8008 Exam Details

-

Exam Code

:8008 -

Exam Name

:PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

Certification

:PRMIA Certifications -

Vendor

:PRMIA -

Total Questions

:362 Q&As -

Last Updated

:Jul 15, 2026

PRMIA 8008 Online Questions & Answers

-

Question 341:

When combining separate bottom up estimates of market, credit and operational risk measures, a most conservative economic capital estimate results from which of the following assumptions:

A. Assuming that the resulting distributions have a correlation between 0 and 1

B. Assuming that market, credit and operational risk estimates are perfectly positively correlated

C. Assuming that market, credit and operational risk estimates are perfectly negatively correlated

D. Assuming that market, credit and operational risk estimates are uncorrelated -

Question 342:

Which of the following are measures of liquidity risk

I - Liquidity Coverage Ratio II - Net Stable Funding Ratio III - Book Value to Share Price IV - Earnings Per Share

A. III and IV

B. I and II

C. II and III

D. I and IV -

Question 343:

A risk analyst peforming PCA wishes to explain 80% of the variance. The first orthogonal factor has a volatility of 100, and the second 40, and the third 30. Assume there are no other factors. Which of the factors will be included in the final analysis?

A. First, Second and Third

B. First and Second

C. First

D. Insufficient information to answer the question -

Question 344:

Which of the following is the most accurate description of EPE (Expected Positive Exposure):

A. The maximum average credit exposure over a period of time

B. The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date

C. Weighted average of the future positive expected exposure across a time horizon.

D. The average of the distribution of positive exposures at a specified future date -

Question 345:

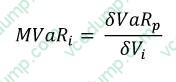

Which of the following best describes the concept of marginal VaR of an asset in a portfolio:

A. Marginal VaR is the value of the expected losses on occasions where the VaR estimate is exceeded.

B. Marginal VaR is the contribution of the asset to portfolio VaR in a way that the sum of such calculations for all the assets in the portfolio adds up to the portfolio VaR.

C. Marginal VaR is the change in the VaR estimate for the portfolio as a result of including the asset in the portfolio.

D. Marginal VaR describes the change in total VaR resulting from a $1 change in the value of the asset in question. -

Question 346:

Consider a portfolio with a large number of uncorrelated assets, each carrying an equal weight in the portfolio. Which of the following statements accurately describes the volatility of the portfolio?

A. The volatility of the portfolio is the same as that of the market

B. The volatility of the portfolio will be close to zero

C. The volatility of the portfolio will be equal to the square root of the sum of the variances of the assets in the portfolio weighted by the square of their weights

D. The volatility of the portfolio will be equal to the weighted average of the volatility of the assets in the portfolio -

Question 347:

Which of the following statements are true ?

I - Risk governance structures distribute rights and responsibilities among stakeholders in the corporation II - Cybernetics is the multidisciplinary study of cyber risk and control systems underlying information systems in an organization III - Corporate governance is a subset of the larger subject of risk governance IV - The Cadbury report was issued in the early 90s and was one of the early frameworks for corporate governance

A. I, II and IV

B. I and IV

C. II and III

D. All of the above -

Question 348:

A long position in a credit sensitive bond can be synthetically replicated using:

A. a long position in a treasury bond and a short position in a CDS

B. a long position in a treasury bond and a long position in a CDS

C. a short position in a treasury bond and a short position in a CDS

D. a short position in a treasury bond and a long position in a CDS -

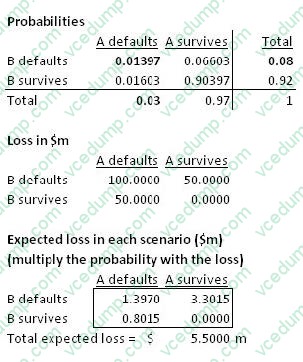

Question 349:

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds are 0.03 and 0.08 respectively, over a one year horizon. If the default correlation is 25%, what is the one year expected loss on this portfolio?

A. $1.38m

B. $11m

C. $5.26m

D. $5.5mc -

Question 350:

A portfolio's 1-day VaR at the 99% confidence level is $250m. What is the annual volatility of the portfolio? (assuming 250 days in the year)

A. $2,410.3m

B. $1,699.4m

C. $107.5m

D. $3,952.8m

Related Exams:

-

8002

PRM Certification - Exam II: Mathematical Foundations of Risk Measurement -

8004

PRM Certification - Exam IV: Case Studies; Standards: Governance, Best Practices and Ethics -

8006

Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition -

8007

Exam II: Mathematical Foundations of Risk Measurement - 2015 Edition -

8008

PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

8009

Exam IV: Case Studies: Standards: Governance, Best Practices and Ethics - 2015 Edition -

8010

Operational Risk Manager (ORM) -

8011

Credit and Counterparty Manager (CCRM) Certificate

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only PRMIA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your 8008 exam preparations and PRMIA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.