CPA-REGULATION Exam Details

-

Exam Code

:CPA-REGULATION -

Exam Name

:CPA Regulation -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:69 Q&As -

Last Updated

:Jul 14, 2026

Test Prep CPA-REGULATION Online Questions & Answers

-

Question 21:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

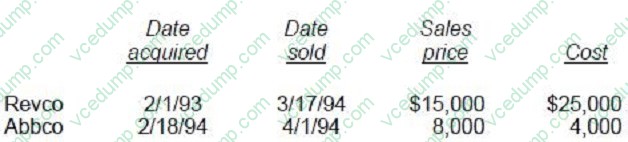

The Moores had no capital loss carryovers from prior years. During 1994, the Moores had the following stock transactions, which resulted in a net capital loss:

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 -

Question 22:

In evaluating the hierarchy of authority in tax law, which of the following carries the greatest authoritative value for tax planning of transactions?

A. Internal Revenue Code.

B. IRS regulations.

C. Tax court decisions.

D. IRS agents' reports. -

Question 23:

On February 1, 1993, Hall learned that he was bequeathed 500 shares of common stock under his father's will. Hall's father had paid $2,500 for the stock in 1990. Fair market value of the stock on February 1, 1993, the date of his father's death, was $4,000 and had increased to $5,500 six months later. The executor of the estate elected the alternate valuation date for estate tax purposes. Hall sold the stock for $4,500 on June 1, 1993, the date that the executor distributed the stock to him. How much income should Hall include in his 1993 individual income tax return for the inheritance of the 500 shares of stock, which he received from his father's estate?

A. $5,500

B. $4,000

C. $2,500

D. $0 -

Question 24:

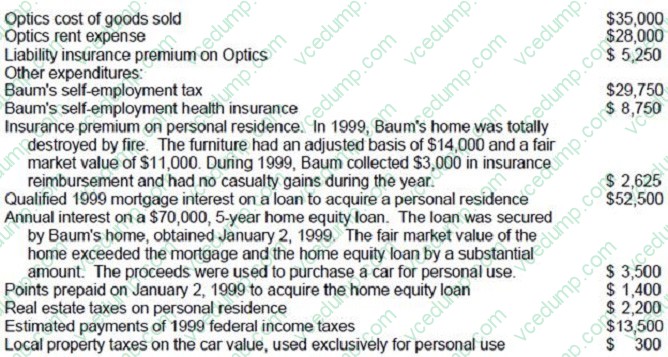

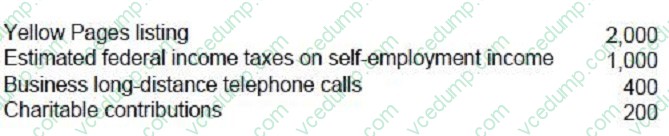

Baum, an unmarried optometrist and sole proprietor of Optics, buys and maintains a supply of eyeglasses and frames to sell in the ordinary course of business. In 1999, Optics had $350,000 in gross business receipts and its year-end

inventory was not subject to the uniform capitalization rules. Baum's 1999 adjusted gross income was $90,000 and Baum qualified to itemize deductions. During 1999, Baum recorded the following information:

Business expenses:

What amount should Baum report as 1999 net earnings from self-employment?

A. $243,250

B. $252,000

C. $273,000

D. $281,750 -

Question 25:

Rich is a cash basis self-employed air-conditioning repairman with 1993 gross business receipts of $20,000. Rich's cash disbursements were as follows:

What amount should Rich report as net self-employment income?

A. $15,100

B. $14,900

C. $14,100

D. $13,900 -

Question 26:

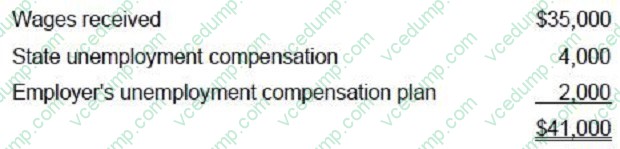

Porter was unemployed for part of the year. Porter received $35,000 of wages, $4,000 from a state unemployment compensation plan, and $2,000 from his former employer's company-paid supplemental unemployment benefit plan. What is the amount of Porter's gross income?

A. $35,000

B. $37,000

C. $39,000

D. $41,000 -

Question 27:

Dale received $1,000 in 1990 for jury duty. In exchange for regular compensation from her employer during the period of jury service, Dale was required to remit the entire $1,000 to her employer in 1990. In Dale's 1990 income tax return, the $1,000 jury duty fee should be:

A. Claimed in full as an itemized deduction.

B. Claimed as an itemized deduction to the extent exceeding 2% of adjusted gross income.

C. Deducted from gross income in arriving at adjusted gross income.

D. Included in taxable income without a corresponding offset against other income. -

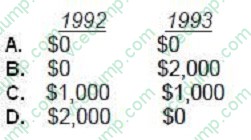

Question 28:

Smith, an individual calendar-year taxpayer, purchased 100 shares of Core Co. common stock for $15,000 on December 15, 1992, and an additional 100 shares for $13,000 on December 30, 1992. On January 3, 1993, Smith sold the shares purchased on December 15, 1992, for $13,000. What amount of loss from the sale of Core's stock is deductible on Smith's 1992 and 1993 income tax returns?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 29:

Greller owns 100 shares of Arden Corp., a publicly-traded company, which Greller purchased on January 1, 2001, for $10,000. On January 1, 2003, Arden declared a 2-for-1 stock split when the fair market value (FMV) of the stock was $120 per share. Immediately following the split, the FMV of Arden stock was $62 per share. On February 1, 2003, Greller had his broker specifically sell the 100 shares of Arden stock received in the split when the FMV of the stock was $65 per share. What is the basis of the 100 shares of Arden sold?

A. $5,000

B. $6,000

C. $6,200

D. $6,500 -

Question 30:

Adams owns a second residence that is used for both personal and rental purposes. During 2001,

Adams used the second residence for 50 days and rented the residence for 200 days. Which of the following statements is correct?

A. Depreciation may not be deducted on the property under any circumstances.

B. A rental loss may be deducted if rental-related expenses exceed rental income.

C. Utilities and maintenance on the property must be divided between personal and rental use.

D. All mortgage interest and taxes on the property will be deducted to determine the property's net income or loss.

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-REGULATION exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.