8008 Exam Details

-

Exam Code

:8008 -

Exam Name

:PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

Certification

:PRMIA Certifications -

Vendor

:PRMIA -

Total Questions

:362 Q&As -

Last Updated

:Jul 15, 2026

PRMIA 8008 Online Questions & Answers

-

Question 101:

For an option position with a delta of 0.3, calculate VaR if the VaR of the underlying is $100.

A. 100

B. 130

C. 30

D. 33.33 -

Question 102:

If an institution has $1000 in assets, and $800 in liabilities, what is the economic capital required to avoid insolvency at a 99% level of confidence? The VaR in respect of the assets at 99% confidence over a one year period is $100.

A. 200

B. 1000

C. 100

D. 1100 -

Question 103:

What would be the consequences of a model of economic risk capital calculation that weighs all loans equally regardless of the credit rating of the counterparty?

A. Create an incentive to lend to the riskiest borrowers II. Create an incentive to lend to the safest borrowers III. Overstate economic capital requirements IV. Understate economic capital requirements

B. III only

C. I and IV

D. II and III

E. I only -

Question 104:

Under the actuarial (or CreditRisk+) based modeling of defaults, what is the probability of 4 defaults in a retail portfolio where the number of expected defaults is 2?

A. 4%

B. 18%

C. 9%

D. 2% -

Question 105:

A bank expects the error rate in transaction data entry for a particular business process to be 0.005%. What is the range of expected errors in a day within +/- 2 standard deviations if there are 2,000,000 such transactions each day?

A. 80 to 120 errors in a day

B. 60 to 80 errors in a day

C. 0 to 200 errors in a day

D. 90 to 110 errors in a day -

Question 106:

Which of the following statements is true:

A. Both total expected losses and total unexpected losses are less than the sum of expected and unexpected losses on underlying exposures respectively

B. Total expected losses are equal to the sum of individual underlying exposures while total unexpected losses are greater than the sum of unexpected losses on underlying exposures

C. Total expected losses are equal to the sum of expected losses in the individual underlying exposures while total unexpected losses are less than the sum of unexpected losses on underlying exposures

D. Total expected losses are greater than the sum of individual underlying exposures while total unexpected losses are less than the sum of unexpected losses on underlying exposures -

Question 107:

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that none of the three bonds will default.

A. 94%

B. 0.11%

C. 0.0006%

D. 2% -

Question 108:

Which of the following is not an event of default covered in the ISDA Master Agreement?

I - failure to pay or deliver II - credit support default III - merger without assumption IV - Bankruptcy

A. All are considered events of default

B. II and III

C. I

D. IV -

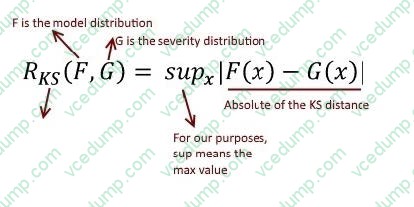

Question 109:

Which of the following is closest to the description of a 'risk functional'?

A. A risk functional is the distribution that models the severity of a risk

B. A risk functional is a model distribution that is an approximation of the true loss distribution of a risk

C. Risk functional refers to the Kolmogorov-Smirnov distance

D. A risk functional assigns a penalty value for the difference between a model distribution and a risk's severity distribution -

Question 110:

A risk analyst attempting to model the tail of a loss distribution using EVT divides the available dataset into blocks of data, and picks the maximum of each block as a data point to consider.

Which approach is the risk analyst using?

A. Block Maxima approach

B. Peak-over-thresholds approach

C. Expected loss approach

D. Fourier transformation

Related Exams:

-

8002

PRM Certification - Exam II: Mathematical Foundations of Risk Measurement -

8004

PRM Certification - Exam IV: Case Studies; Standards: Governance, Best Practices and Ethics -

8006

Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition -

8007

Exam II: Mathematical Foundations of Risk Measurement - 2015 Edition -

8008

PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

8009

Exam IV: Case Studies: Standards: Governance, Best Practices and Ethics - 2015 Edition -

8010

Operational Risk Manager (ORM) -

8011

Credit and Counterparty Manager (CCRM) Certificate

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only PRMIA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your 8008 exam preparations and PRMIA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.