CIMA-F1 Exam Details

-

Exam Code

:CIMA-F1 -

Exam Name

:F1 - Financial Reporting -

Certification

:CIMA Certifications -

Vendor

:CIMA -

Total Questions

:265 Q&As -

Last Updated

:May 26, 2026

CIMA CIMA-F1 Online Questions & Answers

-

Question 161:

FILL IN THE BLANK

BCD owns an item of plant which cost $20,000 and at the time of purchase was assessed to have a useful economic life of 8 years and a residual value of $2,000

The carrying amount of the plant at 1 January 20X8 is $11,000. On that date BCD's directors estimate that the plant's remaining useful life is now 6 years The residual value remains unchanged at $2,000

What is the depreciation charge for this plant for the year ended 31 December 20X8?

Give your answer to the nearest $.

-

Question 162:

Company Y is using some of the money from a share issue to purchase a new office building. The company is also using some of the money to purchase inventories. Which method of financing is this?

A. Conservative financing

B. Matching financing

C. Aggressive financing -

Question 163:

ST has an asset that was classified as held for sale at 30 June 20X4. The asset's carrying value was $230,000 and its fair value $210,000. The cost of disposal was estimated to be $15,000.

In accordance with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, which of the following values should be used for the asset in the statement of financial position as at 30 June 20X4?

A. $230,000

B. $215,000

C. $210,000

D. $195,000 -

Question 164:

An entity acquires 100% of the equity shares in another entity.

The consideration paid for the shares is less than the fair value of the net assets acquired.

Which of the following is the correct accounting treatment for the difference between the consideration paid and the fair value of the net assets acquired, in accordance with IFRS 3 Business Combinations?

A. Recognise as a gain in the consolidated statement of profit or loss.

B. Recognise as a deferred credit and release to consolidated profit or loss over its useful economic life.

C. Recognise as a deduction from goodwill in the consolidated statement of financial position.

D. Recognise as a gain in the statement of changes in equity. -

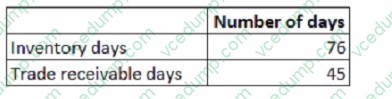

Question 165:

FILL IN THE BLANK

ABC has the following working capital ratios at 31 December 20X2:

During the year ended 31 December 20X4 credit purchases were $1,700,000 and at 31 December 20X4 the outstanding trade payables balance was $340,000

Calculate the working capital cycle for ABC.

Give your answer to the nearest whole number of days and assume there are 365 days in a year.

-

Question 166:

The subsidiary company of Group XY has purchased £150,00 worth of goods its parent company. However the goods purchased have yet to arrive at the subsidiary at the end of the financial year 20X4, meaning there is a disagreement in the current account balances between the parent and subsidiary.

With Group XY looking to produce its CSOFP for the end of the financial year, which of the following statements are true in relation to accounting for this disagreement? Select ALL that apply.

A. The adjustments to resolve this disagreement, need to be accelerated, so they can be included in the consolidation of assets for the CSOFP for 20X4

B. £150,000 worth of inventory will be debited into the subsidiary's inventory account

C. As the goods have not reached the subsidiary by the end of the financial year 20X4, they will be included in the CSOFPfor the next financial year

D. £150,000 worth of inventory will be credited into the subsidiary's inventory account

E. £150,000 will be debited to the payables account of the parent company

F. £150,000 will be credited to the payables account of the subsidiary company

G. £150,000 will be credited into the receivables account of the parent company -

Question 167:

FILL IN THE BLANK

GH's tax liability at 30 June 20X3 in respect of the tax charge on the profits for the year ended 30 June 20X3 is $876,000.

There was an over provision of $105,000 that related to the tax charge on the profits for the year ending 30 June 20X2. What amount should be shown in GH's statement of profit or loss for the year ending 30 June 20X3?

Give your answer to the nearest $.

-

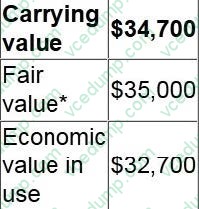

Question 168:

An asset has the following values:

If the asset was sold for its fair value, selling costs of $1,500 would be incurred.

Which of the following is the value of the impairment loss to be recognised for this asset in accordance with IAS 36 Impairment of Assets?

A. $0

B. $300

C. $1,200

D. $2,000 -

Question 169:

Which of the following is not a possible tax rate structure?

A. Progressive

B. Proportional

C. Direct

D. Regressive -

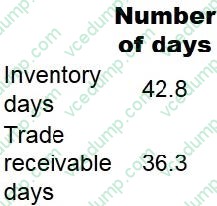

Question 170:

FILL IN THE BLANK

AAA has the following working capital ratios at 30 March 20X4:

During the year ended 30 March 20X4 credit purchases were $3,600 and at 30 March 20X4 the outstanding trade payables amounted to $522.

The year ended 30 March 20X4 was not a leap year.

Calculate the working capital cycle for AAA.

Give your answer to one decimal place.

Related Exams:

-

CIMA-BA1

BA1 - Fundamentals of Business Economics -

CIMA-BA2

BA2 - Fundamentals of Management Accounting -

CIMA-BA3

BA3 - Fundamentals of Financial Accounting -

CIMA-BA4

BA4 - Fundamentals of Ethics, Corporate Governance and Business Law -

CIMA-CS3

CS3 - Strategic Case Study 2021 -

CIMA-E1

E1 - Managing Finance in a Digital World -

CIMA-E2

E2 - Managing Performance -

CIMA-E3

E3 - Strategic Management -

CIMA-F1

F1 - Financial Reporting -

CIMA-F2

F2 - Advanced Financial Reporting

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only CIMA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CIMA-F1 exam preparations and CIMA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.