8008 Exam Details

-

Exam Code

:8008 -

Exam Name

:PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

Certification

:PRMIA Certifications -

Vendor

:PRMIA -

Total Questions

:362 Q&As -

Last Updated

:Jul 15, 2026

PRMIA 8008 Online Questions & Answers

-

Question 151:

Which of the following correctly describes a reverse stress test:

A. Stress tests that start from a known stress test outcome and then ask what events could lead to such an outcome for the bank

B. A stress test that considers only qualitative factors that go beyond mathematical modeling to examine feedback loops and the effect of macro-economic fundamentals

C. Stress tests that are prescribed and conducted by a regulator in addition to the tests done by a bank

D. A stress test that requires a role reversal between risk managers and the risk taking business units in order to determine credible scenarios -

Question 152:

Which of the following statements are true?

I - Retail Risk Based Pricing involves using borrower specific data to arrive at both credit adjudication and pricing decisions II - An integrated 'Risk Information Management Environment' includes two elements - people and processes III - A Logical Data Model (LDM) lays down the relationships between data elements that an organization stores IV - Reference Data and Metadata refer to the same thing

A. II and IV

B. I and III

C. I, II and III

D. All of the above -

Question 153:

Which of the following statements are true:

I - It is usual to set a very high confidence level when estimating VaR for capital requirements.

II - For model validation, very high VaR confidence levels are used to minimize excess losses.

III - For limit setting for managing day to day positions, it is usual to set VaR confidence levels that are neither too low to be exceeded too often, nor too high as to be never exceeded.

IV - The Basel accord requirements for market risk capital require the use of a time horizon of 1 year.

A. I and IV

B. I and III

C. III and IV

D. II and III -

Question 154:

A zero coupon corporate bond maturing in an year has a probability of default of 5% and yields 12%. The recovery rate is zero. What is the risk free rate?

A. 5.26%

B. 7.00%

C. 5.00%

D. 6.40% -

Question 155:

Which of the following is not a tool available to financial institutions for managing credit risk:

A. Collateral

B. Cumulative accuracy plot

C. Third party guarantees

D. Credit derivatives -

Question 156:

Which of the following risks were not covered in detail in most stress tests prior to the current crisis:

I - The behavior of complex structured products under stressed liquidity conditions II - Pipeline or securitization risk III - Basis risk in relation to hedging strategies IV - Counterparty credit risk V - Contingent risks VI - Funding liquidity risk

A. I, IV and VI

B. I, II, III, IV and VIrisk

C. II, III and V

D. All of the above -

Question 157:

Which of the following represent the parameters that define a VaR estimate?

A. trading position and distribution assumption

B. confidence level and the underlying stochastic process

C. confidence level, the holding period and expected volatility

D. confidence level and the holding period -

Question 158:

For a 10 year interest rate swap, what would be the worst time for a counterparty to default (in terms of the maximum likely credit exposure)

A. 10 years

B. Right after inception

C. 2 years

D. 7 years -

Question 159:

A loan portfolio's full notional value is $100, and its value in a worst case scenario at the 99% level of confidence is $65. Expected losses on the portfolio are estimated at 10%. What is the level of economic capital required to cushion unexpected losses?

A. 25

B. 65

C. 10

D. 35 -

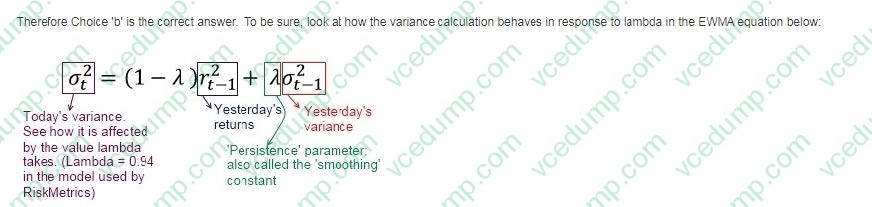

Question 160:

As the persistence parameter under EWMA is lowered, which of the following would be true:

A. The model will react slower to market shocks

B. The model will react faster to market shocks

C. High variance from the recent past will persist for longer

D. The model will give lower weight to recent returns

Related Exams:

-

8002

PRM Certification - Exam II: Mathematical Foundations of Risk Measurement -

8004

PRM Certification - Exam IV: Case Studies; Standards: Governance, Best Practices and Ethics -

8006

Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition -

8007

Exam II: Mathematical Foundations of Risk Measurement - 2015 Edition -

8008

PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

8009

Exam IV: Case Studies: Standards: Governance, Best Practices and Ethics - 2015 Edition -

8010

Operational Risk Manager (ORM) -

8011

Credit and Counterparty Manager (CCRM) Certificate

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only PRMIA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your 8008 exam preparations and PRMIA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.