CIMA-F1 Exam Details

-

Exam Code

:CIMA-F1 -

Exam Name

:F1 - Financial Reporting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:265 Q&As -

Last Updated

:May 26, 2026

CIMA CIMA-F1 Online Questions & Answers

-

Question 121:

FILL IN THE BLANK

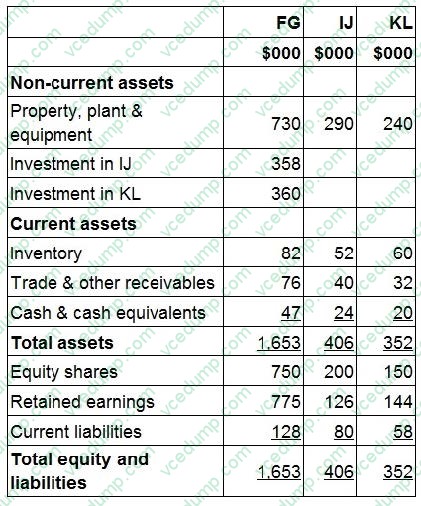

Statements of financial position for FG, IJ and KL at 31 December 20X5 include the following balances:

FG acquired 90% of IJ's equity shares for $358,000 on 1 July 20X5 when IJ's retained earnings were $98,000.

FG acquired 100% of KL's equity shares for $360,000 on 1 January 20X5 when KL's retained earnings were $155,000.

FG used the proportion of net assets method to value non-controlling interests at acquisition.

KL sold a piece of land to FG for $130,000 on 1 September 20X5. At the date of transfer the land had a carrying value of $50,000.

The management of FG expect KL to make profits in the future and no impairment ot its goodwill was proposed at 31 December 20X5.

Calculate the total goodwill to be included in FG's consolidated statement of financial position as at 31 December 20X5. Give your answer to the nearest whole $.

-

Question 122:

Which THREE of the following are part of the International Accounting Standards Committee (IASC) Foundation structure?

A. International Accounting Standards Board

B. Standards Advisory Council

C. International Financial Reporting Interpretations Committee

D. International Organisation of Securities Commission

E. Standards Application Council

F. International Financial Reporting Evaluations Committee -

Question 123:

If an entity makes a capital loss in a period, which of the following is the most likely way that will be allowed for relieving that capital loss?

A. Carry forward and set against future capital gains.

B. Use group loss relief to transfer the capital loss to another group entity.

C. Carry backwards and set against previous years trading profits.

D. Carry forward and set against future trading profits -

Question 124:

The legislation in Country S provides for an indexation allowance in the calculation of capital tax. STU operates in Country S where the indexation factor for the period 1 January 20X1 to 31 December 20X6 is 20% STU purchased a building for $64,000 on 1 January 20X1, incurring legal fees of $4,000. STU sold the building for $86,000 on 31 December 20X6 before selling fees of $3,500

What is the chargeable capital gam arising on STU's disposal of the building?

A. S11,600

B. $5,700

C. S900

D. $200 -

Question 125:

LM is preparing its cash forecast for the next three months. Which of the following items should be left out of its calculations?

A. Tax payment due, that relates to last year's profits.

B. Receipt of a new bank loan raised for the purpose of purchasing new machinery.

C. Expected loss on the disposal of a piece of land.

D. Rental payment on a leased vehicle. -

Question 126:

FILL IN THE BLANK

UK purchased an asset, with a useful economic life of 10 years, on 1 January 20X5 for $40,000. The asset was revalued on 31 December 20X6 to 544,000 and the directors believed its total useful economic life remained unchanged On 31 December 20X7 UK sells the asset for $50,000

How much will be recorded as a profit on disposal of the asset in UK's statement of profit or loss for the year ended 31 December 20X7?

Give your answer to the nearest $.

-

Question 127:

FILL IN THE BLANK

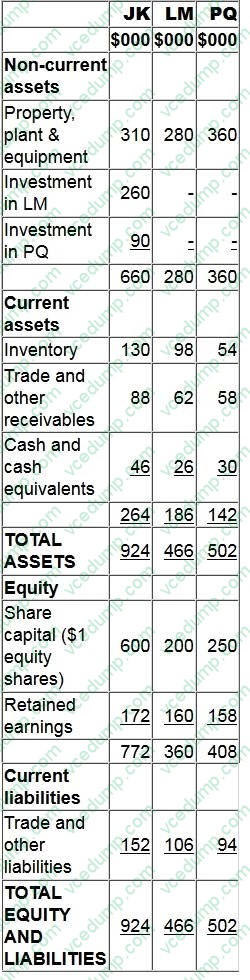

Statements of financial position as at 31 December 20X8 for JK, LM and PQ are as follows:

[1] JK purchased 80% of LM's $1 equity shares on 1 January 20X8 for $260,000 when the retained earnings of JK were $110,000. At that date the non-controlling interest had a fair value of $63,000.

[2] JK purchased 25% of PQ's $1 equity shares on 1 January 20X8 for $90,000 when the retained earnings of PQ were $96,000.

[3] During the year JK sold goods to LM for $32,000 at a mark up of 33.33% on cost. Half of the goods were still in LM's inventory at 31 December 20X8.

[4] LM transferred $32,000 to JK on 30 December 20X8 in settlement of the inter-group trade. JK did not record the cash in its financial records until 2 January 20X9.

Calculate the value of inventory that would be included in JK's consolidated statement of financial position at 31 December 20X8.

Give your answer to the nearest $.

-

Question 128:

In accordance with IAS 2 Inventories, which of the following costs should NOT be included in inventory valuation?

A. Import duties

B. Factory overheads

C. Administrative costs not related to production

D. Freight-in costs -

Question 129:

DRAG DROP

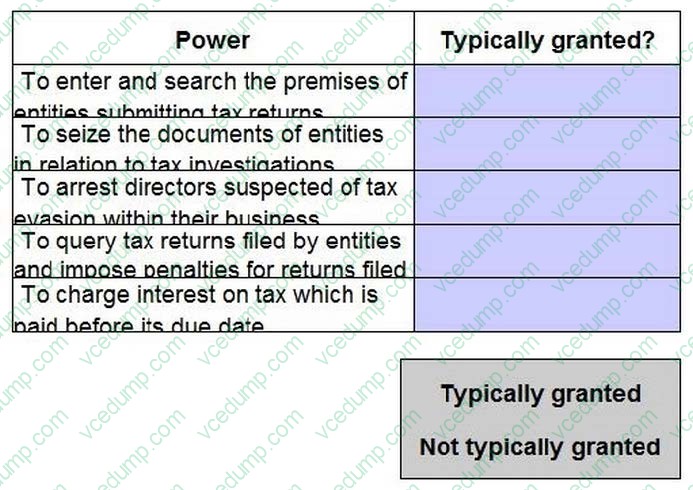

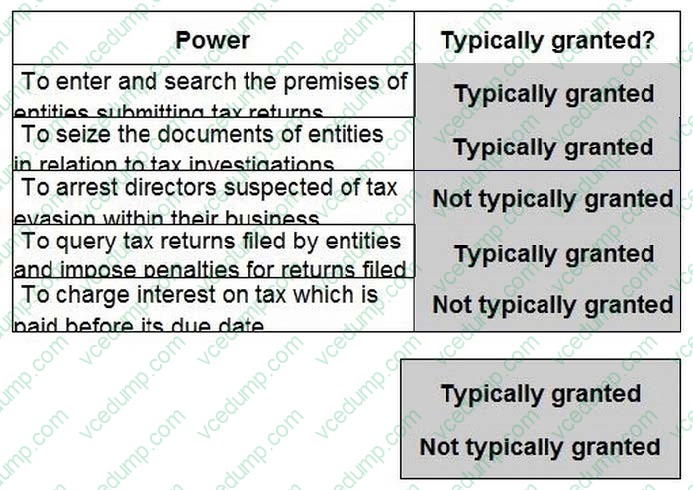

Identify which of the following are powers that a government would typically grant it's tax authority by placing the appropriate response beside each power.

Select and Place:

-

Question 130:

On 1 May 20X8 DEF enters into a contract to lease plant with a fair value of $200,000. Annual lease payments of $50,000 are to be paid in advance and DEF incurred direct costs to arrange the lease of S2.000 The present value of future lease payments at 1 May 20X8 is $190,000.

What is the amount to be recognised as a right-of-use asset on 1 May 20X8?

A. $192 000

B. $200,000

C. $240,000

D. $242000

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-F1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.