CIMA-P1 Exam Details

-

Exam Code

:CIMA-P1 -

Exam Name

:P1 - Management Accounting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:275 Q&As -

Last Updated

:Jul 15, 2026

CIMA CIMA-P1 Online Questions & Answers

-

Question 201:

Explain why sensitivity analysis is useful when dealing with uncertainty in project appraisal. Select all the true statements.

A. Sensitivity analysis enables a company to determine the effect of changes to fixed costs on the planned outcome

B. Sensitivity analysis enables a company to determine the effect of changes to variables on the planned outcome

C. In project appraisal, an analysis can be made if all the key variables to ascertain by how much variable would need to change before the net present value (NPV) reaches zero i.e.the indifference point.

D. In project appraisal, in analysis can be made of all the key variables to ascertain by how much each variable would need to change before the net present value (NPV) reaches 100% i.e. the maximum point. -

Question 202:

The simplex method has been used to determine the optimum output of products P, Q, R and S with constraints on resources J, K and L.

In the final simplex tableau, the figure in the product R row and the column for slack variable K is 80.

Which of the following statements is correct?

A. For each additional unit of resource K available, the contribution would increase by $80.

B. For each additional unit of resource K available, the output of product R would increase by 80 units.

C. For each additional unit of product R produced, 80 additional units of resource K would be required.

D. In the optimum solution, 80 units of resource K are unused. -

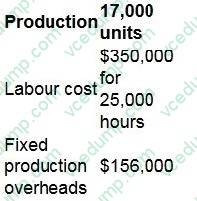

Question 203:

The standard production cost of making a product is as follows:

What is the fixed production overhead capacity variance?

A. $9,000F

B. $6,000F

C. $3,000F

D. $6,000A -

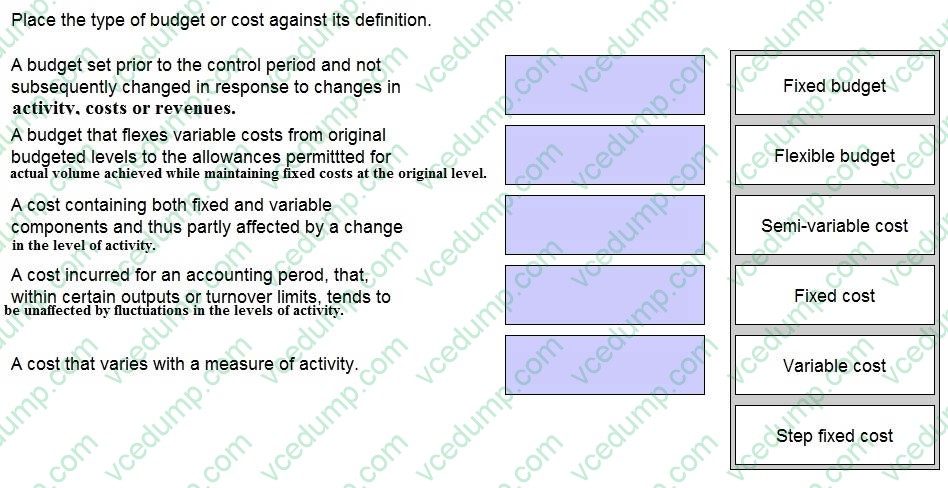

Question 204:

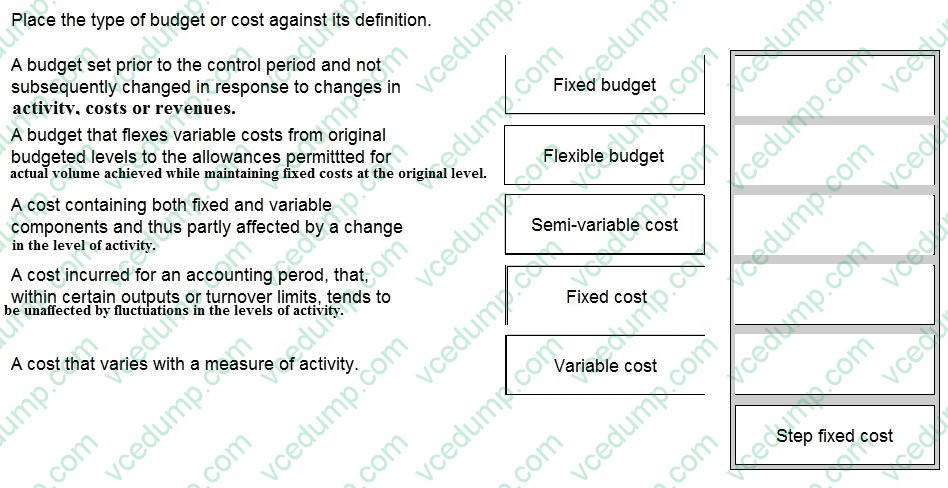

DRAG DROP

Place the type of budget or cost against its definition.

Select and Place:

-

Question 205:

A company manufactures headphones.

70% of production costs are prime costs. Production overhead costs are driven by the number of headphones produced.

Which costing system would be most appropriate for product profitablilty analysis?

A. Absorption costing

B. Marginal costing

C. Activity based costing

D. Relevant costing -

Question 206:

CDF is a manufacturing company within the DF group. CDF has been asked to provide a quotation for a contract for a new customer and is aware that this could lead to further orders. As a consequence, CDF will produce the quotation by using relevant costing instead of its usual method of full cost plus pricing. The following information has been obtained in relation to the contract: Material D 40 tons of material D would be required. This material is in regular use by CDF and has a current purchase price of $38 per ton. Currently, there are 5 tons in inventory which cost $35 per ton. The resale value of the material in inventory is $24 per ton.

Components 4,000 components would be required. These could be bought externally for $15 each or alternatively they could be supplied by RDF, another company within the DF manufacturing group. The variable cost of the component if it were manufactured by RDF would be $8 per unit, and RDF adds 30% to its variable cost to contribute to its fixed costs plus a further 20% to this total cost in order to set its internal transfer price. RDF has sufficient capacity to produce 2,500 components without affecting its ability to satisfy its own external customers. However, in order to make the extra 1,500 components required by CDF, RDF would have to forgo other external sales of $50,000 which have a contribution to sales ratio of 40%.

Labour hours 850 direct labour hours would be required. All direct labour within CDF is paid on an hourly basis with no guaranteed wage agreement. The grade of labour required is currently paid $10 per hour, but department W is already working at 100% capacity. Possible ways of overcoming this problem are: ?Use workers in department Z, because it has sufficient capacity. These workers are paid $15 per hour. ?Arrange for sub-contract workers to undertake some of the other work that is performed in department W. The sub- contract workers would cost $13 per hour.

Specialist machine The contract would require a specialist machine. The machine could be hired for $15,000 or it could be bought for $50,000. At the end of the contract if the machine were bought, it could be sold for $30,000. Alternatively, it could be modified at a cost of $5,000 and then used on other contracts instead of buying another essential machine that would cost $45,000. The operating costs of the machine are payable by CDF whether it hires or buys the machine. These costs would total $12,000 in respect of the new contract.

Supervisor The contract would be supervised by an existing manager who is paid an annual salary of $50,000 and has sufficient capacity to carry out this supervision. The manager would receive a bonus of $500 for the additional work.

Development time 15 hours of development time at a cost of $3,000 have already been worked in determining the resource requirements of the contract.

Fixed overhead absorption rate CDF uses an absorption rate of $20 per direct labour hour to recover its general fixed overhead costs. This includes $5 per hour for depreciation.

Calculate the relevant cost of the contract to CDF. You must present your answer in a schedule that clearly shows the relevant cost value for each of the items identified above. You should also explain each relevant cost value you have included in your schedule and why any values you have excluded are not relevant.

Ignore taxation and the time value of money.

Select all the true statements.

A. Machine operating costs is a relevant cost.

B. Development Cost is a relevant cost.

C. General fixed overhead costs are relevant costs.

D. Direct labour cist is a relevant cost

E. The total relevant cost was $84 990

F. The total relevant cost was $94 740

G. The total relevant cost was $104 320 -

Question 207:

You are a trainee management accountant working for a prestigious manufacturing firm. One day you go to a business meeting a business meeting and the managing director is there. They stand up and say that the company is losing too much money through wastage and losses and so they have decided to implement a total quality management system. They go on to say this system will: 1:Allow the company to improve on a consistent and continual basis 2:Allow the company to identify and allocate quality accountability to certain departments 3:Help the company detect error and fraud Are ALL of these statements correct?

A. No. (2) is incorrect No. (1) is incorrect

B. Yes. They ore all correct

C. No. (1) and (2) are incorrect.

D. No. (3) and (2) are incorrect. -

Question 208:

The term `budgetary slack' refers to the:

A. Lead time between the preparation of the functional budgets and the approval of the master budget by senior management

B. Difference between the budgeted output and the actual output

C. Difference between budgeted capacity utilization and full capacity

D. Intentional over estimation of costs and/or under estimation of revenue in a budget -

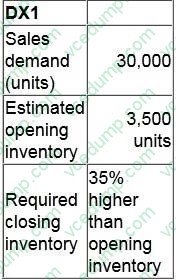

Question 209:

PQR is preparing the production budget for one of its products, the DX1, for the forthcoming year. The following information is available:

How many units of the DX1 will need to be produced in the forthcoming year?

A. 28,775

B. 30,000

C. 31,225

D. 38,225 -

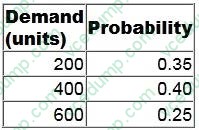

Question 210:

CORRECT TEXT

The daily demand for a perishable product has the following probability distribution:

Each unit of the product costs $6 and is sold for $10.

Unsold items are thrown away at the end of the day.

Orders must be placed each morning before the daily demand is known.

The payoff table below shows the profit that would be earned for each of the combinations of purchases and demand.

The number of units that should be purchased at the beginning of each day in order to maximize expected profit is:

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-P1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.