AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 21:

The term underwriting spread refers to the:

A. Commission percentage an investment banker receives for underwriting a security lease. B. Discount investment bankers receive on securities they purchase from the issuing company. C. Difference between the price the investment banker pays for a new security issue and the price at which the securities are resold. D. Commission a broker receives for either buying or selling a security on behalf of an investor.

C. Difference between the price the investment banker pays for a new security issue and the price at which the securities are resold. Choice "c" is correct. Investment bankers are paid their fees partly by being allowed to purchase the new securities they are underwriting for a discount and then reselling those securities on the market. This is known as the underwriting spread. Choices "a" and "d" are incorrect, as both of these describe either fees or commissions and not an underwriting spread. Choice "b" is incorrect. The underwriting spread is the difference between the discount price paid and the resale price.

Question 22:

Which of the following inventory management approaches orders at the point where carrying costs equate nearest to restocking costs in order to minimize total inventory cost?

A. Economic order quantity. B. Just-in-time. C. Materials requirements planning. D. ABC.

A. Economic order quantity. Explanation Choice "a" is correct. The economic order quantity (EOQ) method of inventory control anticipates orders at the point where carrying costs are nearest to restocking costs. The objective of EOQ is to minimize total inventory costs. The formula for EOQ is: Choice "b" is incorrect. Just in time (JIT) inventory models were developed to reduce the lag time between inventory arrival and inventory use. Choice "c" is incorrect. Materials requirements planning (MRP) is a method of determining inventory requirements when a given number of units is needed. The method is used to create precise schedules of which items will be needed and what times they will be needed. Choice "d" is incorrect. ABC is an acronym for Activity Based Costing, a method of cost assignment that identifies value added activities and related cost drivers. It is not an inventory management approach.

Question 23:

An auditor issued an audit report that was dual dated for a subsequent event occurring after the original date of the auditor's report but before issuance of the related financial statements. The auditor's responsibility for events occurring subsequent to the original report date was:

A. Limited to include only events occurring up to the date of the last subsequent event referenced. B. Limited to the specific event referenced. C. Extended to subsequent events occurring through the later date. D. Extended to include all events occurring since the original report date.

B. Limited to the specific event referenced. Choice "b" is correct. When an auditor issues a report that is dual dated for a subsequent event occurring after the original date of the auditor's report, but before issuance of the related financial statements, the auditor's responsibility for events occurring subsequent to the original report date is limited to the specific event referenced. Choices "a", "c", and "d" are incorrect. The auditor takes responsibility for only the specific event noted in the dual dating and no other event occurring subsequent to the original report date.

Question 24:

Product demands become more elastic the:

A. Greater the number of substitute products available. B. Greater the consumer income. C. Greater the elasticity of supply. D. Shorter the time period considered.

A. Greater the number of substitute products available. Choice "a" is correct. Product demands become more elastic the greater the number of substitutes available. With price increases, consumers will switch to substitute goods. Choice "b" is incorrect. Consumer income will not affect demand elasticity. Choice "c" is incorrect. Elasticity of supply and demand is unrelated. Choice "d" is incorrect. Product demand is more elastic the longer the time period, since more choices become available.

Question 25:

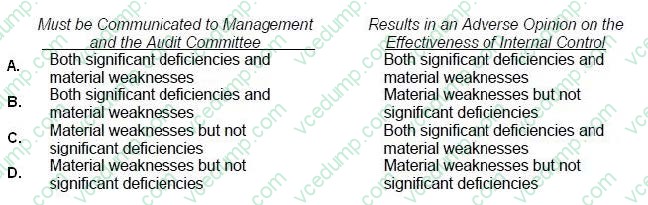

Which of the following best describes the responsibility of the auditor with respect to significant deficiencies and material weaknesses in an audit of an issuer?

A. Option A B. Option B C. Option C D. Option D

B. Option B Choice "b" is correct. In an audit of an issuer, the auditor is required to communicate both significant deficiencies and material weaknesses to management and the audit committee, but only material weaknesses result in an adverse opinion on the effectiveness of internal control. Choice "a" is incorrect. In an audit of an issuer, significant deficiencies (that do not rise to the level of being material weaknesses) do not result in an adverse opinion on the effectiveness of internal control. Choice "c" is incorrect. In an audit of an issuer, both significant deficiencies and material weaknesses must be communicated, in writing, to management and the audit committee. In addition, significant deficiencies (that do not rise to the level of being material weaknesses) do not result in an adverse opinion on the effectiveness of internal control. Choice "d" is incorrect. In an audit of an issuer, the auditor is required to communicate both significant deficiencies and material weaknesses to management and the audit committee.

Question 26:

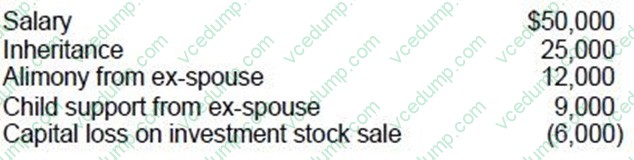

In the current year Jensen had the following items:

What is Jensen's AGI for the current year?

A. $44,000 B. $59,000 C. $62,000 D. $84,000

B. $59,000 Explanation Explanation/Reference:Choice "b" is correct. The question asks for AGI, but all of the items in the list are items of potential gross income. There are no adjustments included in the list; therefore, in this case, AGI is the same as gross income. The calculation is as follows: Choices "a", "c", and "d" are incorrect, per the above calculation.

Question 27:

Which of the following actions is the acknowledged preventive measure for a period of deflation?

A. Increasing interest rates. B. Increasing the money supply. C. Decreasing interest rates. D. Decreasing the money supply.

B. Increasing the money supply. Choice "b" is correct. Deflation is a general decline in the overall price level (i.e., when the inflation rate is negative). Increasing the money supply causes the overall price level to rise. As a result, it helps eliminate deflation. Choice "a" is incorrect. Increasing interest rates causes aggregate demand to shift left. As a result, the aggregate price level will fall even further. This will exasperate deflation. Choice "c" is not wrong but it is not as good an answer as "b". A decrease in interest rates causes the aggregate demand curve to shift right. As a result, the aggregate price level will rise. This helps eliminate deflation. However, there are times when interest rates are already so low that lowering interest rates is not an option. Thus, the preferred or "acknowledged" preventative measure for deflation is increasing the money supply. Choice "d" is incorrect. Decreasing the money supply causes the overall price level to fall. This would obviously exasperate deflation.

Question 28:

A company plans to tighten its credit policy. The new policy will decrease the average number of days in collection from 75 to 50 days and will reduce the ratio of credit sales to total revenue from 70 to 60 percent. The company estimates that projected sales would be five percent less if the proposed new credit policy is implemented. If projected sales for the coming year are $50 million, calculate the dollar impact on accounts receivable of this proposed change in credit policy. Assume a 360-day year.

A. $3,817,445 decrease. B. $6,500,000 decrease. C. $3,333,334 decrease. D. $18,749,778 increase.

C. $3,333,334 decrease. Explanation Explanation/Reference: Choice "c" is correct. $3,333,334 decrease in accounts receivable.

Question 29:

Property acquisitions that are misclassified as maintenance expense would most likely be detected by an internal accounting control system that provides for:

A. Investigation of variances within a formal budgeting system. B. Review and approval of the monthly depreciation entry by the plant supervisor. C. Segregation of duties of employees in the accounts payable department. D. Examination by the internal auditor of vendor invoices and canceled checks for property acquisitions.

A. Investigation of variances within a formal budgeting system. Choice "a" is correct. Investigation of variances in a formal budget might show maintenance costs over budget or acquisition costs under budget, either of which would trigger an investigation. Choice "b" is incorrect. Review of journal entries relating to depreciation would not disclose acquisitions misclassified as maintenance expense, since no depreciation would be recorded for the misclassified items. Choice "c" is incorrect. Segregation of duties in the accounts payable department would have no effect on the account classification of an approved invoice. Choice "d" is incorrect. Since the internal auditor would be looking at invoices and checks related to recorded property acquisitions, he or she would not be likely to identify payments that were erroneously excluded from the property account.

Question 30:

Compared to firms in a perfectly competitive market, a monopolist tends to:

A. Produce substantially less but charge a higher price. B. Produce substantially more and charge a higher price. C. Produce the same output and charge a higher price. D. Produce substantially less and charge a lower price.

A. Produce substantially less but charge a higher price. Choice "a" is correct. Compared to firms in a perfectly competitive market, a monopolist tends to produce substantially less but charge a higher price. Choices "b", "c", and "d" are incorrect, per above Explanation.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.