IMANET-CMA Exam Details

-

Exam Code

:IMANET-CMA -

Exam Name

:Certified Management Accountant (CMA) -

Certification

:IMANET Certifications -

Vendor

:IMANET -

Total Questions

:1336 Q&As -

Last Updated

:May 24, 2026

IMANET IMANET-CMA Online Questions & Answers

-

Question 181:

Without prejudice to your answers from any other questions, assume that the after-tax cost of debt financing is 10%. the cost of retained earnings is 14%. and the cost of new common stock is 16%. What is the marginal cost of capital to - FLF Corporation for any projected capital expansion in excess of $7 million?

A. 10%

B. 12. 74%

C. 136%

D. 16% -

Question 182:

Clay Co. has considerable excess manufacturing capacity. A special job order's cost sheet includes the following applied manufacturing overhead costs: Fixed costs $21,000 Variable costs 33,000

The fixed costs include a normal $3,700 allocation for in-house design costs, although no in-house design will be done. Instead, the job will require the use of external designers costing $7,750. What is the total amount to be included in the calculation to determine the minimum acceptable price for the job?

A. $36,700

B. $40,750

C. $54,000

D. $58,050 -

Question 183:

A firm must select from among several methods of financing arrangements when meeting its capital requirements. To acquire additional growth capital while attempting to maximize earnings per share, a firm should normally

A. Attempt to increase both debt and equate in equal proportions, which preserves a stable capital structure and maintains investor confidence.

B. Select debt over equity' initially, even though increased debt is accompanied by interest costs and a degree of risk.

C. Select equity over debt initially, which minimizes risk and avoids interest costs.

D. Discontinue dividends and use current cash flow, which avoids the cost and risk of increased debt and the dilution of EPS through increased equity. -

Question 184:

A retail company determines its selling price by marking up variable costs 60%. In addition, the company uses frequent selling price markdowns to stimulate sales. If the markdowns average 10%, what is the company's contribution margin ratio?

A. 27. 5%

B. 30.6%

C. 37. 5%

D. 41.7% -

Question 185:

Mercosul is a free-trade agreement among South American nations, What two nations are on associate members?

A. Bolivia and Chile.

B. Argentina and Boliria.

C. Argentina and Chile.

D. Argentina and Paraguay. -

Question 186:

Internal factors that influence the prices charged include

A. Price sensitivity.

B. Desire for market-share leadership.

C. Price elasticity.

D. Competitors' capacity. -

Question 187:

The sum of the costs necessary to effect a one-unit increase in the activity level is a(n)

A. Differential cost.

B. Opportunity cost.

C. Marginal cost.

D. Incremental cost. -

Question 188:

All of the following statements in regard to working capital are true except A. Current liabilities are an important source of financing for many small firms.

B. Profitability varies inversely with liquid dilly.

C. The hedging approach to financing involves matching maturities of debt with specific financing needs.

D. Financing permanent inventory buildup with long-term debt is an example of an aggressive working capital policy.

Correct Answer. D -

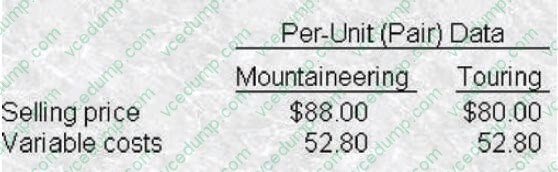

Question 189:

Siberian Ski Company recently expanded its manufacturing capacity, which will allow it to produce up to 15,000 pairs of cross country' skis of the mountaineering model or the touring model. The Sales Department assures management that it can sell between 9.000 pairs and 13,000 pairs of either product this year. Because the models are very similar, Siberian Ski will produce only one of the two models. The following information was compiled by the Accounting Department:

Fixed costs will total $369600 if the mountaineering model is produced but will be only $316,800 if the touring model is produced. Siberian Ski is subject to a 40% income tax rate.If Siberian Ski Company desires an after-tax net income of $24,000, how many pairs of touring model skis will the company have to sell?

A. 13,118pairs.

B. 12,529 pairs.

C. 13,853 pairs.

D. 4,460 pairs. -

Question 190:

Materials requrements planning (MRP)sometimes results in

A. Longer idle periods

B. Less flexibility in responding to custoemrs

C. increased inventory carrying costs

D. Decreased setup costs

Related Exams:

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only IMANET exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your IMANET-CMA exam preparations and IMANET certification application, do not hesitate to visit our Vcedump.com to find your solutions here.