AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 881:

In its annual report to shareholders, ABC Co. included a separate management report that contained additional information. ABC's auditor is expressing an unqualified opinion on ABC's financial statements but has not been engaged to examine and report on this additional information. What is the auditor's responsibility concerning such a report?

A. The auditor should add an explanatory paragraph to the report on the financial statements disclaiming an opinion on the additional information. B. The auditor has no obligation to read the management report or to verify the accuracy or appropriateness of its contents. C. The auditor should request Lake to place the management report in its annual report where it will not be misinterpreted to be the auditor's assertion. D. The auditor should read the management report and consider whether it contains a material misstatement of fact.

D. The auditor should read the management report and consider whether it contains a material misstatement of fact. Choice "d" is correct. The auditor should read other information accompanying the basic financial statements and consider whether it contains a material inconsistency or material misstatement of fact. Choice "a" is incorrect. The auditor generally does not add a disclaimer paragraph in this situation. Choice "b" is incorrect. The auditor should read other information accompanying the basic financial statements and consider whether it contains a material inconsistency or material misstatement of fact. Choice "c" is incorrect. Even if the management report were included in the annual report, the auditor still has the same responsibility regarding both the management report and the annual report: the auditor should read the information and consider whether it contains a material inconsistency or material misstatement of fact.

Question 882:

When an independent CPA assists in preparing the financial statements of a publicly held entity, but has not audited or reviewed them, the CPA should issue a disclaimer of opinion. In such situations, the CPA has no responsibility to apply any procedures beyond:

A. Documenting that internal control is not being relied on. B. Reading the financial statements for obvious material misstatements. C. Ascertaining whether the financial statements are in conformity with GAAP. D. Determining whether management has elected to omit substantially all required disclosures.

B. Reading the financial statements for obvious material misstatements. Choice "b" is correct. The accountant is only required to read the financial statements for obvious material misstatements. Choice "a" is incorrect. The accountant need not document that internal control is not being relied on. Choices "c" and "d" are incorrect. The accountant is not required to evaluate conformity with GAAP, but any known departures (including inadequate disclosure) should be described in the disclaimer.

Question 883:

Under the Revised Model Business Corporation Act, which of the following statements regarding a corporation's bylaws is(are) correct?

A. A corporation's initial bylaws shall be adopted by either the incorporators or the board of directors. II. A corporation's bylaws are contained in the articles of incorporation. B. I only. C. II only. D. Both I and II. E. Neither I nor II.

A. A corporation's initial bylaws shall be adopted by either the incorporators or the board of directors. II. A corporation's bylaws are contained in the articles of incorporation. Choice "a" is correct. Under the Revised Model Business Corporation act, a corporation's initial bylaws may be adopted by either the incorporators or the board of directors. Choices "b" and "c" are incorrect, because the corporation's bylaws are a separate document not included in the corporation's articles of incorporation. Choice "d" is incorrect, because under the Revised Model Business Corporation Act, a corporation's initial bylaws may be adopted by either the incorporators or the board of directors.

Question 884:

The corporate veil is most likely to be pierced and the shareholders held personally liable if:

A. The corporation has elected S corporation status under the Internal Revenue Code. B. The shareholders have commingled their personal funds with those of the corporation. C. An ultra vires act has been committed. D. A partnership incorporates its business solely to limit the liability of its partners.

B. The shareholders have commingled their personal funds with those of the corporation. Choice "b" is correct. Generally, a corporation is treated as an entity distinct from its shareholders and shareholders are not liable for the corporation's debts. However, where the shareholders do not treat the corporation as a distinct entity, such as where they commingle their personal funds with the corporation's funds, courts are likely to ignore the corporate form as well. Choice "a" is incorrect. An election to be taxed like a partnership under Subchapter S is not grounds to pierce the corporate veil. Choice "c" is incorrect. An ultra vires act is one beyond the corporation's powers. The persons who authorized the ultra vires act can be held personally liable for damages caused, but it is not a ground for piercing the corporate veil. Choice "d" is incorrect. Limiting personal liability is the main reason to incorporate. It is a ground for piercing the corporate veil only if it is done fraudulently (i.e., to avoid paying present creditors).

Question 885:

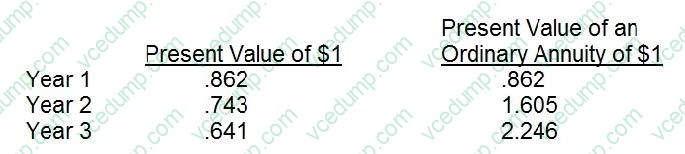

ABC Inc. is considering the purchase of a new machine that will cost $150,000. The machine has an estimated useful life of three years. Assume for simplicity that the equipment will be fully depreciated 30, 40, and 30 percent in each of the

three years, respectively. The new machine will have a $10,000 resale value at the end of its estimated useful life. The machine is expected to save the company $85,000 per year in operating expenses. ABC uses a 40 percent estimated

income tax rate and a 16 percent hurdle rate to evaluate capital projects.

Discount rates for a 16 percent rate are as follows:

The payback period for this investment would be:

A. 2.95 years B. 1.76 years C. 2.09 years D. 2.94 years

C. 2.09 years Explanation Explanation/Reference:Choice "c" is correct. 2.09 years payback period. At the beginning of year 3, $6,000 is needed to recover the investment. Because an inflow of $69,000 is expected throughout the year, only 6,000 ?69,000 = .09 years is needed to recover the $6,000. Thus, the payback is 2.09 years. The $6,000 in salvage is excluded from the totals for year 3. Amounts are not realized until the end of the year while savings and depreciation tax shield occur throughout the year and are relevant to the partial year payback.

Question 886:

ABC Co. manufactures and sells household products. ABC experienced losses associated with its small appliance group. Operations and cash flows for this group can be clearly distinguished from the rest of ABC's operations. ABC plans to sell the small appliance group with its operations. What is the earliest point at which ABC should report the small appliance group as a discontinued operation?

A. When ABC classifies it as held for sale. B. When ABC receives an offer for the segment. C. When ABC first sells any of the assets of the segment. D. When ABC sells the majority of the assets of the segment.

A. When ABC classifies it as held for sale. Choice "a" is correct. The earliest period that a component of an entity can be reported in discontinued operations is when the component meets the following "held for sale" criteria: 1. Management commits to a plan to sell the component. 2. The component is available for immediate sale in its present condition. 3. An active program to locate a buyer has been initiated. 4. The sale of the component is probable and the sale is expected to be completed within one year. 5. The sale of the component is being actively marketed. 6. It is unlikely that significant change to the plan to sell will be made or that the plan will be withdrawn. Choices "b", "c", and "d" are incorrect, per theabove.

Question 887:

Parker, whose spouse died during the preceding year, has not remarried. Parker maintains a home for a dependent child. What is Parker's most advantageous filing status?

A. Single. B. Head of household. C. Married filing separately. D. Qualifying widow(er) with dependent child.

D. Qualifying widow(er) with dependent child. Choice "d" is correct. A qualifying widow(er) is a taxpayer who may use the joint tax return standard deduction and rates (but not the exemption for the deceased spouse) for each of two taxable years following the year of death of his or her spouse, unless he or she remarries. The surviving spouse must maintain a household that, for the whole entire taxable year, was the principal place of abode of a son, stepson, daughter, or stepdaughter (whether by blood or adoption). The surviving spouse must also be entitled to a dependency exemption for such individual. Parker may file as a qualifying widow(er) since her spouse died in the previous tax year, she did not remarry and she maintained a home for a dependent child. Since, qualifying widow(er) is the most advantageous status and Parker qualifies, Parker would file as a qualifying widow(er). Choice "a" is incorrect. Even though Parker would qualify as single, filing single would give Parker a high tax liability than the qualifying widow(er) status and therefore is not most advantageous. Choice "b" is incorrect. Parker would not qualify as head of household for the first two years after the death of Parker's spouse because one of the requirements for Head of Household status is that the taxpayer is NOT a surviving spouse. (Also, note that the likely reason for this requirement is that filing as Head of Household status would give the qualifying surviving spouse taxpayer a higher tax liability than the Qualifying Widow(er) status, which would be less advantageous.). Choice "c" is incorrect. Parker would not qualify to file married filing separately.

Question 888:

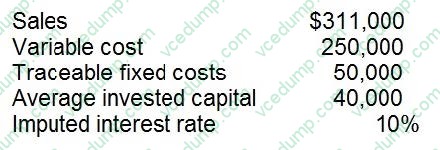

The following information pertains to ABC Co.'s Gold Division for 1993:

ABC's return on investment was:

A. 10.00 percent. B. 13.33 percent. C. 27.50 percent. D. 30.00 percent.

C. 27.50 percent. Explanation Explanation/Reference:Choice "c" is correct. Return on investment equals net income divided by average invested capital: Choices "a", "b", and "d" are incorrect, per the above calculation.

Question 889:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

In 1994, Joan received $3,500 as beneficiary of the death benefit, which was provided by her brother's employer. Joan's brother did not have a nonforfeitable right to receive the money while living.

A. $0 B. $500 C. $900 D. $1,000 E. $1,250 F. $1,300 G. $1,500 H. $2,000 I. $2,500 J. $3,000 K. $10,000 L. $25,000 M. $50,000 N. $55,000 O. $75,000

A. $0 "A" is correct. $0. Life insurance proceeds received by reason of the death of the insured are not taxable income to the recipient.

Question 890:

ABC, Inc. offers credit terms of 2/10, net 30 for its customers. Sixty percent of ABC's customers take the 2% discount and pay on day 10. The remainder of ABC's customers pay on day 30. How many days' sales are in ABC's accounts receivable?

A. 6 B. 12 C. 18 D. 20

C. 18 Choice "c" is correct. Days' sales in accounts receivable is normally calculated as Days' sales = Ending accounts receivable / Average daily sales. However, that formula will not work in this case because the necessary information is not provided. However, enough information about payments is provided so that the total days' sales can be determined on a weighted average basis. In this question, nobody pays before the 10th day and 60% of the customers pay on the 10th day, so there are 10 x .60, or 6 day's sales there. The other 40% of the customers pay on the 30th day so there are 30 x .40, or 12 day's sales there. The total is 18 days sales. Choice "a" is incorrect. This answer is apparently calculated from just the 60% of the customers who pay on the 10th day. The others have to be included also. Choice "b" is incorrect. This answer is apparently calculated from just the 40% of the customers who pay on the 30th day. The others have to be included also. Choice "d" is incorrect. This answer is apparently calculated by as the difference between the 30th day and the 10th day. The answer does not take into account how many customers pay when.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.