CIMA-F1 Exam Details

-

Exam Code

:CIMA-F1 -

Exam Name

:F1 - Financial Reporting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:265 Q&As -

Last Updated

:May 26, 2026

CIMA CIMA-F1 Online Questions & Answers

-

Question 71:

Which of the following is a feature of value added tax (VAT)?

A. Only registered entities can charge VAT on sales or recover VAT paid on purchases.

B. The value of all supplies must be taken into account when determining whether the registration threshold has been exceeded.

C. Entities cannot register for VAT if the value of their taxable supplies is below the registration threshold.

D. Entities that make only standard-rated or zero-rated supplies have their right to recover input tax restricted. -

Question 72:

What is the double-entry for recording the purchase of a non-current asset on credit?

A. Debit Cash, Credit Non-current Assets

B. Debit Non-current Assets, Credit Trade Payables

C. Debit Trade Receivables, Credit Non-current Assets

D. Debit Non-current Assets, Credit Bank -

Question 73:

XYZ Ltd pays rent in advance for 6 months on 1 October 20X6. How should this be accounted for in the financial statements for the year ended 31 December 20X6?

A. As an expense in full for the year.

B. As a prepayment in current assets.

C. As a liability under accruals.

D. As a reduction in retained earnings. -

Question 74:

MNO is a commercial bank. One of MNO's clients is FGH, a trading company which sells goods to PQR.

MNO is asked to draw up an instrument between FGH and PQR in respect of goods sold FGH then asks MNO to sell this instrument on its behalf in the discount market MNO does this and pays the proceeds to FGH.

What source of short-term finance is being described here?

A. Overdraft

B. Bill of exchange

C. Factoring

D. Certificate of deposit -

Question 75:

Country A permits the following deductions in an entity's annual corporate income tax return in relation to entertaining expenses and gifts;

1 Employee entertaining up to a value of $150 a head

2 Entertaining of overseas customers.

3 Individual gifts not to exceed $10 in value

Which THREE of the following actions would be regarded as tax evasion?

A. Delay the next entertainment event for staff until the next financial year so that the $150 limit is not breached.

B. Inflate the number of employees that are recorded as being entertained so that the overall employee entertainment bill falls below $150 a head.

C. Split any gifts made so that any gift does not exceed $10 on an individual basis.

D. Ensure that employees reimburse their employers for any entertaining incurred which exceeds the $150 a head limit

E. Record customers who do not meet the overseas criteria as overseas customers.

F. Deduct all entertaining expenses without any analysis of what the entertaining relates to. -

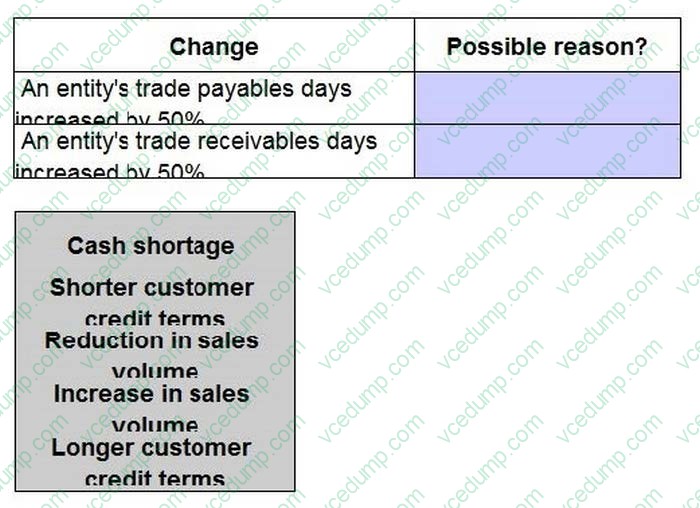

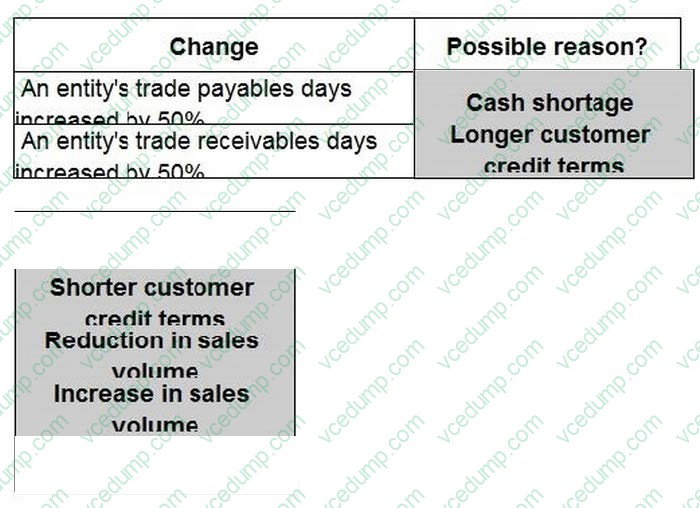

Question 76:

DRAG DROP

Indicate the possible reasons for the changes identified below to working capital ratios by placing the appropriate reason against each change.

Select and Place:

-

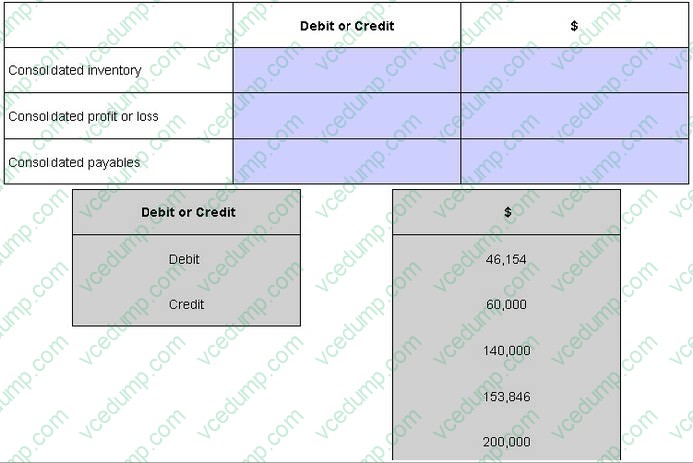

Question 77:

DRAG DROP

MN has a receivables ledger total balance of $160,000, which represents two months' sales. A factor will operate the ledger on a non-recourse basis for a fee of 2.8% of invoiced sales or on a recourse basis of 1% of sales.

It is estimated that using the factor will deter some of the company's customers, and persuade them to buy from a competitor instead. Sales will fall by an estimated $28,000 each year, with a corresponding saving in cost of sales and distribution costs of 40% of this figure.

If the factor is used, administrative savings for both options would be $26,000 each year. Irrecoverable debts are currently 2% of sales.

Select and Place:

-

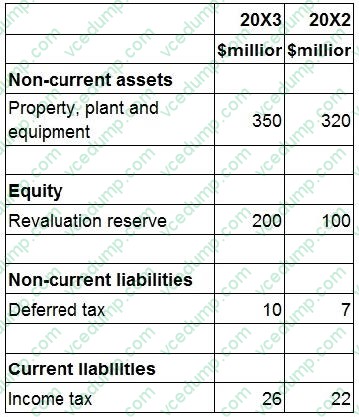

Question 78:

FILL IN THE BLANK

The following information is extracted from the statement of financial position for ZZ at 31 March 20X3:

Included within cost of sales in the statement of profit or loss for the year ended 31 March 20X3 is $20 million relating to the loss on the sale of plant and equipment which had cost $100 million in June 20X1. Depreciation is charged on all plant and equipment at 25% on a straight line basis with a full year's depreciation charged in the year of acquisition and none in the year of sale.

The revaluation reserve relates to the revaluation of ZZ's property.

The total depreciation charge for property, plant and equipment in ZZ's statement of profit of loss for the year ended 31 March 20X3 is $80 million.

The corporate income tax expense in ZZ's statement of profit or loss for year ended 31 March 20X3 is $28 million.

ZZ is preparing its statement of cash flows for the year ended 31 March 20X3. What figure should be included for corporate income tax paid in order to arrive at the net cash flow from operating activities?

Give your answer to the nearest $ million.

-

Question 79:

Which of the following is a type of short-term finance?

A. Trade payables

B. Trade receivables

C. Interest bearing bank deposit

D. Loan repayable in five years -

Question 80:

Which THREE of the following actions, considered in isolation, would increase the working capital cycle of an entity?

A. Remove a prompt payment discount available to customers.

B. Reduce the selling prices charged to customers.

C. Change to a Just-in-Time approach to manage inventory.

D. Take advantage of new bulk purchase discounts available.

E. Take longer to pay suppliers for purchases.

F. Increase the credit period available to customers.

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-F1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.