IMANET-CMA Exam Details

-

Exam Code

:IMANET-CMA -

Exam Name

:Certified Management Accountant (CMA) -

Certification

:IMANET Certifications -

Vendor

:IMANET -

Total Questions

:1336 Q&As -

Last Updated

:May 24, 2026

IMANET IMANET-CMA Online Questions & Answers

-

Question 231:

Donnelly Corporation manufactures and sells T-shirts imprinted with college names and slogans. Last year. the shirts sold for $7. 50 each, and the variable cost to manufacture them was $2. 25 per unit. The company needed to sell 20.000 shirts to break even. The net income last year was $5,040 Donnelly expectations for me coming year include the following:

The sales price of the T-shirts will be $9

Variable cost to manufacture Will increase by one-third

Fixed costs will increase by 10% The income tax rate of 40% will be unchanged

The selling price that would maintain the same contribution margin rate as last year is?

A. $9.00

B. $8.25

C. $10.00

D. $9.75 -

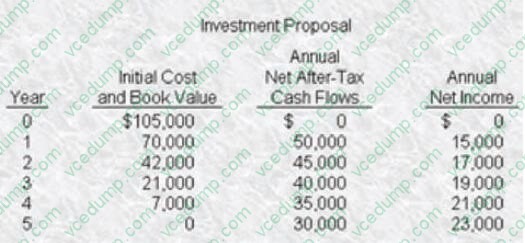

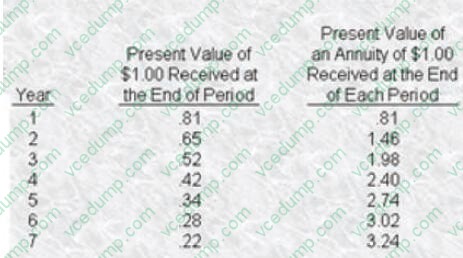

Question 232:

Yipann Corporation is reviewing an investment proposal. The initial cost, as well as other related data for each year. are presented in the schedule below. All cash flows are assumed to take place at the end of the year. The salvage value of the investment at the end of each year is equal to its net book value, and there will be no salvage value at the end of the investments life.

Yipann uses a 24% after4axtargetrate of return for new investment proposals. The discount figures for a 24% rate of return are given.

The average annual cash inflow at which Yipann would be indifferent to the investment (rounded to the nearest dollar) is

A. $21,000

B. $40,000

C. $38,321

D. $46,667 -

Question 233:

Multinational financial management requires that

A. Legal differences be excluded from financial decisions.

B. Political risk be ignored from multinational corporate financial analyses because it cannot be quantified by management.

C. The effect of changing currency values be included in financial analyses.

D. Firms diversity into at least 20 countries to receive a sufficient diversification benefit. -

Question 234:

A firm has $3 million in total assets and $1.65 million in equity. How much of its $500,000 capital budget should be debt- financed to retain the same debt-equity ratio?

A. $50,000

B. $225,000

C. $275,000

D. $450,000 -

Question 235:

Determining the appropriate level of working capital for a firm requires

A. Changing the capital structure and dividend policy of the firm.

B. Maintaining short-term debt at the lowest possible level because it is generally more expensive than long-term debt.

C. Offsetting the benefit of current assets and current liabilities against the probability of technical insolvency.

D. Maintaining a high proportion of liquid assets to total assets in order to maximize the return on total investments. -

Question 236:

The manufacturing concept that relates demand forecasts to specific dates for completion is

A. Master production schedule

B. Materials requirements planning

C. Manufacturing resource planning

D. Bill of materials -

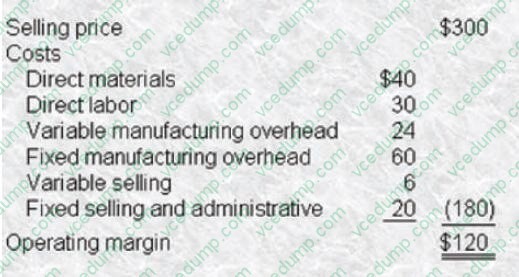

Question 237:

Pontotoc industries manufactures a product that is used as a subcomponent by other manufacturers It has the following price and cost structure

During the next year, sales are expected to be 10.000 units all costs will remain the same except for fixed manufacturing overhead, which will increase 20%. and direct materials. which will increase 10%. The selling price per unit for next year will be $320. Based on this information, Pontotoc's contribution margin for next year will be

A. $1,240,000

B. $1,360,000

C. $2,160,000

D. $2,200,000 -

Question 238:

Simulation, a widely used technique in decision modeling, is a

A. Process of modeling in which real activities are represented in mathematical form.

B. Tool used for allocating scarce resources.

C. Technique used to add random behavior to simulate uncertain.

D. Technique used to map out possible actions given probabilistic events. -

Question 239:

Which of the following is the best example of a variable cost?

A. The corporate president's salary.

B. Cost of raw material.

C. Interest charges.

D. Property taxes. -

Question 240:

Which of the following is exercisable on at the expiration date?

A. Coleopteran.

B. European opinion

C. American option.

D. Put option.

Related Exams:

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only IMANET exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your IMANET-CMA exam preparations and IMANET certification application, do not hesitate to visit our Vcedump.com to find your solutions here.