CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

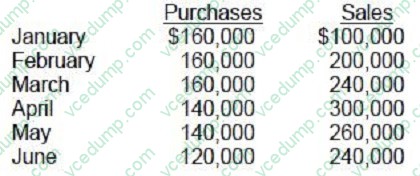

Question 1211:

The following information applies to ABC Company.

Forty percent of purchases are paid for in cash at the time of purchase, and 30 percent is paid for in each of the next two months. Purchases for the previous November and December were $150,000 per month. Payroll is 10 percent of sales in the month it occurs, and operating expenses are 20 percent of the following months sales (July sales were $220,000). Interest payments were $20,000 paid quarterly in January and April. ABC's cash disbursements for the month of April were:

A. $152,000

B. $200,000

C. $248,000

D. $254,000 -

Question 1212:

Analytical procedures performed in the overall review stage of an audit suggest that several accounts have unexpected relationships. The results of these procedures most likely would indicate that:

A. Irregularities exist among the relevant account balances.

B. Internal control activities are not operating effectively.

C. Additional tests of details are required.

D. The communication with those charged with governance should be revised. -

Question 1213:

When an auditor tests the internal controls of a computerized accounting system, which of the following is true of the test data approach?

A. Test data are coded to a dummy subsidiary so they can be extracted from the system under actual operating conditions.

B. Test data programs need not be tailor-made by the auditor for each client's computer applications.

C. Test data programs usually consist of all possible valid and invalid conditions regarding compliance with internal controls.

D. Test data are processed with the client's computer and the results are compared with the auditor's predetermined results. -

Question 1214:

When a company offers credit terms of 2/10, net 30, the annual interest cost, based on a 360-day year, is:

A. 24.0 percent.

B. 35.3 percent.

C. 36.0 percent.

D. 36.7 percent. -

Question 1215:

ABC Co. reported a retained earnings balance of $400,000 at December 31, 1991. In August 1992, ABC determined that insurance premiums of $60,000 for the three-year period beginning January 1, 1991, had been paid and fully expensed in 1991. ABC has a 30% income tax rate. What amount should ABC report as adjusted beginning retained earnings in its 1992 statement of retained earnings?

A. $420,000

B. $428,000

C. $440,000

D. $442,000 -

Question 1216:

Which of the following partners of a limited liability partnership (LLP) may avoid personal liability when a partner commits a negligent act?

A. All the partners.

B. The supervisor of the negligent partner.

C. All the partners other than the negligent partner.

D. All the partners other than the supervisor of, and, the negligent partner. -

Question 1217:

It is not appropriate to refer a reader of an auditor's report to a financial statement footnote for details concerning:

A. Subsequent events.

B. The pro forma effects of a business combination.

C. Sale of a discontinued operation.

D. The results of confirmation of receivables. -

Question 1218:

ABC Corp. reports operating expenses in two categories: (1) selling and (2) general and administrative. The adjusted trial balance at December 31, 1989 included the following expense and loss accounts:

One-half of the rented premises is occupied by the sales department. ABC's total selling expenses for 1989 are:

A. $480,000

B. $400,000

C. $370,000

D. $360,000 -

Question 1219:

Income tax-basis financial statements differ from those prepared under GAAP in that income tax-basis financial statements:

A. Do not include nontaxable revenues and nondeductible expenses in determining income.

B. Include detailed information about current and deferred income tax liabilities.

C. Contain no disclosures about capital and operating lease transactions.

D. Recognize certain revenues and expenses in different reporting periods. -

Question 1220:

Which of the following statements regarding competitive advantage is not true?

A. The two major forms of competitive advantage are product differentiation and cost leadership.

B. If the manufacturing costs of a firm are less than those of close rivals, then the firm has a competitive market advantage.

C. Cost leadership advantage may be the best be obtained by a firm when a firm builds market share or matches the price of its rivals.

D. Differentiation advantage may best be obtained by a firm when a firm builds market share or increases its price.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.