CIMA-P1 Exam Details

-

Exam Code

:CIMA-P1 -

Exam Name

:P1 - Management Accounting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:275 Q&As -

Last Updated

:Jul 15, 2026

CIMA CIMA-P1 Online Questions & Answers

-

Question 51:

Company NBO is providing a quote to manufacture 500 passenger seats for a bus company.

Relevant cost is being used as the basis for the quote.

Which THREE of the following should be included as relevant costs or savings in the production of the 500 passenger seats?

A. Equipment depreciation of $2,000 for the time the passenger seats are in production.

B. Electricity charges of $1,500 for the completion of the order.

C. Administration overheads of $3,200 apportioned on the basis of labour hours in production.

D. Seat cover material, to be bought for $6,000, which cannot be used on other products.

E. Idle time pay of $1,000 which would be paid to workers if the quote is not accepted

F. $750 paid for a consultant's advice on quoting for the order. -

Question 52:

`A zero-based budgeting system involves establishing decision packages that are then ranked in order of their relative importance in meeting the organization's objectives'.

Which of the following is true regarding he difficulties that a not-for-profit organization may experience when trying to rank decision packages.

Select ALL true statements.

A. The activities that are being proposed in a budget are described in variable packages. There will often be more less than one decision package proposed for an activity.

B. The activities that are being proposed in a budget are described in decision packages. There will often be more than one decision package proposed for an activity.

C. Some of these packages will be inclusive and will require operations to select the best solution to the issue involved.

D. Some of these packages will be mutually inclusive and will require management to select the best solution to the issue involved.

E. Each decision package is evaluated. Its costs are compared to its benefits and net present values or other measures calculated.

F. Management may decide to reject packages even though the activity was done last year. In this way the organization is said to be starting from a zero base with each package given due consideration.

G. Management may decide to accept packages even though the activity was done last year. In this way the organization is said to be starting from a 100% cost base with each package given due consideration.

H. In a public sector body, for example, decision packages will relate profit making activities.

I. In a public sector body, for example, decision packages will relate to very disparate activities. -

Question 53:

In a make or buy decision, the company has unused machine time. What is the opportunity cost of using the machine for in-house production?

A. Zero

B. Historical cost of machine

C. Market resale value of the machine

D. Fixed overhead absorption rate -

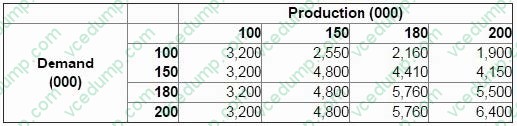

Question 54:

A company is launching a new product.

The company accountant has constructed a payoff table to show the estimated profit at different levels of production and demand.

How many units should the company produce if the minimax regret criterion is applied?

A. 100,000

B. 150,000

C. 180,000

D. 200,000 -

Question 55:

RT produces two products from different quantities of the same resources using a just-in- time (JIT) production system. The selling price and resource requirements of each of the products are shown below:

Market research shows that the maximum demand for products R and T during June 2010 is 500 units and 800 units respectively. This does not include an order that RT has agreed with a commercial customer for the supply of 250 units of R and 350 units of T at selling prices of $100 and $135 per unit respectively. Although the customer will accept part of the order, failure by RT to deliver the order in full by the end of June will cause RT to incur a $10,000 financial penalty. At a recent meeting of the purchasing and production managers to discuss the production plans of RT for June, the following resource restrictions for June were identified: Direct labour hours 7,500 hours

Material A 8,500 kgs

Material B 3,000 litres

Machine hours 7,500 hours

(Refer to previous 2 questions.)

You have now presented your optimum production plan to the purchasing and production managers of RT. During your presentation it became clear that the predicted resource restrictions were rather optimistic. In fact, the managers agreed

that the availability of all of the resources could be as much as 10% lower than their original predictions.

Assuming that RT completes the order with the commercial customer, and using linear programming, show the optimum production plan for RT for June 2010 on the basis that the availability of all resources is 10% lower than originally

predicted.

A. The optimal plan is to produce 550 units of Product R and 650 units of product T in addition to the contract.

B. The optimal plan is to produce 520 units of Product R and 620 units of product T in addition to the contract.

C. The optimal plan is to produce 510 units of Product R and 720 units of product T in addition to the contract.

D. The optimal plan is to produce 560 units of Product R and 670 units of product T in addition to the contract.

E. The optimal plan is to produce 450 units of Product R and 690 units of product T in addition to the contract.

F. The optimal plan is to produce 500 units of Product R and 550 units of product T in addition to the contract. -

Question 56:

Each finished unit of product G contains 2 litres of ingredient L. Losses during production are 10% of input of ingredient L. Budgeted data for next period are as follows:

The budgeted purchases of ingredient L for next period are:

A. 5,770 litres

B. 6,230 litres

C. 5,710 litres

D. 5,170 litres -

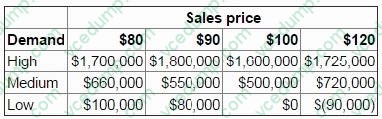

Question 57:

CORRECT TEXT

MBM is considering introducing a new product and has to decide if the sales price should be $80, $90, $100 or $120.

There is a 30% chance that demand could be high, a 50% chance that demand will be at a medium level and a 20% chance that demand will be low.

A payoff table below shows the profits based on the sales price and the level of demand.

MBM has decided, using an expected value approach, that the sales price should be set at $80 as this gives the highest expected profit of $860,000.

A market research company has since approached MBM offering to provide perfect information on the demand level.

What is the maximum amount that should be paid for the perfect information?

Give your answer as a whole number (in '000s).

-

Question 58:

Reported profits using activity-based costing (ABC) may be different from reported profits using marginal costing because ABC:

A. ignores variable costs.

B. includes fixed costs within the cost of inventory.

C. treats materials as the only truly variable cost.

D. leads to a different selling price. -

Question 59:

Which of the following statements regarding marginal and absorption costing are true in the context of pricing decisions? Select ALL that apply.

A. Marginal costing is appropriate for long-term pricing decisions.

B. Marginal costing is appropriate for short-term pricing decisions.

C. Absorption costing when used for pricing decisions includes the 'total-cost' of the product.

D. Marginal costing ensures the recovery of all costs incurred in selling prices.

E. Marginal costing is more appropriate for use in one-off pricing decisions.

F. Absorption costing is more appropriate for use in one-off pricing decisions. -

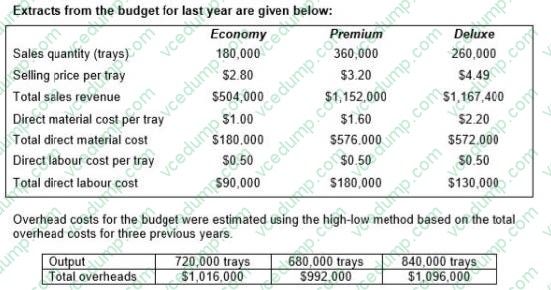

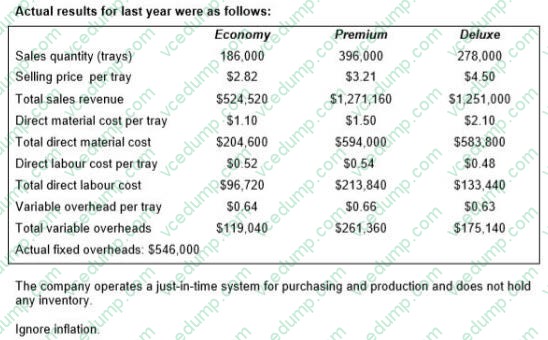

Question 60:

A company produces trays of pre-prepared meals that are sold to restaurants and food retailers. Three varieties of meals are sold: economy, premium and deluxe.

Calculate, for the original budget, the budgeted fixed overhead costs, the budgeted variable overhead cost per tray and the budgeted total overheads costs.

A. Original budget contribution = $162 000, Flexed budget contribution = $ 178 200, Actual Contribution $ 201 960

B. Original budget contribution = $172 000, Flexed budget contribution = $ 148 200, Actual Contribution $ 221 960

C. Original budget contribution = $272 000, Flexed budget contribution = $ 248 200, Actual Contribution $ 321 960

D. Original budget contribution = $242 000, Flexed budget contribution = $ 148 200, Actual Contribution $ 121 960

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-P1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.