Exam Details

Exam Code

:CCRAExam Name

:Certified Credit Research AnalystCertification

:AIWMI CertificationsVendor

:AIWMITotal Questions

:84 Q&AsLast Updated

:Jul 04, 2025

AIWMI AIWMI Certifications CCRA Questions & Answers

-

Question 51:

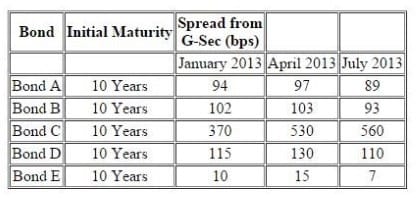

The following information pertains to bonds: Further following information is available about a particular bond `Bond F'

There is a 10.25% risky bond with a maturity of 2.25% year(s) its current price is INR105.31, which corresponds to YTM of 9.22%. The following are the benchmark YTMs.

Assuming the G-Sec has not changed from the time January 2013 to April 2013, what can you predict about the changes bond price and change in issues borrowing rates:

A. Decrease and Increase

B. Increase and Increase

C. Decrease and Decrease

D. Increase and Decrease

-

Question 52:

The following information pertains to bonds:

Further following information is available about a particular bond `Bond F'

There is a 10.25% risky bond with a maturity of 2.25% year(s) its current price is INR105.31, which corresponds to YTM of 9.22%. The following are the benchmark YTMs.

Following are the relevance of Industry Analysis:

Statement 1: Evaluating Industry risk is the first and foremost step for top down approach of analysis.

Statement 2: Industry Analysis is relevant for analyzing the industry life cycle, which is highly important

from the perspective of an investor or lender.

State which is/are correct?

A. Both are incorrect

B. Both are correct

C. Only Statement 2 is correct

D. Only Statement 1 is correct

-

Question 53:

The following information pertains to bonds:

Further following information is available about a particular bond `Bond F'

There is a 10.25% risky bond with a maturity of 2.25% year(s) its current price is INR105.31, which corresponds to YTM of 9.22%. The following are the benchmark YTMs.

Compute interpolated spread for Bond F based on the information provided in the vignette:

A. 1.64%

B. 0.43%

C. 0.61%

D. 1.46%

-

Question 54:

The following information pertains to bonds:

Further following information is available about a particular bond `Bond F'

There is a 10.25% risky bond with a maturity of 2.25% year(s) its current price is INR105.31, which corresponds to YTM of 9.22%. The following are the benchmark YTMs.

From the time January 2013 to April 2013, what can you predict about the market conditions, assuming the G-Sec has not changed?

A. There has been credit spread compression, which means the spreads have declines, which can be lead indicator of oncoming economy stress.

B. There has been widening of credit spread, which means the spreads have increased, which can be lead indicator of oncoming economy stress.

C. There has been widening of credit spread, which means the spreads have increased, which can be lead indicator of oncoming economy stress.

D. There has been credit spread compression, which means the spreads have declines, which can be lead indicator of oncoming economy boom.

-

Question 55:

Satish Dhawan, a veteran fixed income trader is conducting interviews for the post of a junior fixed income trader. He interviewed four candidates Adam, Balkrishnan, Catherine and Deepak and following are the answers to his questions. Q-1: Tell something about Option Adjusted Spread

Adam: OAS is applicable only to bond which do not have any options attached to it. It is for the plain bonds.

Balkishna: In bonds with embedded options, AS reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

Catherine: Sincespreads are calculated to know the level of credit risk in the bound, OAS is difference between in the Z spread and price of a call option for a callable bond.

Deepark: For callable bond OAS will be lower than Z Spread.

Q-2: This is a spread that must be added to the benchmark zero rate curve in a parallel shift so that the sum of the risky bond's discounted cash flows equals its current market price. Which Spread I am talking about?

Adam: Z Spread

Balkrishna: Nominal Spread Catherine: Option Adjusted Spread Deepark: Asset Swap Spread Q-3: What do you know about Interpolated spread and yield spread?

Adam: Yield spread is the difference between the YTM of a risky bond and the YTM of an on-the-run treasury benchmark bond whose maturity is closest, but not identical to that of risky bond. Interpolated spread is the spread between the YTM of risky bond and the YTM of same maturity treasury benchmark, which is interpolated from the two nearest on-the-run treasury securities.

Balkrishna: Interpolated spread is preferred to yield spread because the latter has the maturity mismatch, which leads to error if the yield curve is not flat and the benchmark security changes over time, leading to inconsistency.

Catherine: Interpolated spread takes account the shape of the benchmark yield curve and therefore better than yield spread.

Deepak: Both Interpolated Spread and Yield Spread rely on YTM which suffers from drawbacks and inconsistencies such as the assumption of flat yield curve and reinvestment at YTM itself.

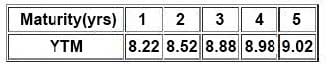

Then Satish gave following information related to the benchmark YTMs:

Who amongst the four candidates is correct regarding OAS?

A. Only Catherine

B. Only Deepak

C. Only Adam and Catherine

D. Only Deepak and Catherine

-

Question 56:

Satish Dhawan, a veteran fixed income trader is conducting interviews for the post of a junior fixed income trader. He interviewed four candidates Adam, Balkrishnan, Catherine and Deepak and following are the answers to his questions. Q-1: Tell something about Option Adjusted Spread

Adam: OAS is applicable only to bond which do not have any options attached to it. It is for the plain bonds.

Balkishna: In bonds with embedded options, AS reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

Catherine: Sincespreads are calculated to know the level of credit risk in the bound, OAS is difference between in the Z spread and price of a call option for a callable bond.

Deepark: For callable bond OAS will be lower than Z Spread.

Q-2: This is a spread that must be added to the benchmark zero rate curve in a parallel shift so that the sum of the risky bond's discounted cash flows equals its current market price. Which Spread I am talking about?

Adam: Z Spread

Balkrishna: Nominal Spread Catherine: Option Adjusted Spread Deepark: Asset Swap Spread

Q-3: What do you know about Interpolated spread and yield spread?

Adam: Yield spread is the difference between the YTM of a risky bond and the YTM of an on-the-run treasury benchmark bond whose maturity is closest, but not identical to that of risky bond. Interpolated spread is the spread between the YTM of risky bond and the YTM of same maturity treasury benchmark, which is interpolated from the two nearest on-the-run treasury securities.

Balkrishna: Interpolated spread is preferred to yield spread because the latter has the maturity mismatch, which leads to error if the yield curve is not flat and the benchmark security changes over time, leading to inconsistency.

Catherine: Interpolated spread takes account the shape of the benchmark yield curve and therefore better than yield spread.

Deepak: Both Interpolated Spread and Yield Spread rely on YTM which suffers from drawbacks and inconsistencies such as the assumption of flat yield curve and reinvestment at YTM itself.

Then Satish gave following information related to the benchmark YTMs:

There is an 8.75% risky bond with a maturity of 2.75% year(s). Its current price is INR102.31, which corresponds to YTM of 8.52%. Compute Yield Spread from the information provided in the vignette:

A. 0.13%

B. 0.00%

C. 0.36%

D. 0.27%

-

Question 57:

Satish Dhawan, a veteran fixed income trader is conducting interviews for the post of a junior fixed income trader. He interviewed four candidates Adam, Balkrishnan, Catherine and Deepak and following are the answers to his questions. Q-1: Tell something about Option Adjusted Spread

Adam: OAS is applicable only to bond which do not have any options attached to it. It is for the plain bonds.

Balkishna: In bonds with embedded options, AS reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

Catherine: Sincespreads are calculated to know the level of credit risk in the bound, OAS is difference between in the Z spread and price of a call option for a callable bond.

Deepark: For callable bond OAS will be lower than Z Spread.

Q-2: This is a spread that must be added to the benchmark zero rate curve in a parallel shift so that the sum of the risky bond's discounted cash flows equals its current market price. Which Spread I am talking about?

Adam: Z Spread

Balkrishna: Nominal Spread Catherine: Option Adjusted Spread Deepark: Asset Swap Spread

Q-3: What do you know about Interpolated spread and yield spread?

Adam: Yield spread is the difference between the YTM of a risky bond and the YTM of an on-the-run treasury benchmark bond whose maturity is closest, but not identical to that of risky bond. Interpolated spread is the spread between the YTM of risky bond and the YTM of same maturity treasury benchmark, which is interpolated from the two nearest on-the-run treasury securities.

Balkrishna: Interpolated spread is preferred to yield spread because the latter has the maturity mismatch, which leads to error if the yield curve is not flat and the benchmark security changes over time, leading to inconsistency.

Catherine: Interpolated spread takes account the shape of the benchmark yield curve and therefore better than yield spread.

Deepak: Both Interpolated Spread and Yield Spread rely on YTM which suffers from drawbacks and inconsistencies such as the assumption of flat yield curve and reinvestment at YTM itself.

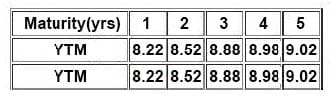

Then Satish gave following information related to the benchmark YTMs:

An investor decides to invest in the bond futures and has an outlook that the term structure curve would steepen. What should be his trading strategy?

A. Sell futures on short-maturity underlying, Buy futures on long-maturity underlying

B. Buy futures on short-maturity underlying, Buy futures on long-maturity underlying and Sell futures on middle-maturity underlying

C. Buy futures on short-maturity underlying, Sell futures on long-maturity underlying.

D. Sell futures on short-maturity underlying, Sell futures on long-maturity underlying and Buy futures on middle-maturity underlying.

-

Question 58:

Satish Dhawan, a veteran fixed income trader is conducting interviews for the post of a junior fixed income trader. He interviewed four candidates Adam, Balkrishnan, Catherine and Deepak and following are the answers to his questions. Q-1: Tell something about Option Adjusted Spread

Adam: OAS is applicable only to bond which do not have any options attached to it. It is for the plain bonds.

Balkishna: In bonds with embedded options, AS reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

Catherine: Sincespreads are calculated to know the level of credit risk in the bound, OAS is difference between in the Z spread and price of a call option for a callable bond.

Deepark: For callable bond OAS will be lower than Z Spread.

Q-2: This is a spread that must be added to the benchmark zero rate curve in a parallel shift so that the sum of the risky bond's discounted cash flows equals its current market price. Which Spread I am talking about?

Adam: Z Spread

Balkrishna: Nominal Spread Catherine: Option Adjusted Spread Deepark: Asset Swap Spread

Q-3: What do you know about Interpolated spread and yield spread?

Adam: Yield spread is the difference between the YTM of a risky bond and the YTM of an on-the-run treasury benchmark bond whose maturity is closest, but not identical to that of risky bond. Interpolated spread is the spread between the YTM of risky bond and the YTM of same maturity treasury benchmark, which is interpolated from the two nearest on-the-run treasury securities.

Balkrishna: Interpolated spread is preferred to yield spread because the latter has the maturity mismatch, which leads to error if the yield curve is not flat and the benchmark security changes over time, leading to inconsistency.

Catherine: Interpolated spread takes account the shape of the benchmark yield curve and therefore better than yield spread.

Deepak: Both Interpolated Spread and Yield Spread rely on YTM which suffers from drawbacks and inconsistencies such as the assumption of flat yield curve and reinvestment at YTM itself.

Then Satish gave following information related to the benchmark YTMs:

There is a 10.25% risky bond with a maturity of 4.75 year(s). Its current price is INR105.31, which corresponds to YTM of 9.22%. Compute Interpolated Spread from the information provided in the vignette:

A. 0.20%

B. 0.21%

C. 0.24%

D. 0.22%

-

Question 59:

Satish Dhawan, a veteran fixed income trader is conducting interviews for the post of a junior fixed income trader. He interviewed four candidates Adam, Balkrishnan, Catherine and Deepak and following are the answers to his questions. Q-1: Tell something about Option Adjusted Spread

Adam: OAS is applicable only to bond which do not have any options attached to it. It is for the plain bonds.

Balkishna: In bonds with embedded options, AS reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

Catherine: Sincespreads are calculated to know the level of credit risk in the bound, OAS is difference between in the Z spread and price of a call option for a callable bond.

Deepark: For callable bond OAS will be lower than Z Spread.

Q-2: This is a spread that must be added to the benchmark zero rate curve in a parallel shift so that the sum of the risky bond's discounted cash flows equals its current market price. Which Spread I am talking about?

Adam: Z Spread

Balkrishna: Nominal Spread Catherine: Option Adjusted Spread Deepark: Asset Swap Spread

Q-3: What do you know about Interpolated spread and yield spread?

Adam: Yield spread is the difference between the YTM of a risky bond and the YTM of an on-the-run treasury benchmark bond whose maturity is closest, but not identical to that of risky bond. Interpolated spread is the spread between the YTM of risky bond and the YTM of same maturity treasury benchmark, which is interpolated from the two nearest on-the-run treasury securities.

Balkrishna: Interpolated spread is preferred to yield spread because the latter has the maturity mismatch, which leads to error if the yield curve is not flat and the benchmark security changes over time, leading to inconsistency.

Catherine: Interpolated spread takes account the shape of the benchmark yield curve and therefore better than yield spread.

Deepak: Both Interpolated Spread and Yield Spread rely on YTM which suffers from drawbacks and inconsistencies such as the assumption of flat yield curve and reinvestment at YTM itself.

Then Satish gave following information related to the benchmark YTMs:

Which of the modified statement of Balkrishna will be a correct statement?

A. In bonds with embedded options, Nominal Spread reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

B. In bonds with embedded options, spread reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

C. None of the three.

D. In bonds with embedded options, Z Spread reflects not only the credit risk but also reflects prepayment risk over and above the benchmark.

-

Question 60:

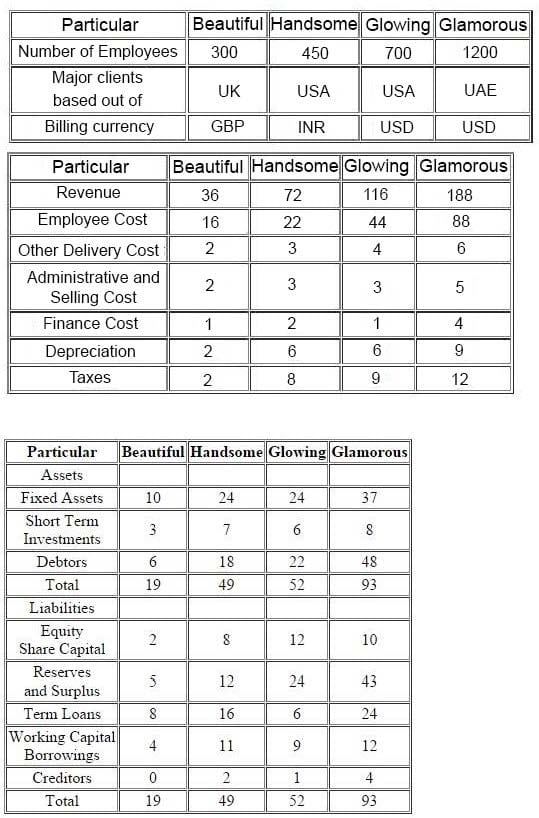

"Following four entities operate in the Indian IT and BPO space. They all are into same segment of providing off-shore analytical services. They all operate on the labour cost-arbitrage in India and the countries of their clients. Following information pertains for the year ended March 31, 2013.

The year FY13, was typically a good year for Indian IT companies. For FY14, the economic analysts have given following predictions about the IT Industry:

A. It is expected that INR will appreciate sharply against other USD.

B. Given high inflation and attrition in IT Industry in India, the wages of IT sector employees will increase more sharply than Inflation and general wage rise in country.

C. US Congress will be passing a bill which restricts the outsourcing to third world countries like India. While analyzing the four entities, you come across following findings related to Glowing:

Glowing is promoted by Mr.M R Bhutta, who has earlier promoted two other business ventures, He started with ABC Entertainment Ltd in 1996 and was promoter and MD of the company. ABC was a listed entity and its share price had sharp movements at the time of stock market scam in late 1990s. In 1999, Mr. Bhutta sold his entire stake and resigned from the post of MD. The stock price declined by about 90% in coming days and has never recovered. Later on in 2003, Mr. Bhutta again promoted a new business, Klear Publications Ltd (KCL) an in the business of magazine publication. The entity had come out with a successful IPO and raised money from public. Thereafter it ran into troubles and reported losses. In 2009, Mr. Bhutta went on to exit this business as well by selling stake to other promoter(s). There have been reports in both instances with allegations that promoters have siphoned off money from listed entities to other group entities, however, nothing has been proved in any court."

Based on your findings in the case of Glowing, how will you handle the same as a credit rating analyst:

A. Be more cautious and skeptical on any information received from Glowing and give negative marks in management risk and use it as an overriding factor to lower the credit ratings.

B. Any of the three.

C. Deny taking up assignment for Glowing.

D. One needs to check only the corporate governance aspect of the Glowing and the past same should not have any bearing on Glowing.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AIWMI exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CCRA exam preparations and AIWMI certification application, do not hesitate to visit our Vcedump.com to find your solutions here.