IMANET-CMA Exam Details

-

Exam Code

:IMANET-CMA -

Exam Name

:Certified Management Accountant (CMA) -

Certification

:IMANET Certifications -

Vendor

:IMANET -

Total Questions

:1336 Q&As -

Last Updated

:May 24, 2026

IMANET IMANET-CMA Online Questions & Answers

-

Question 241:

A company's stock trades rights-on for $50.00 and ex-rights for $48.00. The subscription price for rights holders is $40.00, and four rights are required to purchase one share of stock.The value of a right while the stock is still trading rights-on is

A. $0.40

B. $0.50

C. $1.60

D. $2. 00 -

Question 242:

Logistics Corp. is performing research to determine the feasibility of entering the truck renal industry. The decision to enter the market is most likely to be deterred if

A. Buyer switching costs are high

B. Buyers view the product as differentiated

C. The market is dominated by a small consortium of buyers

D. Buyers enjoy large profit margins -

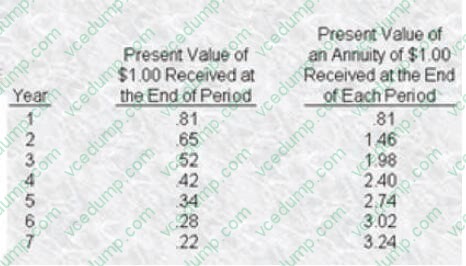

Question 243:

Yipann Corporation is reviewing an investment proposal. The initial cost, as well as other related data for each year. are presented in the schedule below. All cash flows are assumed to take place at the end of the year. The salvage value of the investment at the Yipann uses a 24% after4axtargetrate of return for new investment proposals. The discount figures for a 24% rate of return are given.

The net present value of the investment proposal is

A. $4,600

B. $10,450

C. $(55,280)

D. $115,450 -

Question 244:

Von Stutgatt International's breakeven point is 8,000 racing bicycles and 12,000 5- speed bicycles. If the selling price and variable costs are $570 and $200 for a racer, and $180 and $90 for a 5-speed respectively, what is the weighted-average contribution margin?

A. $100

B. $145

C. $179

D. $202 -

Question 245:

A company has daily cash receipts of $150,000. The treasurer of the company has investigated a lockbox service whereby the bank that offers this service will reduce the company's collection time by four days at a monthly fee of $2,500. money market rates average 4% during the year, the additional annual income (loss) from using the lockbox service would be

A. $6,000

B. $(6,000)

C. $12,000

D. $(12,000) -

Question 246:

The capital budgeting model that is generally considered the best model for long-range decision making is the

A. Payback model.

B. Accounting rate of return model.

C. Unadjusted rate of return model.

D. Discounted cash flow model. -

Question 247:

Post-investment audits?

A. Complete a stage in the capital budgeting process.

B. Sieve as a control mechanism.

C. Allow the outcome of a project to be evaluated as soon as possible

D. Deter managers from proposing profitable investments -

Question 248:

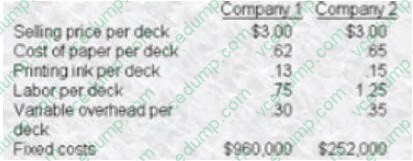

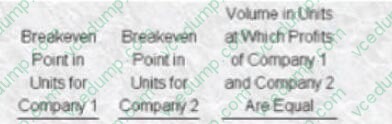

Two compares are expected to have annual sales of I .000.000 decks at playing cards next year Eirne1es for next year are presented below:

Given these data, which of the following responses is rue?

A. 800.000 420.000 1.180,000

B. 800.000 420,000 1000,000

C. 533,334 106. 000 1.000,000

D. 533,334 105. 000 1,180,000 -

Question 249:

The marketing communication mix consists of five types of promotional tools or media. Electronic mail belongs to which class of promotional tools or media?

A. Direct marketing.

B. Advertising.

C. Public relations.

D. Personal selling. -

Question 250:

The technique that incorporates the time value of money by determining the compound interest rate of an investment such that the present value of the after-tax cash inflows over the life of the investment is equal to the initial investment is called the

A. Internal rate of return method.

B. Capital asset pricing model.

C. Profitability index method.

D. Accounting rate of return method.

Related Exams:

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only IMANET exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your IMANET-CMA exam preparations and IMANET certification application, do not hesitate to visit our Vcedump.com to find your solutions here.