Test Prep Test Prep Certifications CPA-REGULATION Questions & Answers

Question 41:

Capital assets include:

A. A corporation's accounts receivable from the sale of its inventory.

B. Seven-year MACRS property used in a corporation's trade or business.

C. A manufacturing company's investment in U.S. Treasury bonds.

D. A corporate real estate developer's unimproved land that is to be subdivided to build homes, which will be sold to customers.

Correct Answer: C

Choice "c" is correct. Investment assets of a taxpayer that are not inventory are capital assets. The manufacturing company would have capital assets including an investment in U.S. Treasury bonds. Choice "a" is incorrect. Accounts receivable generated from the sale of inventory are excluded from the statutory definition of capital assets. Choice "b" is incorrect. Depreciable property used in a trade or business is excluded from the statutory definition of capital assets. Choice "d" is incorrect. Land is usually a capital asset, but when it is effectively inventory, as when it is used by a developer to be subdivided, it is excluded from the statutory definition of capital assets.

Question 42:

Leker exchanged a van that was used exclusively for business and had an adjusted tax basis of $20,000 for a new van. The new van had a fair market value of $10,000, and Leker also received $3,000 in cash. What was Leker's tax basis in the acquired van?

A. $20,000

B. $17,000

C. $13,000

D. $7,000

Correct Answer: B

Choice "b" is correct. $17,000 is the tax basis in the van. The basis for like-kind exchanges is computed as follows: The general rule is the gain is recognized to the extent boot is received. As the transaction results in a loss to Leker (he received an asset worth $10,000 plus $3,000 cash less a $20,000 tax basis equals $7,000 loss) no gain is recognized and the $3,000 received reduces his basis in the new asset. Choice "a" is incorrect. Basis must be reduced by non-like-kind assets (boot) received. Choice "c" is incorrect. For non-like-kind exchanges, the basis would be the FMV of the assets received ($10,000 FMV plus $3,000 Boot). However, because both assets have similar use, this is a like-kind exchange, which follows the rule above. Choice "d" is incorrect. The basis of the old property is used to calculate the basis of the new property, less any boot received.

Question 43:

Smith made a gift of property to Thompson. Smith's basis in the property was $1,200. The fair market value at the time of the gift was $1,400. Thompson sold the property for $2,500. What was the amount of Thompson's gain on the disposition?

A. $0

B. $1,100

C. $1,300

D. $2,500

Correct Answer: C

Choice "c" is correct. The general rule for the basis on gifted property is that the donee receives the property with a rollover cost basis (equal to the donor's basis). An exception exists where the fair market value of the property at the time of the gift is less than the donor's basis. That is not the case in this question; thus, the calculation of the gain on the disposition of the property is:

Choice "a" is incorrect. This choice could be correct if the facts of the question met the exception whereby no gain or loss is recognized when a donee sells gifted property for an amount between the donor's basis and the fair market value at the date of the gift. Choice "b" is incorrect. This choice uses the basis as the fair market value of the property. Fair market value of property at date of death is used as the basis for inherited property, not gifted property. Choice "d" is incorrect. This choice assumes that Thompson's basis is zero. His basis is $1,200 as indicated above.

Question 44:

Under the uniform capitalization rules applicable to taxpayers with property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions have been met?

A. Option A

B. Option B

C. Option C

D. Option D

Correct Answer: A

Choice "a" is correct. Direct material, direct labor, and factory overhead (applicable indirect costs) are

capitalized with respect to inventory under the uniform capitalization rules for property acquired for resale.

Applicable indirect costs include depreciation and amortization, insurance, supervisory wages, utilities,

spoilage and scrap, design expenses, repair and maintenance and rental of equipment and facilities

(including offsite storage), some administrative costs, costs of bonus and other incentive plans, and

indirect supplies and other materials (including repackaging costs).

Choices "b", "c", and "d" are incorrect, per the above discussion.

Question 45:

Which of the following is subject to the Uniform Capitalization Rules of Code Sec. 263A?

A. Editorial costs incurred by a freelance writer.

B. Research and experimental expenditures.

C. Mine development and exploration costs.

D. Warehousing costs incurred by a manufacturing company with $12 million in annual gross receipts.

Correct Answer: D

Choice "d" is correct. Uniform capitalization rules apply to the following: (1) real or tangible personal property produced by the taxpayer for use in his or her trade or business; (2) real or tangible personal property produced by the taxpayer for sale to his or her customers; and (3) real or tangible personal property acquired by the taxpayer for resale, provided the taxpayer's annual average gross receipts for the preceding three years exceeds $10,000,000. Warehousing costs incurred by a manufacturing company (making inventory for sale to its customers) are subject to the Uniform Capitalization Rules. Further, they are the only item on the list that is real or tangible personal property. In this case, the inventory is not acquired for resale (it is produced by the taxpayer for sale to his or her customers), so the fact that the annual sales are $12,000,000 does not matter in this case. The sales could have been less than $10,000,000 annually, and the Uniform Capitalization Rules would still have applied. Choices "a", "b", and "c" are incorrect, based on the above discussion.

Question 46:

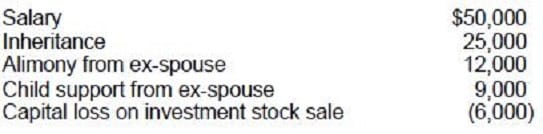

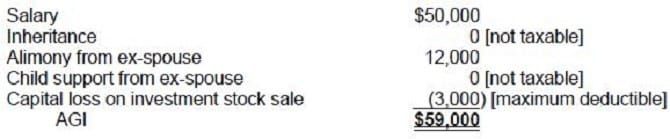

In the current year Jensen had the following items:

What is Jensen's AGI for the current year?

A. $44,000

B. $59,000

C. $62,000

D. $84,000

Correct Answer: B

Choice "b" is correct. The question asks for AGI, but all of the items in the list are items of potential gross income. There are no adjustments included in the list; therefore, in this case, AGI is the same as gross income. The calculation is as follows:

Choices "a", "c", and "d" are incorrect, per the above calculation.

Question 47:

Which one of the following will result in an accruable expense for an accrual-basis taxpayer?

A. An invoice dated prior to year end but the repair completed after year end.

B. A repair completed prior to year end but not invoiced.

C. A repair completed prior to year end and paid upon completion.

D. A signed contract for repair work to be done and the work is to be completed at a later date.

Correct Answer: B

RULE: An accruable expense is one is which the services have been received/performed but have not been paid for by the end of the reporting period.

Choice "b" is correct. The facts indicate that a repair was completed prior to year end but not yet invoiced. If it has not yet been invoiced, it is assumed that it has also not yet been paid for. Therefore, this is a situation in which the repair expense would be accrued at year end. Services have been performed, but they have not been paid for, as they have not even been invoiced yet. Choice "a" is incorrect. If the repair was completed after year end, then the expense is not accruable, as the benefit of the services hasn't been received as of year end. The fact that the repair was invoiced prior to year end does not impact the situation. Choice "c" is incorrect. If a repair was completed and paid for prior to year end, no accrual is appropriate. On the accrual basis, the expense is taken in the year the repair is completed and the benefit is received. In this case, the account payable was also paid in the same year, but this has no effect on the expense. Choice "d" is incorrect. The facts indicate that the work is to be completed at a date later than year end. Therefore, the expense is not accruable at year end, as the benefit of the repair hasn't been received as of year end. It is reasonable that a signed contract for the repair work exists, but this has no effect on the accrual.

Question 48:

Porter was unemployed for part of the year. Porter received $35,000 of wages, $4,000 from a state unemployment compensation plan, and $2,000 from his former employer's company-paid supplemental unemployment benefit plan. What is the amount of Porter's gross income?

A. $35,000

B. $37,000

C. $39,000

D. $41,000

Correct Answer: D

RULE: Gross income includes all income unless it is specifically excluded in the tax code.

Choice "d" is correct. Wages and all unemployment compensation are not excluded from being taxable;

therefore, there are included in the taxpayer's gross income for tax purposes.

Choice "a" is incorrect. All forms of unemployment compensation are included as part of gross income. Choice "b" is incorrect. The $4,000 of state unemployment compensation received is included as part of gross income. Choice "c" is incorrect. The $2,000 of his former employer's company-paid supplemental unemployment benefit plan is included as part of gross income.

Question 49:

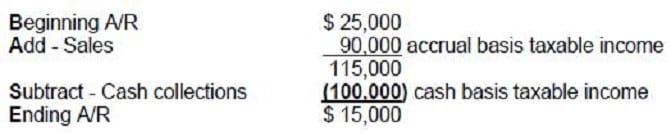

Mosh, a sole proprietor, uses the cash basis of accounting. At the beginning of the current year, accounts receivable were $25,000. During the year, Mosh collected $100,000 from customers. At the end of the year, accounts receivable were $15,000. What was Mosh's gross taxable income for the current year?

A. $75,000

B. $90,000

C. $100,000

D. $110,000

Correct Answer: C

Choice "c" is correct. The facts state that cash collections from customers were $100,000 and as a cash basis taxpayer this is the amount of Mosh's gross taxable income for the year. Note that according to the formula BASE - we can determine the amount of sales = $90,000, but that would give us accrual, not cash basis, income.

Choice "a" is incorrect. See explanation above.

Choice "b" is incorrect. $90,000 is the amount of sales that would be Mosh's taxable income if Mosh were

an accrual basis taxpayer.

Choice "d" is incorrect. See explanation above.

Question 50:

DAC Foundation awarded Kent $75,000 in recognition of lifelong literary achievement. Kent was not required to render future services as a condition to receive the $75,000. What condition(s) must have been met for the award to be excluded from Kent's gross income?

I. Kent was selected for the award by DAC without any action on Kent's part.

II.

Pursuant to Kent's designation, DAC paid the amount of the award either to a governmental unit or to a charitable organization.

A.

I only.

B.

II only.

C.

Both I and II.

D.

Neither I nor II.

Correct Answer: C

Choice "c" is correct. Generally, the fair market value of prizes and awards is taxable income. However, an

exclusion from income for certain prizes and awards applies where the winner is selected for the award

without entering into a contest (i.e., without any action on their part) and then assigns the award directly to

a governmental unit or charitable organization. Therefore, conditions "I" and "II" must be met in order for

Ken to exclude the award from his gross income.

Choice "a" is incorrect. "II" is a necessary condition as well. See explanation above.

Choice "b" is incorrect. "I" is a necessary condition as well. See explanation above.

Choice "d" is incorrect. "I" and "II" are both necessary conditions. See explanation above.

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-REGULATION exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.