IMANET-CMA Exam Details

-

Exam Code

:IMANET-CMA -

Exam Name

:Certified Management Accountant (CMA) -

Certification

:IMANET Certifications -

Vendor

:IMANET -

Total Questions

:1336 Q&As -

Last Updated

:May 24, 2026

IMANET IMANET-CMA Online Questions & Answers

-

Question 151:

The Sommers Company manufactures a van ely of industrial valves. Currently, the company is operating at about 70% capacity and is earning a satisfactory return on investment, Management has been approached by Glascow Industries Ltd of Scotland with an offer to buy 120.000 units of a pressure valve. Glascow manufactures a valve that is almost identical to Sommers' pressure valve however, a fire in Glascow industries valve plant has shut down its manufacturing operations. Glascow needs the 120.000 valves over the next 4 months to meet commitments to its regular customers, the company is prepared to pay $19 each for the valves, FOB shipping point. Sommers' product cost, based on current attainable standards, for the pressure valve is

Manufacturing overhead is applied to production at the rate of $18 per standard direct labor hour This overhead rate is made up of the following components

What is the incremental profit (loss) before tax associated with the Glascow order?

A. ($168,000)

B. ($120,000)

C. $552,000

D. $600000 -

Question 152:

The frame Supply Company has just acquired a large account and needs to increase its working capital by $100,000. The controller of the company has identified the four sources of funds given below.

1. Pay a factor to buy the company's receivable, which average $125,000 per month and have an average collection period of 30 days. The factor will advance u to 80% of the face value of receivables at 10% and charge a fee of 2%.

2. Borrow $110,000 from a bank at 12% interest. A 9% compensating balance would be required.

3. Issue $110,000 of 6-month commercial paper to net $100,000 (New paper would be issued every 6 months.)

4. Borrow $125,000 from a bank on a discount basis at 20%. No compensating balance would be required. Assume a 360-day year in all of your calculations. The cost of Alternative 2. to Frame Supply Company is

A. 9.0%

B. 12. 0%

C. 13. 2%

D. 21.0% -

Question 153:

Marston Enterprises sells three chemicals: petrol, septine, and tridol. Petrol is the company's most profitable product tridol is the least profitable. Which one of the following events will definitely decrease the firm's overall breakeven point for the upcoming accounting period?

A. The installation of new computer-controlled machinery and subsequent layoff of assembly-line workers.

B. A decrease in tridol's selling price.

C. An increase in the overall market for septine.

D. An increase in anticipated sales of petrol relative to sales of septine and tridol. -

Question 154:

In an organization with empowered work teams, organizational policies

A. Should define the limits or constraints within which the work teams must act if they are to remain self-directing.

B. Become more important than ever. Without clear rules to follow, empowered work reams are almost certain to make mistakes.

C. Should be few or none. The work reams should have the freedom to make their own decisions.

D. Should be set by the teams themselves in periodic joint meetings. -

Question 155:

Which one of the following statements is true when comparing bond financing alternatives?

A. A bond with a call provision typically has a lower yield to maturity than a similar bond without a call provision.

B. A convertible bond must be converted to common stock prior to its maturity.

C. A call provision is generally considered detrimental to the investor.

D. A call premium requires the investor to pay an amount greater than par at the time of purchase. -

Question 156:

The risk that securities cannot be sold ate reasonable price on short notice is called

A. Default risk.

B. Interest-rate risk.

C. Purchasing-power risk.

D. Liquidly risk. -

Question 157:

Average daily collection of checks for a firm is $40,000.The firm also writes on the average $35,000 of checks daily. If the collection period for checks is 5 days, calculate the net float.

A. $25,000

B. $40,000

C. $175,000

D. $200,000 -

Question 158:

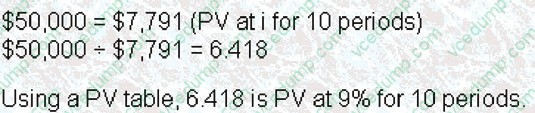

Pena Company is considering a project that calls for an initial cash outlay of $50,000. The expected net cash inflows from the project are $7,791 for each of 10 years. What is the PR of the project?

A. 6%

B. 7%

C. 8%

D. 9% -

Question 159:

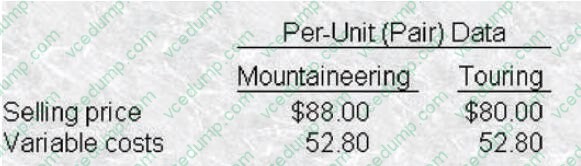

Siberian Ski Company recently expanded its manufacturing capacity, which will allow it to produce upto 15,000 pairs of cross country skis of the mountaineering model or the touring model. The Sales Department assures management that it can sell between 9,000 pairs and 13000 pairs of either product this year. Because the models are very similar, Siberian Ski will produce only one of the two models. The following information was compiled by the Accounting Department

Fixed costs will total $369,600 if the mountaineering model is produced but will be only $316,800 if the touring model is produced. Siberian Ski is subject to a 40% income tax rate.If the Siberian Ski Company Sales Department could guarantee the annual sale of 12,000 pairs of either model, Siberian Ski would

A. Produce 12,000 pairs of touring skis because they have a lowerfixed cost.

B. Be indifferent as to which model is sold because each model has the same variable cost per unit.

C. Produce 12,000 pairs of mountaineering skis because they have a lower breakeven point.

D. Produce 12,000 pairs of mountaineering skis because they are more profitable. -

Question 160:

RLE Corporation had income before taxes of $60,000 for the year. Included in this amount were depreciation of $5,000, a charge of $6,000 for the amortization of bond discounts, and $4,000 for interest expense. The estimated cash flow for the period is

A. $60000

B. $66,000

C. $49000

D. $71000

Related Exams:

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only IMANET exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your IMANET-CMA exam preparations and IMANET certification application, do not hesitate to visit our Vcedump.com to find your solutions here.