CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 991:

When an accountant examines a financial forecast that fails to disclose several significant assumptions used to prepare the forecast, the accountant should describe the assumptions in the accountant's report and issue a (an):

A. "Except for" qualified opinion.

B. "Subject to" qualified opinion.

C. Unqualified opinion with a separate explanatory paragraph.

D. Adverse opinion. -

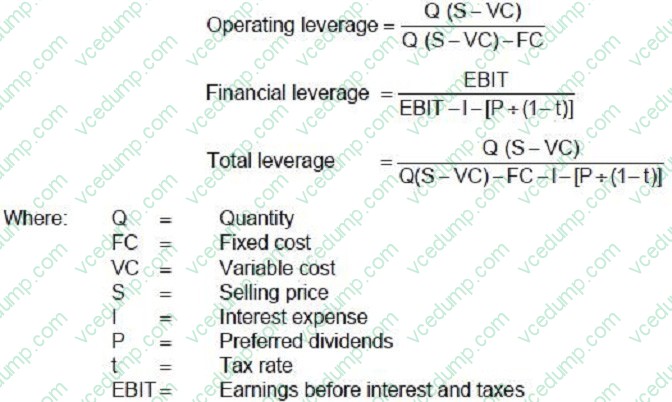

Question 992:

ABC Company presently sells 400,000 bottles of perfume each year. Each bottle costs $.84 to produce and sells for $1.00. Fixed costs are $28,000 per year. The firm has annual interest expense of $6,000, preferred stock dividends of $2,000 per year, and a 40 percent tax rate. ABC uses the following formulas to determine the company's leverage.

If ABC Company did not have preferred stock, the degree of total leverage would:

A. Decrease in proportion to a decrease in financial leverage.

B. Increase in proportion to an increase in financial leverage.

C. Decrease but not be proportional to the decrease in financial leverage.

D. Decrease but not have an effect on financial leverage. -

Question 993:

An auditor ordinarily sends a standard confirmation request to all banks with which the client has done business during the year under audit, regardless of the year-end balance. A purpose of this procedure is to:

A. Provide the data necessary to prepare a proof of cash.

B. Request a cutoff bank statement and related checks be sent to the auditor.

C. Detect kiting activities that may otherwise not be discovered.

D. Seek information about contingent liabilities and security agreements. -

Question 994:

Which of the following sets of information does an auditor usually confirm on one form?

A. Accounts payable and purchase commitments.

B. Cash in bank and collateral for loans.

C. Inventory on consignment and contingent liabilities.

D. Accounts receivable and accrued interest receivable. -

Question 995:

Which one of the following is not a key assumption of perfect competition?

A. Customers are indifferent about which firm they buy from.

B. The level of a firm's output is small relative to the industry's total output.

C. Each firm can price its product above the industry price.

D. There is freedom of entry into and exit out of the industry. -

Question 996:

A firm's target or optimal capital structure is consistent with which one of the following?

A. Minimum cost of debt.

B. Minimum risk.

C. Minimum cost of equity.

D. Minimum weighted average cost of capital. -

Question 997:

Heather, Erika, and Shelby are members in ABC LLC. Heather dies. Absent an agreement to the contrary, what is the result?

A. The LLC must dissolve.

B. The LLC ceases to exist.

C. The LLC is dissolved unless the other members consent to continue.

D. The LLC continues as though nothing happened. -

Question 998:

Which one of the following responses is not an advantage to a corporation that uses the commercial paper market for short-term financing?

A. The borrower avoids the expense of maintaining a compensating balance with a commercial bank.

B. There are no restrictions as to the type of corporation that can enter into this market.

C. This market provides a broad distribution for borrowing.

D. A benefit accrues to the borrower because its name becomes more widely known. -

Question 999:

Which of the following is not a reason justifying the use of accounting estimates?

A. The valuation or measurement of some accounts is uncertain pending the outcome of future events.

B. Data about past events cannot be accumulated in a cost-effective manner.

C. Data about future events cannot be accumulated in a cost-effective manner.

D. Data about past events cannot be accumulated in a timely manner. -

Question 1000:

ABC Corp. owned a restaurant called XYZ. The corporation president, T.J. Jones, hired a contractor to make repairs at the restaurant, signing the contract, "T.J. Jones for XYZ." Two invoices for restaurant repairs were paid by ABC Corp. with corporate checks. Upon presenting the final invoice, the contractor was told that it would not be paid. The contractor sued ABC Corp. Which of the following statements is correct regarding the liability of ABC Corp.?

A. It is not liable because Jones is liable.

B. It is not liable because the corporation was an undisclosed principal.

C. It is liable because Jones is not liable.

D. It is liable because Jones had authority to make the contract.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.