amount of Freeman's income is subject to self-employment tax?

A. $0

B. $20,000

C. $50,000

D. $70,000 -

Question 39:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

Tom's 1994 wages were $53,000. In addition, Tom's employer provided group-term life insurance on Tom's life in excess of $50,000. The value of such excess coverage was $2,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 -

Question 40:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

In 1992, Joan received an acre of land as an inter-vivos gift from her grandfather. At the time of the gift, the land had a fair market value of $50,000. The grandfather's adjusted basis was $60,000. Joan sold the land in 1994 to an unrelated

third party for $56,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-REGULATION exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.