AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 921:

When an auditor concludes there is substantial doubt about a continuing audit client's ability to continue as a going concern for a reasonable period of time, the auditor's responsibility is to:

A. Issue a qualified or adverse opinion, depending upon materiality, due to the possible effects on the financial statements. B. Consider the adequacy of disclosure about the client's possible inability to continue as a going concern. C. Report to the client's audit committee that management's accounting estimates may need to be adjusted. D. Reissue the prior year's auditor's report and add an explanatory paragraph that specifically refers to "substantial doubt" and "going concern."

B. Consider the adequacy of disclosure about the client's possible inability to continue as a going concern. Choice "b" is correct. When an auditor concludes there is substantial doubt about an entity's ability to continue as a going concern for a reasonable period of time, the auditor's responsibility is to consider the adequacy of disclosure about the entity's possible inability to continue as a going concern and include an explanatory paragraph in the audit report. Choice "a" is incorrect. The auditor would include an explanatory paragraph following the unqualified opinion, or disclaim an opinion due to a material uncertainty. A qualified or adverse opinion is not appropriate for doubt about an entity's ability to continue as a going concern. Choice "c" is incorrect. Management's accounting estimates are unrelated to going concern issues. Choice "d" is incorrect. Going concern issues are considered prospectively. It is not appropriate to reissue a prior audit report if doubt arises about an entity's ability to continue in a future period.

Question 922:

Which of the following procedures would an auditor most likely perform to test controls relating to management's assertion about the completeness of cash receipts for cash sales at a retail outlet?

A. Observe the consistency of the employees' use of cash registers and tapes. B. Inquire about employees' access to recorded but undeposited cash. C. Trace the deposits in the cash receipts journal to the cash balance in the general ledger. D. Compare the cash balance in the general ledger with the bank confirmation request.

A. Observe the consistency of the employees' use of cash registers and tapes. Choice "a" is correct. Observing the consistent use of cash registers and tapes by employees would provide evidence to the auditor regarding the controls over the completeness of cash receipts. Choices "b", "c", and "d" are incorrect. The completeness assertion relates to the recording of all transactions. Inquiries about access to recorded cash, tracing from the cash receipts journal, and testing the general ledger balance do not provide evidence regarding possible unrecorded transactions.

Question 923:

In which type of business entity is the entire ownership interest most freely transferable?

A. General partnership. B. Limited partnership. C. Corporation. D. Limited liability company.

C. Corporation. Choice "c" is correct. Among the business entities listed, entire ownership interests are most freely transferable in a corporation. Unless transferability is restricted by contract (restricted shares or voting trusts or voting agreements), there are no restrictions on the sale of corporate stock (the common stock represents the stockholders' ownership interest). The right to transfer ownership interests freely is one of the advantages of the corporate form of business. Choice "a" is incorrect. A general partner in a general partnership may assign his or her right to receive profits or surplus. A general partner cannot assign his interest and confer partnership status on the assignee without unanimous consent of all other partners. Choice "b" is incorrect. Both general partners and limited partners in a limited partnership may assign the right to receive profits and surplus. Neither general nor limited partners can confer general or limited partnership status on the assignee without the unanimous consent of all general and all limited partners. Choice "d" is incorrect. In most states, limited liability company (LLC) members may not sell and confer ownership interest without the consent of all LLC members.

Question 924:

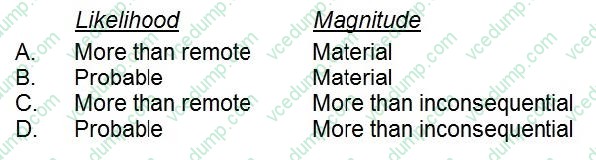

For a nonissuer, a control deficiency would be considered a material weakness when the likelihood and magnitude of potential financial statement misstatements are:

A. Option A B. Option B C. Option C D. Option D

A. Option A Choice "a" is correct. A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement of the entity's financial statements will not be prevented or detected. Choices "b", "c", and "d" are incorrect, based on theabove.

Question 925:

The summary of significant accounting policies should disclose the:

A. Maturity dates of noncurrent debts. B. Terms for convertible debt to be exchanged for common stock. C. Concentration of credit risk of all financial instruments by geographical region. D. Criteria for determining which investments are treated as cash equivalents.

D. Criteria for determining which investments are treated as cash equivalents. Choice "d" is correct. The criteria for determining which investments are treated as cash equivalents would be part of the summary of significant accounting policies. Choice "a" is incorrect. The maturity dates of noncurrent debts are required disclosures, but are not a part of the summary of significant accounting policies. Choice "b" is incorrect. The terms for convertible debt to be exchanged for common stock are not accounting policies; they would be disclosed separately. Choice "c" is incorrect. The concentration of credit risk of all financial instruments by geographic region may be a required segment disclosure, especially for financial institutions. However, it would not be a part of the summary of significant accounting policies.

Question 926:

The level of safety stock in inventory management depends on all of the following, except the:

A. Level of uncertainty of the sales forecast. B. Level of customer dissatisfaction for back orders. C. Level of uncertainty in lead-time for stock shipments. D. Cost to reorder stock.

D. Cost to reorder stock. Choice "d" is correct. Reorder costs do not impact the level of safety stock. Choices "a", "b", and "c" are incorrect. Safety stock levels are affected by: 1. Uncertain sales forecasts - greater uncertainty means a higher level of safety stock should be carried. 2. Dissatisfaction of customers - if customers are dissatisfied with back orders (which occur when there are stock outs), then more safety stock should be carried to prevent stock outs. 3. Uncertain lead times - greater uncertainty means a higher level of safety stock is needed.

Question 927:

A change in credit policy has caused an increase in sales, an increase in discounts taken, a reduction in the investment in accounts receivable, and a reduction in the number of doubtful accounts. Based upon this information, we know that:

A. Net profit has increased. B. The average collection period has decreased. C. Gross profit has declined. D. The size of the discount offered has decreased.

B. The average collection period has decreased. Choice "b" is correct. Whenever accounts receivable (AR) are decreasing when sales are increasing (and the decrease in AR is not due to an increase in bad debt write offs), this would indicate that the average collection period for AR has decreased. Choices "a", "c", and "d" are incorrect. There is insufficient information in the question to draw conclusions about these items.

Question 928:

ABC Manufacturers uses a performance reporting system that combines both financial and nonfinancial measures to evaluate division performance. All of the following measure operational efficiency, except:

A. Operating leverage. B. Days' sales in accounts receivables. C. Inventory turnover. D. Residual income.

D. Residual income. Choice "d" is correct. Residual income measures profitability in excess of a target rate of return. Operational efficiency is not considered. Choices "a", "b", and "c" are incorrect. Operating leverage, days' sales in accounts receivable, and inventory are all measures of operational efficiency, specifically, efficiency in managing working capital.

Question 929:

In a competitive market an increase in the minimum wage will likely have the following effects:

A. The general (or aggregate) demand for labor will increase; however, the quantity demanded will remain unchanged. B. The general (or aggregate) supply of labor will increase; however, the quantity supplied will remain unchanged. C. The general (or aggregate) demand for labor will remain unchanged; however, the quantity demanded will decrease. D. The general (or aggregate) supply of labor will remain unchanged; however, the quantity supplied will decrease.

C. The general (or aggregate) demand for labor will remain unchanged; however, the quantity demanded will decrease. Choice "c" is correct. The general (or aggregate) demand for labor will remain unchanged; however, the quantity demanded will decrease. Choice "a" is incorrect, per for choice "c" above. Choices "b" and "d" are incorrect. The general (or aggregate) supply of labor will remain unchanged; however, the quantity supplied will increase.

Question 930:

What is the effect when a foreign competitor's currency becomes weaker compared to the U.S. dollar?

A. The foreign company will have an advantage in the U.S. market. B. The foreign company will be disadvantaged in the U.S. market. C. The fluctuation in the foreign currency's exchange rate has no effect on the U.S. company's sales or cost of goods sold. D. It is better for the U.S. company when the value of the U.S. dollar strengthens.

A. The foreign company will have an advantage in the U.S. market. Choice "a" is correct. As a foreign competitor's currency becomes weaker compared to the U.S. dollar, the product becomes less expensive in U.S. dollars. The less expensive product will have the advantage in the U.S. market. Choice "b" is incorrect. As a foreign competitor's currency becomes weaker compared to the U.S. dollar, the product becomes less expensive in U.S. dollars. The less expensive product will have the advantage in the U.S. market, not a disadvantage. Choice "c" is incorrect. Foreign currency exchange rates impact both sales and possibly cost of goods sold of a competing domestic company. Sales within U.S. markets will deteriorate as the currency of foreign competitors deteriorates and makes the domestic company's goods more expensive. As a foreign competitor's currency appreciates, sales within U.S. markets by a domestic company should also increase as goods manufactured in the U.S. become less expensive. Cost of goods sold may fluctuate if foreign suppliers are used. Choice "d" is incorrect. It is better for a U.S. company when the value of the U.S. dollar weakens, not strengthens. A weak U.S. dollar makes domestic goods relatively less expensive that imported goods.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.