CIMA-F1 Exam Details

-

Exam Code

:CIMA-F1 -

Exam Name

:F1 - Financial Reporting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:265 Q&As -

Last Updated

:May 26, 2026

CIMA CIMA-F1 Online Questions & Answers

-

Question 201:

An entity has an inventory holding period of 52 days. This means that the inventory:

A. takes 52 days to arrive after it has been ordered.

B. stays in the entity's warehouse for an average of 52 days before it is sold.

C. takes 52 days to manufacture.

D. takes 52 days to be paid for. -

Question 202:

XY is an entity incorporated in Country B but operates in several countries. Monthly management meetings to decide on strategic matters take place in Country A, where the majority of its production happens. XY sells most of its goods to Country

C.

In accordance with the Organization for Economic Co-operation and Development (OECD) rules on corporate residence which of the following statements is true?

A. XY is resident in Country B because this is the country of its incorporation.

B. XY is resident in Country C because this is the country where XY generates most of its revenue.

C. XY is resident in Country A because this is the country of its effective management.

D. XY is resident in Country A because this is the country where XY undertakes most of its production. -

Question 203:

The tax rules in a country state that all tax returns must be filed by 31 March each year and that any outstanding tax balance must be paid by 14 April each year. An entity filed its tax return on 10 April 20X2 and paid the outstanding tax on 20 April 20X2. Which TWO of the following powers is the tax authority likely to have in respect of these actions by the entity?

A. Charge a fixed penalty for late submission of the tax return.

B. Charge interest for non-payment of the outstanding tax balance between 14 April 20X2 and 20 April 20X2.

C. Charge interest for non-payment of the outstanding tax balance between 31 March 20X2 and 20 April 20X2.

D. Charge interest for non-payment of the outstanding tax balance between 10 April 20X2 and 20 April 20X2.

E. Seize the assets of the entity. -

Question 204:

On 31 March 20X1 OP decided to sell a property. On that date this property was correctly classified as held for sale in accordance with IFRS 5 Non-Current Assets Held For Sale And Discontinued Operations.

In the draft financial statements of OP for the year ended 31 October 20X1 this property has been included at its fair value, which was $520,000 lower than its carrying value. This has resulted in a charge to profit or loss, the result of which is that the draft financial statements show a loss of $450,000 for the year to 31 October 20X1. When the management board of OP reviewed the draft financial statements it was unhappy about the loss and decided that the property should be reclassified as a non-current asset and reinstated to its original value, despite the fact that its plans for the property had not changed.

In accordance with the ethical principle of professional competence and due care, which THREE of the following statements explain how this property should be accounted for in the financial statements of OP for the year ended 31 October 20X1?

A. The property should be treated as a non-current asset held for sale from 31 March 20X1.

B. The property should be treated as a non-current asset held for sale from 1 November 20X1.

C. The property should not be depreciated after 31 March 20X1.

D. The impairment of $520,000 should be shown as an expense in the statement of profit or loss.

E. The property should be depreciated until 31 October 20X1.

F. The property impairment should not be recorded until the sale has completed. -

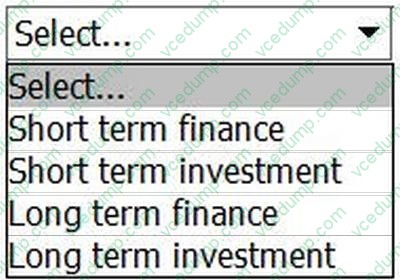

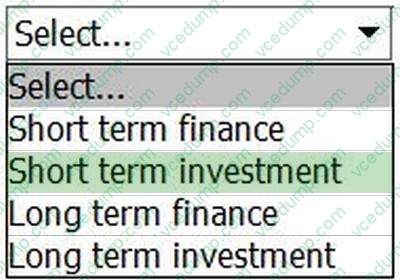

Question 205:

HOTSPOT

What is the correct classification of a 90-day government bond?

-

Question 206:

Which THREE of the following statements about government grants are INCORRECT?

A. A grant is recognised as revenue

B. Grants must not be deducted from the related expenses in financial statements

C. Capital grants relate to cash inflow and outflow

D. A compensatory grant should be recognised in statements when it is received, not when the expenses it applies to occurred

E. A grant is recognised only when there is reasonable assurance that the entity will comply with any conditions attached to the grant -

Question 207:

Extreme nepotism within Company E shows a failure to correctly observe which of the following principles of corporate governance?

A. Role and responsibilities of the board

B. Rights and equitable treatment of shareholders

C. Interests of other stakeholders

D. Integrity and ethical behaviour

E. Disclosure and transparency -

Question 208:

Which TWO of the following are implications of employee income tax being paid to the tax authority through a Pay-As-You-Earn scheme?

A. The government can budget its cash flows more easily.

B. The risk of employees defaulting on the payment of tax due is reduced

C. The tax authority deals directly with the employees rather than the employers.

D. The tax is paid after the employee completes a tax return.

E. Most of the administrative costs of collecting the tax are borne by the tax authority -

Question 209:

The International Accounting Standards Board's "The Conceptual Framework for Financial Reporting" (known as The Conceptual Framework) states that "faithful representation" is a fundamental qualitative characteristic. In accordance with the Conceptual Framework which of the following is NOT part of faithful representation?

A. Complete

B. Neutral

C. Free from error

D. Comparable -

Question 210:

At 31 December 20X4 the directors of MNO decide to revalue its property. Before revaluation adjustments the balances relating to property are as follows:

The property has been revalued at $1,600,000.

How much will be included within MNO's statement of financial position at 31 December 20X4 for revaluation surplus?

A. $400,000

B. $1,190,000

C. $1,600,000

D. $810,000

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-F1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.