CIMA-P1 Exam Details

-

Exam Code

:CIMA-P1 -

Exam Name

:P1 - Management Accounting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:275 Q&As -

Last Updated

:Jul 15, 2026

CIMA CIMA-P1 Online Questions & Answers

-

Question 61:

A completed unit of Product A requires 9 kg of material and 10% of material is wasted in the production process.

Material has a standard cost of $5 per kg.

Product A also requires 4 labour hours at a standard cost of $10 per labour hour and variable overheads at a standard cost of $2 per labour hour

What is the standard variable production cost per unit of Product A?

A. $97.50

B. $93

C. $98

D. $50 -

Question 62:

Some of the movements in a time series follow a pattern over time. Which type of movement does NOT follow a pattern over time?

A. Trend

B. Cyclical variation

C. Random variation

D. Seasonal variation -

Question 63:

A manager has not yet used all oh his budget. He is worried that his budget maybe reduced next year if he is not seen to have needed all the funds. He decides to spend the remaining £1,580 on another team building exercise as well as a catered lunch for his department.

This example falls under which behavioural aspect of budgetary control?

A. Irrational spending

B. Motivation

C. Budget negotiation

D. Short term focus -

Question 64:

RFT, an engineering company, has been asked to provide a quotation for a contract to build a new engine. The potential customer is not a current customer of RFT, but the directors of RFT are keen to try and win the contract as they believe that this may lead to more contracts in the future. As a result, they intend pricing the contract using relevant costs. The following information has been obtained from a two-hour meeting that the Production Director of RFT had with the potential customer. The Production Director is paid an annual salary equivalent to $1,200 per 8-hour day. 110 square meters of material A will be required. This is a material that is regularly used by RFT and there are 200 square meters currently in inventory. These were bought at a cost of $12 per square meter. They have a resale value of $10.50 per square meter and their current replacement cost is $12.50 per square meter. 30 liters of material B will be required. This material will have to be purchased for the contract because it is not otherwise used by RFT. The minimum order quantity from the supplier is 40 liters at a cost of $9 per liter. RFT does not expect to have any use for any of this material that remains after this contract is completed. 60 components will be required. These will be purchased from HY. The purchase price is $50 per component. A total of 235 direct labour hours will be required. The current wage rate for the appropriate grade of direct labour is $11 per hour. Currently RFT has 75 direct labour hours of spare capacity at this grade that is being paid under a guaranteed wage agreement. The additional hours would need to be obtained by either (i) overtime at a total cost of $14 per hour; or (ii) recruiting temporary staff at a cost of $12 per hour. However, if temporary staff are used they will not be as experienced as RFT's existing workers and will require 10 hours supervision by an existing supervisor who would be paid overtime at a cost of $18 per hour for this work. 25 machine hours will be required. The machine to be used is already leased for a weekly leasing cost of $600. It has a capacity of 40 hours per week. The machine has sufficient available capacity for the contract to be completed. The variable running cost of the machine is $7 per hour. The company absorbs its fixed overhead costs using an absorption rate of $20 per direct labour hour.

Select ALL the true statements.

A. The cost for the production director meeting was a relevant cost.

B. Material A was a relevant cost.

C. Material B was a relevant cost.

D. The components are to be purchased from HY at a cost of $50 each. This is a relevant cost because it is future expenditure that will be incurred as a result of the work being undertaken.

E. The machine is currently being leased and it has spare capacity so it will either stand idle or be used on this work. The lease cost will be a relevant cost or $10 per hour.

F. The company absorbs its fixed overhead costs using an absorption rate of $20 per direct labour hour. This is a relevant cost.

G. The relevant cost is $7010

H. The relevant cost is $7080

I. The relevant cost is $7100 -

Question 65:

Explain the advantages of management participation in budget setting and the potential problems that may arise in the use of the resulting budget as a control mechanism.

Select all the correct answers.

A. A purposes of budgeting is to act as a control mechanism, with actual results being compared against budget.

B. Another purpose of a budget is to set targets to motivate managers and optimize their performance.

C. The participation of managers in the budget setting process has several advantages. Managers are more likely to be motivated to achieve the target if they have participated in setting process has several advantages. managers are more likely to be motivated to achieve the target if they have participated in setting the target.

D. Participation in budget setting can reduce the information asymmetry gap that can arise when targets are imposed by senior management. Imposed targets are likely to make managers feel demotivated and alienated and result in poor performance.

E. Participation in budget setting can cause problems; in particular, managers may attempt to negotiate budgets that they feel are easy to achieve which gives rise to "budget padding" or budgetary slack.

F. Managers will not `empire build' because they don't believe that the size of their budget reflects their importance within the organization. -

Question 66:

A company is preparing its annual budget and is estimating the number of units of Product A that it will sell in each quarter of year 2. Past experience has shown that the trend for sales of the product is represented by the following relationship: y = a + bx where y = number of sales units in the quarter a = 10,000 units b = 3,000 units x = the quarter number where 1 = quarter 1 of year 1 Actual sales of Product A in Year 1 were affected by seasonal variations and were as follows: Quarter 1:14,000 units Quarter2: 18,000 units Quarter 3: 18,000 units Quarter 4: 20,000 units Calculate the expected sales of Product A (in units) for each quarter of year 2, after adjusting for seasonal variations using the additive model.

A. The expected sales for year 2 Quarter 4 was 32700 units

B. The expected sales for year 2 Quarter 4 was 32000 units

C. The expected sales for year 2 Quarter 4 was 33000 units

D. The expected sales for year 2 Quarter 4 was 40000 units -

Question 67:

A company operates a customer complaints department.

How will the cost of the customer complaints department be classified in a system focussed on quality related costs?

A. External failure cost

B. Internal failure cost

C. Prevention cost

D. Appraisal cost -

Question 68:

CORRECT TEXT

A company has identified the trend in its sales figures through the regression equation Y = 65.9 + 3.86X, where Y is the sales revenue in thousands of dollars and X is the month number. The average seasonal variation for October is 87%

Calculate the forecast sales revenue for October of Year 6. Give your answer to the nearest $000.

-

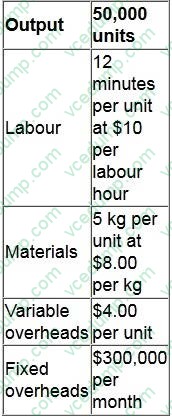

Question 69:

CORRECT TEXT

A company's budgeted data for the period are shown in the table below.

There is a stepped increase in fixed overheads of $10,000 when production exceeds 52,000 units.

Actual production for the period was 60,000 units.

What is the flexed budgeted cost for the period?

Give your answer as a whole number (in '000s).

-

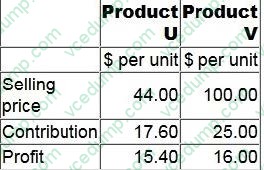

Question 70:

Information about a company's only two products is as follows:

The revenue from the products must be in the constant mix of 2U:3V. Budgeted monthly sales revenue is $110,000.

Fixed costs are $23,095 each month.

To the nearest $10, what is the budgeted monthly margin of safety in terms of sales revenue?

A. $35,500

B. $74,500

C. $12,140

D. $38,940

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-P1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.