CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 611:

Which of the following statements is correct concerning liability when a partner in a general partnership commits a tort while engaged in partnership business?

A. The partner committing the tort is the only party liable.

B. The partnership is the only party liable.

C. Each partner is jointly and severally liable.

D. Each partner is liable to pay an equal share of any judgment. -

Question 612:

Cobb, Inc., a partner in TLC Partnership, assigns its partnership interest to Bean, who is not made a partner. After the assignment, Bean asserts the rights to:

A. Participate in the management of TLC. II. Cobb's share of TLC's partnership profits. Bean is correct as to which of these rights?

B. I only.

C. II only.

D. I and II.

E. Neither I nor II. -

Question 613:

The kinked demand curve is associated with:

A. The analysis of agricultural markets.

B. The analysis of monopolistic competition.

C. The analysis of pure competition.

D. The analysis of oligopoly. -

Question 614:

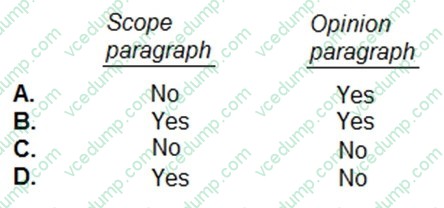

When disclaiming an opinion due to a client-imposed scope limitation, an auditor should indicate in a separate paragraph why the audit did not comply with generally accepted auditing standards. The auditor should also omit the:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 615:

ABC Corp.'s trial balance of Income Statement Accounts for the year ended December 31, 1988 as follows:

ABC's income tax rate is 30%. The gain on debt extinguishment is considered a usual and recurring part of ABC's operations. The hurricane is considered an unusual and infrequent event. ABC prepares a multiple- step income statement for

1988.

Net income is:

A. $140,000

B. $161,000

C. $168,000

D. $200,000 -

Question 616:

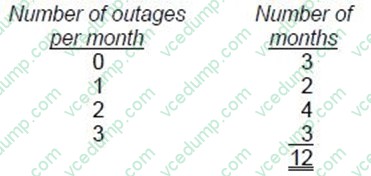

During 1994, ABC Corp. experienced the following power outages:

Each power outage results in out-of-pocket costs of $400. For $500 per month, ABC can lease an auxiliary generator to provide power during outages. If ABC leases an auxiliary generator in 1995, the estimated savings (or additional

expenditures) for 1995 would be:

A. ($3,600)

B. ($1,200)

C. $1,600

D. $1,900 -

Question 617:

Which of the following is a true statement regarding documentation requirements for analytical procedures?

A. When an analytical procedure is used as the principal substantive test of a significant financial statement assertion, the auditor is required to document the reasons analytical procedures were performed instead of tests of details.

B. When an analytical procedure is used as the principal substantive test of a significant financial statement assertion, the auditor is required to document his or her expectation and management's concurrence with that expectation.

C. When an analytical procedure is used during the overall review stage of the audit, the auditor is required to document the auditor's expectation and any additional procedures performed to investigate significant unexplained differences.

D. When an analytical procedure is used as the principal substantive test of a significant financial statement assertion, the auditor is required to document both the auditor's expectation and the factors considered in developing that expectation. -

Question 618:

Which of the following factors most likely would lead a CPA to conclude that a potential audit engagement should be rejected?

A. The details of most recorded transactions are not available after a specified period of time.

B. Internal control activities requiring the segregation of duties are subject to management override.

C. It is unlikely that sufficient appropriate evidence is available to support an opinion on the financial statements.

D. Management has a reputation for consulting with several accounting firms about significant accounting issues. -

Question 619:

In an audit of contingent liabilities, which of the following procedures would be least effective?

A. Reviewing a bank confirmation letter.

B. Examining customer confirmation replies.

C. Examining invoices for professional services.

D. Reading the minutes of the board of directors. -

Question 620:

An auditor was engaged to conduct a performance audit of a governmental entity in accordance with Government Auditing Standards. These standards do not require, as part of this auditor's report:

A. A statement of the audit objectives and a description of the audit scope.

B. Indications or instances of illegal acts that could result in criminal prosecution discovered during the audit.

C. The pertinent views of the entity's responsible officials concerning the auditor's findings.

D. A concurrent opinion on the financial statements taken as a whole.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.