CIMA-F1 Exam Details

-

Exam Code

:CIMA-F1 -

Exam Name

:F1 - Financial Reporting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:265 Q&As -

Last Updated

:May 26, 2026

CIMA CIMA-F1 Online Questions & Answers

-

Question 111:

FILL IN THE BLANK

EFG purchased an asset on 1 January 20X5 for $24,000. On that date its useful life was 5 years and residual value was expected to be nil. EFG calculates depreciation on a pro-rata basis.

The asset is reclassified as held for sale on 1 October 20X8 and is unsold on 31 December 20X8.

It is expected that the asset will be sold for S6;300 and that selling costs will be S500

What is the amount that this asset will be included at in EFG's statement of financial position at 31 December 20X8?

Give your answer to the nearest $.

-

Question 112:

When calculating the gam chargeable to tax on the disposal of a building, which of the following would NOT be an allowable deduction?

A. Interest on a loan that was used to assist with its original purchase.

B. Costs of constructing an extension to the building.

C. Legal fees arising on the original purchase of the building.

D. Estate agent's fee payable on its sale. -

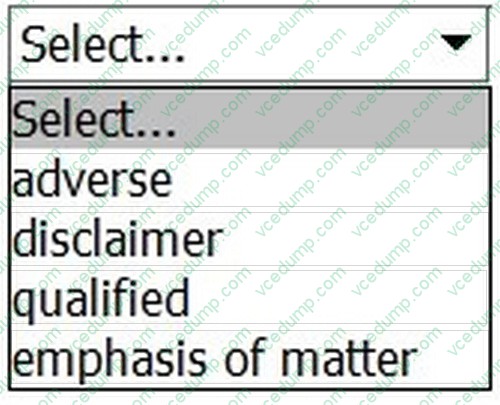

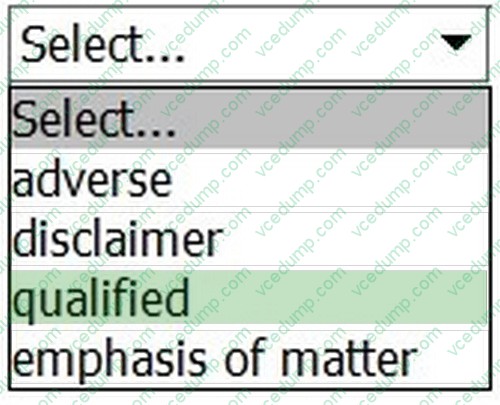

Question 113:

HOTSPOT

The auditor has identified a material but not pervasive mis-statement whilst undertaking the external audit of an entity's financial statements.

This will result in a modified audit report with the opinion being .

-

Question 114:

Which of the following is an example of a progressive tax?

A. Personal income tax of 10% on earnings up to $10,000, then at 15% over $10,001

B. Corporate income tax of 20% on earnings up to $100,000, then at 10% over $100,000

C. Corporate income tax of 20% on all earnings

D. Personal income tax of 10% and corporate income tax of 20% -

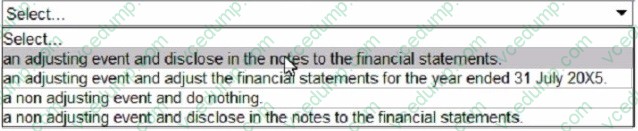

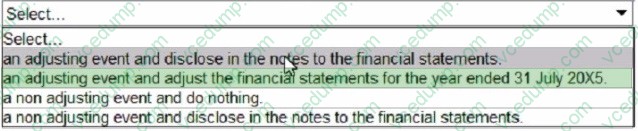

Question 115:

FILL IN THE BLANK

AB has prepared its financial statements for the year ended 31 July 20X5. On 15 September 20X5 a major fraud was uncovered by the external auditors which had taken place during the year to 31 July 20X5 The financial statements have not yet been authorised In accordance with IAS 10 Events After the Reporting Period, AB should treat the fraud as:

-

Question 116:

A non-executive director of a company is somebody who:

A. is involved in making operational decisions m the company

B. need not have experience of the industry in which the company operates

C. does not earn remuneration from the company

D. can be appointed Chief Executive Officer of the company. -

Question 117:

ABC Ltd has a gross profit margin of 30% and revenue of $500,000. What is its cost of sales?

A. $350,000

B. $150,000

C. $500,000

D. $200,000 -

Question 118:

In accordance with IFRS 3 Business Combinations, acquisition accounting of an investment in another entity within the consolidated statement of financial position means that the:

A. Parent's and 100% of the other entity's assets and liabilities are added together line by line.

B. Group's share of the net assets of the other entity are shown as one line under non- current assets.

C. Parent's and group share of the other entity's assets and liabilities are added together line by line.

D. Group's share of the net assets of the other entity are shown as one line within equity. -

Question 119:

The financial statements of JK for the year ended 31 August 20X4 were approved on 10 November 20X4. Within these financial statements which of the following would have been treated as a non- adjusting event in accordance with IAS 10 Events After the Reporting Period?

A. Inventory which was originally valued at its cost of $45,000 being sold for $37,000 in September 20X4.

B. A fire in JK's main warehouse on 3 September 20X4 destroying 60% of the inventory that had been held at the year end.

C. Notification received on 31 August that one of JK's major customers had gone into liquidation and was unlikely to pay any outstanding invoices.

D. The completion of a court case on 5 November 20X4 in which JK was ordered to pay damages of $150,000. -

Question 120:

FILL IN THE BLANK

For the year ending 31 March 20X2, MN made an accounting profit of $120,000. Profit included $8,500 of political donations which are disallowable for tax purposes and $8,000 of income exempt from taxation.

MN has $15,000 of plant and machinery which was acquired on 1 April 20X0 and purchased a new machine costing $25,000 on 1 April 20X1. This new machine is entitled to first year allowances of 100% instead of the usual tax depreciation of 20% reducing balance. All plant and machinery is depreciated in the accounts at 10% on cost.

MN also has a building that cost $120,000 on 1 April 20X0 and is depreciated in the accounts at 4% on a straight line basis. Tax depreciation is calculated at 3% on a straight line basis.

Calculate the taxable profit.

Give your answer to the nearest $.

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-F1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.