Exam Details

Exam Code

:CIMAPRA19-F02-1Exam Name

:F2 - Advanced Financial ReportingCertification

:CIMA CertificationsVendor

:CIMATotal Questions

:256 Q&AsLast Updated

:Jul 17, 2025

CIMA CIMA Certifications CIMAPRA19-F02-1 Questions & Answers

-

Question 121:

The basic earning per share computed by a company for year ended 31st March 20X7 is £2 per share. The company had certain convertible debentures outstanding as on 31st March 20X7. The conversion of debentures to equity shares would result in the earnings per share to be ?.2. Which of the following should the company disclose?

A. Basic earnings per share only

B. Diluted earnings per share only

C. Both basic and diluted earnings per share

D. Neither basic nor diluted earnings per share

-

Question 122:

LM is a car dealer that is supplied inventory by car manufacturer SQ. Trading between LM and SQ is subject to a contractual agreement. This agreement states the following:

1.

Legal title of the cars remains with SQ until they are sold by LM to a third party.

2.

Upon notification of sale to a third party by LM, SQ raises an invoice at the price agreed at the original date of delivery to LM.

3.

LM has the right to return any car at any time without incurring a penalty.

4.

LM is responsible for insuring all of the cars on its property.

When considering how these cars should be accounted for, which THREE of the following statements are true?

A. The most significant risks attached to the cars are held by LM.

B. The most significant risks attached to the cars are held by SQ.

C. SQ should recognise the cars as inventory in their financial statements.

D. LM should recognise the cars as inventory in their financial statements.

E. SQ should recognise revenue when the cars are delivered to LM.

F. When LM sells a car to a third party, SQ should recognise the revenue associated with that sale.

-

Question 123:

Which TWO of the following are true in relation to IAS21 The Effects of Changes in Foreign Exchange Rates when consolidating an overseas subsidiary?

A. A current period exchange gain or loss is shown within the consolidated statement of comprehensive income within other comprehensive income.

B. Goodwill is re-translated at the end of each reporting period and reflected at the period end exchange rate in the consolidated statement of financial position.

C. Assets and liabilities of the subsidiary are translated at each reporting date using the average exchange rate for the period.

D. Goodwill is reflected in the consolidated statement of financial position translated at the exchange rate on the date of acquisition.

E. The statement of profit or loss of the subsidiary is translated for the reporting period using the closing exchange rate.

-

Question 124:

JKL measure gearing as debt:equity, based on book values. At 31 December 20X5 the ratio is 2:3 and JKL would like this to be 2:5. Which of the following transactions individually would achieve this?

A. Bonus issue from the share premium account.

B. Revaluation of investment property to an increased fair value.

C. Repayment of a 6 year term loan with the issue of 5 year redeemable debentures.

D. Issue of redeemable preference shares at par.

-

Question 125:

AB owned 80% of the equity share capital of FG at 1 January 20X6. AB disposed of 10% of FG's equity share capital on 31 December 20X6 for $400,000. The non controlling interest was measured at $700,000 immediately prior to the disposal.

Which of the following represents the adjustment that AB made to non controlling interest in respect of the disposal when it prepared its consolidated financial statements at 31 December 20X6?

A. Credit of $350,000

B. Debit of $400,000

C. Debit of $350,000

D. Credit of $50,000

-

Question 126:

A local council is one year into a two year project to renovate local parks. The project is on track to be completed within the set time-scale, however it has proved more costly than initially expected.

The project is on track to be completed within its two year period. Contracts for the labour and materials needed to renovate the parks were agreed at the start of the project and no changes have arisen. Despite the fact that the council has

yet to fully settle these contracts, costs are set to be as budgeted.

Why would this example not be recognised as a provision?

A. Neither the timing nor the amount of the provision is uncertain.

B. The settlement of the contract is unlikely to result in an outflow from the council.

C. The council doesn't have a present obligation from the project.

D. The council has no potential future obligations arising from the project.

-

Question 127:

Which of the following is a related party according to the definition of a related party in IAS24 Related Party Disclosures?

A. Major customer

B. Provider of finance

C. Managing Director

D. Major supplier

-

Question 128:

Entity A entered into a 3 year operating lease on 1 April 20X3. The rentals are £5,000 a year payable in advance with an additional payment of $1,800 payable on 1 April 20X3. The rental expense to be included in the statement of profit or loss for the year ended 31 December 20X3 will be:

A. $4,200

B. $5,000

C. $6,800

D. $5,600

-

Question 129:

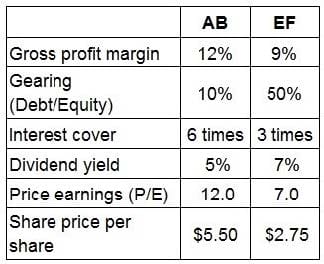

AB and EF are located in the same country and prepare their financial statements to 31 October in accordance with International Accounting Standards. EF supplies AB with a component that is vital to AB's product range. AB is considering acquiring a controlling interest in EF by 31 December 20X4 in order to guarantee future supply. The Board of EF has indicated that such an approach would be postively considered. AB would use its control to make AB the sole customer of EF.

The Finance Director of AB has been granted access to EF's management accounts and has conducted some initial analysis from the financial press. The results togther with comparisons for AB for the year to 31 October 20X4 are presented below:

AB and EF are forecasting revenues of S1,500,000 and $700,000 respectively for the year ended 31 October 20X5.

AB's Finance Director met with one of the directors of EF to discuss the potential impact of the acquisition.

Which of the director's statements below is correct?

A. The P/E ratio of EF will increase to 12 after acquisition in line with that of AB.

B. The gross profit margin of EF will increase if AB's bargaining power is used to negotiate lower material costs for the whole group.

C. Redundancy costs arising from reorganisation following acquisition will be provided for by charging EF's profit for the year ended 31 October 20X4.

D. Dividend yield for both entities will be identical after the acquisition.

-

Question 130:

Which of the following best describes the goal of WACC as a measure?

A. To work out the average return that is required by the company on its investments in order to satisfy all shareholders and debt holders.

B. To work out the average return that is required by the company on its investments in order to satisfy all shareholders.

C. To work out the average return that is required by the company on its investments in order to satisfy all debt holders.

D. To work out the minimum return that is required by the company on its investments in order to satisfy all shareholders and debt holders.

Related Exams:

CIMA-BA1

BA1 - Fundamentals of Business EconomicsCIMA-BA2

BA2 - Fundamentals of Management AccountingCIMA-BA3

BA3 - Fundamentals of Financial AccountingCIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business LawCIMA-CS3

CS3 - Strategic Case Study 2021CIMA-E1

E1 - Managing Finance in a Digital WorldCIMA-E2

E2 - Managing PerformanceCIMA-E3

E3 - Strategic ManagementCIMA-F1

F1 - Financial ReportingCIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMAPRA19-F02-1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.