AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 591:

When auditing an entity's financial statements in accordance with Government Auditing Standards (the Yellow Book), an auditor is required to report on:

A. Recommendations for actions to improve operations. II. The scope of the auditor's tests of compliance with laws and regulations. B. I only. C. II only. D. Both I and II. E. Neither I nor II.

B. I only. Choice "b" is correct. When auditing an entity's financial statements in accordance with Government Auditing Standards, an auditor is required to report on the scope of the auditor's testing of compliance with laws and regulations, but not on recommendations for actions to improve operations. Choices "a", "c", and "d" are incorrect based on the above Explanation.

Question 592:

Net working capital is the difference between:

A. Current assets and current liabilities. B. Fixed assets and fixed liabilities. C. Total assets and total liabilities. D. Total assets and current liabilities.

A. Current assets and current liabilities. Choice "a" is correct. Current assets minus current liabilities equals net working capital. Choices "b", "c", and "d" are incorrect, per the above Explanation.

Question 593:

An individual had the following capital gains and losses for the year:

What will be the net gain (loss) reported by the individual and at what applicable tax rate(s)?

A. Long-term gain of $16,000 at the 15% rate. B. Short-term loss of $3,000 at the ordinary rate and long-term capital gain of $86,000 at the 15% rate. C. Long-term capital gain of $3,000 at the 15% rate, collectibles gain of $10,000 at the 28% rate, and Section 1250 gain of $56,000 at the 25% rate. D. Short-term loss of $3,000 at the ordinary rate, long-term capital gain of $10,000 at the 15% rate, collectibles gain of $10,000 at the 28% rate, and Section 1250 gain of $56,000 at the 25% rate.

A. Long-term gain of $16,000 at the 15% rate. Choice "a" is correct. Specific netting procedures for capital gains and losses are outlined in the Internal Revenue Code for non-corporate taxpayers. Gains and losses are netted within each tax rate group (e.g., the 15% rate group). The facts of this question have already performed this step for us. Short-term Capital Gains and Losses 1. If there are any short-term capital losses (this includes any short-term capital loss carryovers), they are first offset against any short-term gains that would be taxable at the ordinary income rates. 2. Any remaining short-term capital loss is used to offset any long-term capital gains from the 28% grate group (e.g., collectibles). 3. Any remaining short-term capital loss is then used to offset any long-term gains from the 25% group (e.g., un-recaptured Section 1250 gains). 4. Any remaining short-term capital loss is used to offset any long-term capital gains applicable at the lower (e.g., 15%) tax rate. Long-term Capital Gains and Losses 1. If there are any long-term capital losses (this includes any long-term capital loss carryovers) from the 28% rate group, they are first offset against any net gains from the 25% rate group and then against net gains from the 15% rate group. 2. If there are any long-term capital losses (this includes any long-term capital loss carryovers) from the 15% rate group, they are offset first against any net gains from the 28% rate group and then against net gains from the 25% rate group. In this case, we are given net short-term capital losses of $70,000 to start with. Following the rules above, this first goes to offset any short-term gains at the ordinary income rates, but there are none in the facts. So, the next step is to offset the losses against any 28% rate gain long-term capital gains. The facts provide that there is $10,000 in gains from collectibles (taxable at the 28% rate). The remaining short-term loss ($60,000) is next used to offset the long-term capital gains at the 25% rate. The facts give us un- recaptured Section 1250 gains of $56,000 (taxed at the 25% tax rate). The remaining short-term capital loss is $4,000 ($70,000 - $10,000 - $56,000 = $4,000). The balance of the short-term capital losses is finally used to offset any capital gains taxed at the 15% tax rate, which the facts give us as $20,000. Therefore, after the $4,000 remaining short-term capital loss is applied to offset the $20,000 long-term capital gain taxed at the 15% tax rate, there is an amount of $16,000 remaining of long-term capital losses to be taxed at the 15% tax rate. Choices "b", "c", and "d" are incorrect, per the ordering rules discussed above.

Question 594:

The use of an accelerated method instead of the straight-line method of depreciation in computing the net present value of a project has the effect of:

A. Raising the hurdle rate necessary to justify the project. B. Lowering the net present value of the project. C. Increasing the present value of the depreciation tax shield. D. Increasing the cash outflows at the initial point of the project.

C. Increasing the present value of the depreciation tax shield. Explanation Explanation/Reference:Rule: The greater the depreciation expense, the greater the depreciation tax shield. Deprecation Tax Shield = Depreciation Expense ?Marginal Tax Rate Choice "c" is correct. Use of an accelerated method instead of the straight-line method of depreciation in computing the NPV of a project has the effect of increasing the PV of the deprecation tax shield. Choice "a" is incorrect. Depreciation method does not affect the hurdle rate. The hurdle rate is independently selected by management. Choice "b" is incorrect. Using an accelerated method instead of the straight-line method of depreciation will increase the present value of the deprecation tax shield and therefore increase the net present value of the project. Choice "d" is incorrect. Depreciation method does not affect cash outflows at the initial point of the project.

Question 595:

Davis, a director of ABC Corp., is entitled to:

A. Serve on the board of a competing business. B. Take sole advantage of a business opportunity that would benefit ABC. C. Rely on information provided by a corporate officer. D. Unilaterally grant a corporate loan to one of ABC's shareholders.

C. Rely on information provided by a corporate officer. Choice "c" is correct. As a director of the corporation, Davis may rely on information provided to him/her by a corporate officer. A corporate director is under no obligation to verify information given to him by management (corporate officers). Choice "a" is incorrect. A director is not entitled to serve on the board of a competing business. Doing so would be a breach of fiduciary duty. Choice "b" is incorrect. A director may not take sole advantage of a business opportunity that would benefit the corporation. Doing so would be a breach of fiduciary duty. Choice "d" is incorrect. A director may not unilaterally grant a corporate loan to one of the corporation's shareholders. Directors generally must act through a majority vote at a directors' meeting.

Question 596:

Cooper, CPA, believes there is substantial doubt about the ability of ABC Corp. to continue as a going concern for a reasonable period of time. In evaluating ABC's plans for dealing with the adverse effects of future conditions and events, Cooper most likely would consider, as a mitigating factor, ABC's plans to:

A. Discuss with lenders the terms of all debt and loan agreements. B. Strengthen internal controls over cash disbursements. C. Purchase production facilities currently being leased from a related party. D. Postpone expenditures for research and development projects.

B. Strengthen internal controls over cash disbursements. Choice "d" is correct. When assessing management's plans for dealing with the adverse effects of future conditions and events, mitigating factors would include: 1. The postponement of expenditures (including RandD), 2. Plans to dispose of assets, 3. Plans to borrow money or restructure debt, 4. Plans to increase ownership equity (sell stock). Choice "a" is incorrect. Discussions with lenders regarding terms would not be a mitigating factor. Actual agreements regarding restructuring of debt or amendments to covenants would be required. Choice "b" is incorrect. Strengthening internal controls over cash would not qualify as a management tactic to address going concern issues. Choice "c" is incorrect. Purchasing facilities which are currently being leased would only further decrease cash flow.

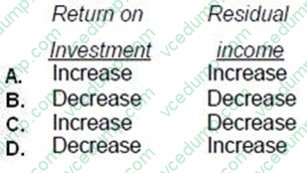

Question 597:

ABC, Inc. purchased a long-term asset on the last day of the current year. What are the effects of this purchase on return on investment and residual income?

A. Option A B. Option B C. Option C D. Option D

B. Option B Choice "b" is correct. The addition of an asset at year end serves to reduce both return on investment and residual income. The addition of an asset increases then denominator in the ROI computation and increases the threshold earnings required using the residual income approach. Both measures would suffer as a result of addition of assets. See illustration below: The purchase of the additional asset reduces ROI from 10% to 8% and produces negative residual income. Choices "a", "c", and "d" are incorrect, per the above illustration.

Question 598:

In competitive markets, an increase in demand for a product causes a(n):

A. Increase in product supply. B. Reduction in purchases by consumers. C. Reduction in the number of buyers of the product. D. Increase in the price of the product.

D. Increase in the price of the product. Rule of economic reasoning: "Draw the graph!" Choice "d" is correct. When demand increases and supply has not increased (as implied by the question), suppliers will raise the price of the product and more product will be bought (but the supply curve does not change). Because consumers are demanding more product than is available, they are "willing" to pay a higher price. Choice "a" is incorrect. Although buyers would pay higher prices and purchase more products, the supply "curve" has not changed. Therefore, the quantity supplied remains the same. Choice "b" is incorrect. Because consumer demand has increased (not decreased). Choice "c" is incorrect. An increase in demand has an indeterminate (and irrelevant) impact on the number of buyers. For example, there could be the same number of buyers in the market, but that each demands a higher quality.

Question 599:

Which of the following procedures would an auditor most likely perform in searching for unrecorded liabilities?

A. Vouch a sample of accounts payable entries recorded just before year-end to the unmatched receiving report file. B. Compare a sample of purchase orders issued just after year-end with the year-end accounts payable trial balance. C. Vouch a sample of cash disbursements recorded just after year-end to receiving reports and vendor invoices. D. Scan the cash disbursements entries recorded just before year-end for indications of unusual transactions.

C. Vouch a sample of cash disbursements recorded just after year-end to receiving reports and vendor invoices. Choice "c" is correct. The auditor is able to detect liabilities not recorded at year-end by comparing cash payments made after the balance sheet date to the related receiving reports and vendor invoices; any payments made on transactions dated before year-end reflect a liability that should have been recorded. Choice "a" is incorrect. Vouching a sample of recorded accounts payable entries to unmatched receiving reports does not test the completeness of the listing. Unrecorded liabilities would not be included in recorded accounts payable entries. Choice "b" is incorrect. Purchase orders issued after year-end should not be included in the year-end balance of accounts payable. This would be an example of an overstated liability, rather than an unrecorded one. Choice "d" is incorrect. Examination of cash disbursements entries made just prior to the balance sheet date relates to liabilities that have been paid, which would not be considered to be outstanding liabilities at year-end.

Question 600:

If an investor's certainty equivalent is greater than the expected value of an investment alternative, the investor is said to be:

A. Risk indifferent. B. Risk averse. C. Risk seeking. D. Cautious.

C. Risk seeking. Choice "c" is correct. If an investor's certainty equivalent, the point at which they are indifferent to risk, exceeds the expected return on an investment, then the investor is actually seeking lower return for higher risk. This behavior represents risk seeking behavior. Choice "a" is incorrect. Risk indifferent behavior occurs when an investor's certainty equivalent is equal to the expected return on the investment. Choice "b" is incorrect. Risk averse behavior occurs when an investor's certainty equivalent is less than the expected rate of return. The investor seeks higher returns for more risk. Choice "d" is incorrect. Cautious is not a technical term used in risk behavior classifications.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.