CIMA-F1 Exam Details

-

Exam Code

:CIMA-F1 -

Exam Name

:F1 - Financial Reporting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:265 Q&As -

Last Updated

:May 26, 2026

CIMA CIMA-F1 Online Questions & Answers

-

Question 191:

From the list below identify the item that appears in the statement of financial position.

A. The amount of interest charged on loans during the year.

B. The amount of loans outstanding at the year end.

C. The amount of loans repaid during the year.

D. The amount of interest actually paid during the year. -

Question 192:

Which of the following statements about trade payables management is false?

A. Trade payables are an important source of finance.

B. When goods are in short supply customers who pay immediately are likely to be given priority over customers who take credit.

C. Trade payables should be paid as quickly as possible.

D. Goods or services may be more costly if extended credit is required. -

Question 193:

FILL IN THE BLANK

During the year a piece of equipment that originally cost $96,000, with accumulated depreciation of $39,000, met the criteria of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations to be classified as held for sale.

The equipment is being advertised for sale at $46,000 and costs of $1,000 will be incurred to enable the sale to be completed.

At what value should the equipment be included in the statement of financial position at the year end assuming that it remains unsold?

Give your answer to the nearest whole number.

-

Question 194:

FILL IN THE BLANK

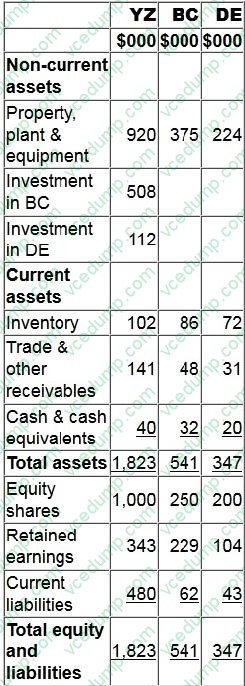

Statements of financial position for YZ, BC and DE at 31 March 20X2 include the following balances:

YZ purchased 90% of BC's equity shares for $508,000 on 1 January 20X2. On 1 January 20X2 BC's retained earnings were $183,000. YZ uses the proportion of net assets method to value non-controlling interest at acquisition.

YZ purchased 30% of DE's equity shares on 1 April 20X1 for $112,000. DE's retained earnings at 1 April 20X1 were $88,000.

On 1 February 20X2 YZ sold goods to BC for $28,000 at a mark up of 25% on cost. All the goods were still in BC's inventory at 31 March 20X2. Calculate the value of inventory that will be included in YZ's consolidated statement of financial position at 31 March 20X2. Give your answer to the nearest whole $.

-

Question 195:

Which of the following is correct?

The primary purpose of a cash budget prepared on a monthly basis is to determine:

A. next month's sales volumes.

B. the amount of inventory to purchase in the following month.

C. when to pay employees salaries.

D. whether there will be sufficient cash in the bank to meet requirements. -

Question 196:

Which of the following is NOT an appropriate description of the meaning of the term incidence of tax?

A. It refers to the distribution of the tax burden.

B. It only relates to the person or entity that actually pays the tax authorities.

C. It can be formal or actual.

D. It relates to the person or entity that ultimately bears the cost of the tax. -

Question 197:

FILL IN THE BLANK

An entity bought a capital item for $110,000 on 1 March 20X4 incurring legal fees at the date of purchase of $2,500.

On 1 May 20X4 additional costs classified as capital expenditure by the tax rules of the country of $25,000 were incurred in respect of the asset. On 1 June 20X4 repairs not classified as capital expenditure were incurred at a cost of $15,000.

The asset was sold for $250,000 on 30 November 20X8 and costs to sell were incurred of $4,300.

Calculate the chargeable gain on the disposal.

Give your answer to the nearest $.

-

Question 198:

In accordance with the Conceptual Framework for Financial Reporting, which TWO of the following qualitative characteristics of useful financial information should be considered when selecting a measurement basis?

A. Relevance

B. Comparability

C. Verifiability

D. Faithful representation

E. Timeliness -

Question 199:

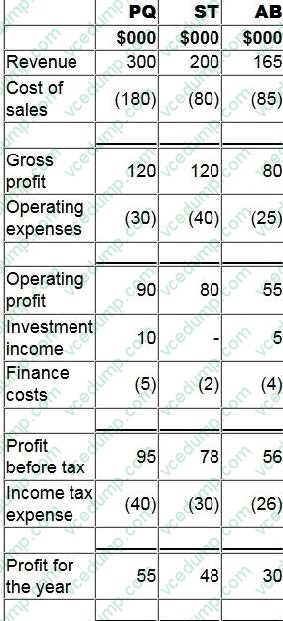

The statement of profit or loss for PQ, ST and AB for the year ended 31 December 20X0 are shown below:

1.PQ acquired 80% of its subsidiary, ST, on 1 January 20X0 and 40% of its associate, AB, on 1 September 20X0.

2.Since acquistion PQ has sold goods to ST and AB for $20,000 and $30,000 respectively. At the year end both ST and AB have 50% of these goods remaining in inventory. PQ uses a mark-up of 20% on all of its sales.

3.Since acquisition the goodwill in respect of ST has been impaired by $8,000 and the investment in AB has been impaired by $2,000.

4.PQ uses the fair value method for non-controlling interest at acquisition.

What is the revenue figure to be included in PQ's consolidated statement of profit or loss for the year ended 31 December 20X0?

A. $450,000

B. $440,000

C. $480,000

D. $476,000 -

Question 200:

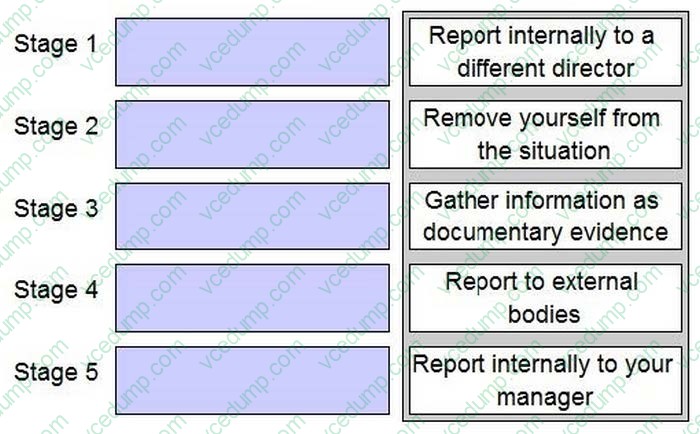

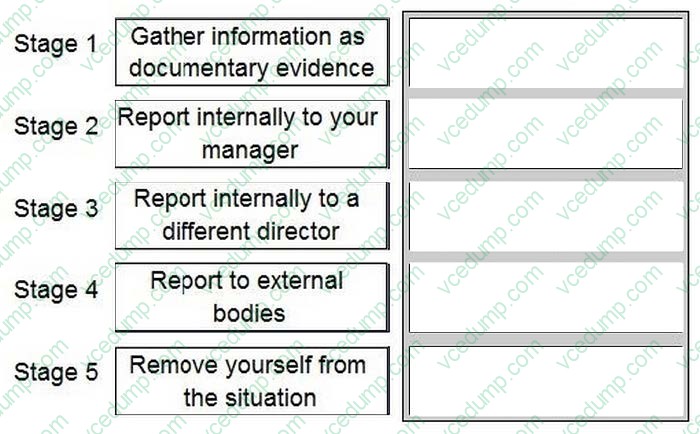

DRAG DROP

You work in the finance department of an entity. A director has approached you and asked you to falsify sales invoices which would significantly inflate revenue. The CIMA Code of Ethics suggests that you should deal with such an ethical dilemma by following a number of stages.

Place each of the stages identified below into chronological order.

Select and Place:

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-F1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.