IMANET-CMA Exam Details

-

Exam Code

:IMANET-CMA -

Exam Name

:Certified Management Accountant (CMA) -

Certification

:IMANET Certifications -

Vendor

:IMANET -

Total Questions

:1336 Q&As -

Last Updated

:May 24, 2026

IMANET IMANET-CMA Online Questions & Answers

-

Question 161:

A manufacturing arrangement characterized by low or no setup times and the ability to switch quickly from producing one product to another is called a

A. Just-in-time manufacturing system.

B. Computer-integrated manufacturing system.

C. Flexible manufacturing system.

D. Robot. -

Question 162:

In general, it is more expensive for a company to finance with equity capital than with debt capital because

A. Long-term bonds have a maturity date and must therefore be repaid in the future

B. Investors are exposed to greater risk with equity capital.

C. Equity capital is in greater demand than debt capital

D. Dividends fluctuate to a greater extent than interest rates -

Question 163:

When a firm finances each asset with a financial instrument of the same approximate maturity as the life of the assets, it is applying

A. Working capital management

B. Return maximization

C. Financial leverage

D. A hedging approach -

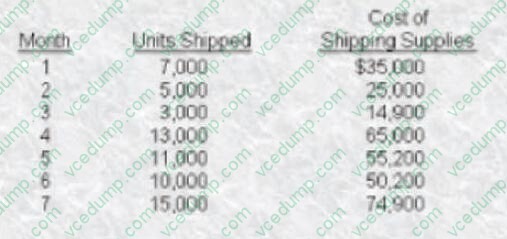

Question 164:

The following data were collected from the records of the shipping department of a company:

The cost of shipping supplies is most likely to be a

A. Variable cost.

B. Fixed cost.

C. Step cost.

D. Semi-fixed cost. -

Question 165:

All of the following are alternative marketable securities suitable for investment except

A. U.S.Treasurjbills.

B. Eurodollars.

C. Commercial paper.

D. Convertible bonds. -

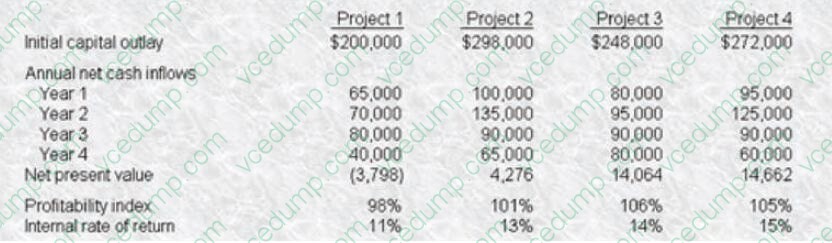

Question 166:

Capital Invest, Inc. uses a 12% hurdle rate for all capital expenditures and has done the following analysis for four projects for the upcoming year:

Which project(s) should Capital Invest, Inc. undertake during the upcoming year if it has only $300,000 of capital funds available?

A. Project 1. B. Projects 2, 3, and 4.

C. Projects 3 and 4.

D. Project 3. -

Question 167:

The prime lending rate of commercial banks is an announced rate and is often understated from the viewpoint of even the most credit-worthy firms. Which one of the following requirements always results in a higher effective interest rate?

A. A floating rate for the loan period

B. A covenant that restricts the issuance of any new unsecured bonds during the existence of the loan.

C. The imposition of a compensating balance with an absolute minimum that cannot be met by current transaction balances.

D. The absence of a charge for any unused portion in the line of credit. -

Question 168:

What s the weighted average cost of capital for a firm with equal amounts of debt and equity financing, a 15% before-tax company cost of equity capital, a 35% tax rate, and a 12% coupon rate on its debt that is selling at par value?

A. 8.775%

B. 9.60%

C. 11.40% D 13. 50% -

Question 169:

An increase in sales resulting from an increased cash discount for prompt payment would be expected to cause

A. An increase in the operating cycle.

B. An increase in the average collection period.

C. A decrease in the cash conversion cycle.

D. A decrease in purchase discounts taken. -

Question 170:

Speech Co.'s budgeted sales and budgeted cost of sales for the coming year are $212,000,000 and $132,500,000, respectively. Short-term interest rates are expected to average 5%. If Speech could increase inventory turnover from its current 8.0 times permeate 10.0 times per year, its expected cost savings in the current year would be

A. $165,625

B. $0

C. $3,312,500

D. $828,125

Related Exams:

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only IMANET exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your IMANET-CMA exam preparations and IMANET certification application, do not hesitate to visit our Vcedump.com to find your solutions here.