AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 571:

Which of the following best describes the auditor's reporting responsibility concerning information accompanying the basic financial statements in an auditor-submitted document?

A. The auditor has no reporting responsibility concerning information accompanying the basic financial statements. B. The auditor should report on the information accompanying the basic financial statements only if the auditor participated in its preparation. C. The auditor should report on the information accompanying the basic financial statements only if the auditor did not participate in its preparation. D. The auditor should report on all the information included in the document.

D. The auditor should report on all the information included in the document. Choice "d" is correct. When an auditor submits a document containing audited financial statements to the client or others, the auditor has a responsibility to report on all the information included in the document. Choice "a" is incorrect. The auditor does have additional reporting responsibilities concerning information that accompanies the basic financial statements in an auditor-submitted document. Choice "b" is incorrect. The auditor has responsibility to report on any additional information regardless of whether the auditor participated in the preparation of the information. Choice "c" is incorrect. The auditor has reporting responsibilities regardless of whether the auditor participated in the preparation of the information.

Question 572:

Which of the following procedures is usually the first step in reviewing the financial statements of a nonissuer?

A. Make preliminary judgments about risk and materiality to determine the scope and nature of the procedures to be performed. B. Obtain a general understanding of the entity's organization, its operating characteristics, and its products or services. C. Assess the risk of material misstatement arising from fraudulent financial reporting and the misappropriation of assets. D. Perform a preliminary assessment of the operating efficiency of the entity's internal control activities.

B. Obtain a general understanding of the entity's organization, its operating characteristics, and its products or services. Choice "b" is correct. In reviewing the financial statements of a nonpublic entity, one of the first steps would be to obtain sufficient knowledge of the entity's business, including its organization, operating characteristics, and products or services. Choice "a" is incorrect. In an audit, preliminary judgments about risk and materiality are used to determine the scope and nature of procedures to be performed. A review is substantially less in scope than an audit and consists principally of inquiries and analytical procedures. Choice "c" is incorrect. In an audit, the risk of material misstatement arising from fraud must be assessed in order to determine the scope and nature of procedures to be performed. A review is substantially less in scope than an audit and consists principally of inquiries and analytical procedures. While inquiries would be made about fraud, a formal fraud risk assessment is not required. Choice "d" is incorrect. In a review of a nonissuer's financial statements, no assessment or testing of internal control is required.

Question 573:

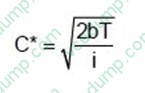

A company uses the following formula in determining its optimal level of cash.

Where: b = Fixed cost per transaction i = Interest rate on marketable securities T = Total demand for cash over a period of time

This formula is a modification of the Economic Order Quantity (EOQ) formula used for inventory management. Assume that the fixed cost of selling marketable securities is $10 per transaction, and the interest rate on marketable securities is 6 percent per year. The company estimates that it will make cash payments of $12,000 over a one-month period. What is the average cash balance (rounded to the nearest dollar)?

A. $1,000 B. $2,000 C. $3,464 D. $6,928

C. $3,464 Choice "c" is correct. Like the EOQ, this formula represents the amount of cash brought in by the sale of marketable securities. Also like the EOQ, this cash goes to zero (or the safety level) over time. The average cash (like the average inventory) is one half of the amount collected. Remember also to convert the interest rate to a per month figure of 0.5% Choices "a", "b", and "d" are incorrect, per above.

Question 574:

The apparent authority of a partner to bind the partnership in dealing with third parties: A. Will be effectively limited by a formal resolution of the partners of which third parties are aware.

B. Will be effectively limited by a formal resolution of the partners of which third parties are unaware.

C. Would permit a partner to submit a claim against the partnership to arbitration.

D. Must be derived from the express powers and purposes contained in the partnership agreement.

Correct Answer. A

A Choice "a" is correct. This is really an agency question on apparent authority. Apparent authority is authority that a third party reasonably believes an agent has. If the third party is aware of a restriction on the agent's authority, the third party cannot reasonably believe that the agent has the restricted authority. Choice "b" is incorrect. A formal resolution of the partners will not be effective to destroy authority if a third party is aware of the resolution, but not if the third party is unaware of the resolution. Choice "c" is incorrect. Submitting a claim to arbitration is an extraordinary act. A partner has apparent authority only to enter into transactions apparently carrying on in the usual way the business of the partnership. There is no apparent authority to enter into an extraordinary transaction. Choice "d" is incorrect. Apparent authority is derived from what a reasonable person believes concerning the authority of a partner based on the partnership's actions toward the third party; authority derived from the express powers and purposes contained in the partnership agreement is actual authority.

Question 575:

Park and Graham entered into a written partnership agreement to operate a retail store. Their agreement was silent as to the duration of the partnership. Park wishes to dissociate from the partnership. Which of the following statements is correct?

A. Park may dissociate from the partnership at any time. B. Unless Graham consents to the dissociation, Park must apply to a court and obtain a decree ordering the dissociation. C. Park may not dissociate from the partnership unless Graham consents. D. Park may dissociate from the partnership only after notice of the proposed dissolution is given to all partnership creditors.

A. Park may dissociate from the partnership at any time. Choice "a" is correct. Because the agreement is silent as to duration, it is a partnership at will. A partner may dissociate from a partnership at will at any time. Choice "b" is incorrect. Because the agreement is silent as to duration, it is a partnership at will. A partner may dissociate from a partnership at will at any time. No court order is required. Choice "c" is incorrect. Partnerships are consensual relationships, so any partner has the power to dissociate at any time; he or she need not obtain the consent of the other partners (though absent consent, the partner will be liable for damages if the dissociation is wrongful). Choice "d" is incorrect. There is no requirement of giving partnership creditors a formal notice of intent to dissociate, but it is a good idea to do so to avoid liability on future partnership obligations.

Question 576:

The purpose of segregating the duties of hiring personnel and distributing payroll checks is to separate the:

A. Human resources function from the controllership function. B. Administrative controls from the internal accounting controls. C. Authorization of transactions from the custody of related assets. D. Operational responsibility from the recordkeeping responsibility.

C. Authorization of transactions from the custody of related assets. Choice "c" is correct. The purpose of segregating the duties of hiring personnel (personnel department/human resources) and distributing payroll checks (treasurer's department) is to separate the authorization of transactions (hiring, pay rates, et. are authorized by the personnel department/human resources) from the custody of related assets (cash or checks are held in the treasurer's department). Choice "a" is incorrect. Segregation of hiring personnel (human resources/ personnel) from distribution of payroll checks (treasurer's department) does not involve the controllership function. Choice "b" is incorrect. Keeping administrative controls (management's directives) and accounting controls separate is not accomplished by segregating the hiring and distribution functions. Choice "d" is incorrect. Neither operational responsibility nor recordkeeping responsibility includes distributing checks or hiring personnel.

Question 577:

Which of the following would not be considered an analytical procedure?

A. Estimating payroll expense by multiplying the number of employees by the average hourly wage rate and the total hours worked. B. Projecting an error rate by comparing the results of a statistical sample with the actual population characteristics. C. Computing accounts receivable turnover by dividing credit sales by the average net receivables. D. Developing the expected current-year sales based on the sales trend of the prior five years.

B. Projecting an error rate by comparing the results of a statistical sample with the actual population characteristics. Choice "b" is correct. Analytical procedures involve comparison of recorded amounts, or ratios developed from recorded amounts, to expectations developed by the auditor. Projecting an error rate from a statistical sample does not involve such a comparison. Choice "a" is incorrect. An analytical procedure involves comparison of an independently developed expectation to a recorded amount. Comparing an estimate of payroll expense (developed by multiplying the number of employees by the average hourly rate and the total hours worked) to the recorded expense is an analytical procedure. Choice "c" is incorrect. An analytical procedure involves comparison of an independently developed expectation to a recorded amount. Ratio analysis is often performed in order to compare recorded results to industry norms or to past performance, and therefore calculation of accounts receivable turnover is likely to be an analytical procedure. Choice "d" is incorrect. An analytical procedure involves comparison of an independently developed expectation to a recorded amount. Comparing an estimate of sales (developed based on a trend analysis) to the recorded amount is an analytical procedure.

Question 578:

Eller, Fort, and Owens do business as Venture Associates, a general partnership. ABC Corp. brought a breach of contract suit against Venture and Eller individually. ABC won the suit and filed a judgment against both Venture and Eller. ABC will generally be able to collect the judgment from:

A. Partnership assets only. B. The personal assets of Eller, Fort, and Owens only. C. Eller's personal assets only after partnership assets are exhausted. D. Eller's personal assets only.

C. Eller's personal assets only after partnership assets are exhausted. Choice "c" is correct. When a judgment is obtained against both a partnership and an individual general partner, the plaintiff must proceed against the partnership assets first and then the assets of any individual general partner. The partnership assets must be exhausted before any general partner's individual assets can be attached. Choices "a", "b", and "d" are incorrect, per the above rule.

Question 579:

Which of the following is required documentation in an audit in accordance with generally accepted auditing standards?

A. A flowchart or narrative of the information system relevant to financial reporting describing the recording and classification of transactions for financial reporting. B. An audit plan setting forth in detail the procedures necessary to accomplish the engagement's objectives. C. A planning memorandum establishing the timing of the audit procedures and coordinating the assistance of entity personnel. D. An internal control questionnaire identifying controls that assure specific objectives will be achieved.

B. An audit plan setting forth in detail the procedures necessary to accomplish the engagement's objectives. Choice "b" is correct. In an audit conducted in accordance with GAAS, the auditor must document the audit plan, setting forth in detail the procedures necessary to accomplish the engagement's objectives. Choice "a" is incorrect. Documentation of the auditor's understanding of the client's internal control is required, but may take different forms. A narrative, an internal control questionnaire, a flowchart, or simply a memorandum (for a small client) may be sufficient. Choice "c" is incorrect. A planning memo, while recommended, is not required under GAAS. Choice "d" is incorrect. Documentation of the auditor's understanding of the client's internal control is required, but may take different forms: narrative, internal control questionnaire, flowchart, or simply a memorandum (for a small client) may be sufficient. In addition, controls do not assure the achievement of objectives.

Question 580:

An example of an indirect cash flow effect would be:

A. Cash committed at inception of the project. B. Increased payroll expenses due to the project. C. A depreciation tax shield. D. An increase in expected future operating cash flows.

C. A depreciation tax shield. Choice "c" is correct. A depreciation tax shield is one of the most common indirect cash flow effects. Choices "a", "b", and "d" are incorrect, as these are all directly related to the capital investment and have an immediate effect on the amount of cash available to the company. Thus, they are all direct cash flow effects.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.