IMANET-CMA Exam Details

-

Exam Code

:IMANET-CMA -

Exam Name

:Certified Management Accountant (CMA) -

Certification

:IMANET Certifications -

Vendor

:IMANET -

Total Questions

:1336 Q&As -

Last Updated

:Jun 01, 2026

IMANET IMANET-CMA Online Questions & Answers

-

Question 481:

In evaluating a capital budget project, the use of the net present value (NPV) model is generally not affected by the

A. Method of funding the project.

B. Initial cost of the project.

C. Amount of added working capital needed for operations during the term of the project.

D. Project's salvage value. -

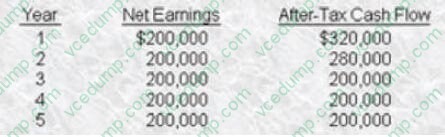

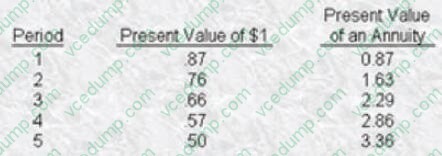

Question 482:

Tonya, Inc. has a cost of capital of 15% and is considering the acquisition of a new machine that costs $800,000 and has a useful life of 5 years. Tonya projects that earnings and cash flow will increase as follows:

Interest rate factors at 15% are as follows:

What is the profitability index for the investment?

A. 0.05

B. 0.96

C. 1.05

D. 1.25 -

Question 483:

The length of time required to recover the initial cash outlay of a capital project is determined by using the

A. Discounted cash flow method.

B. Payback method.

C. Weighted net present value method.

D. Net present value method. -

Question 484:

Independent harms that agree to integrate their operations to achieve bring and selling power are most likely to operate in which type of vertical marketing system (VMS)?

A. Contractual.

B. Administered.

C. Corporate.

D. Conventional channel. -

Question 485:

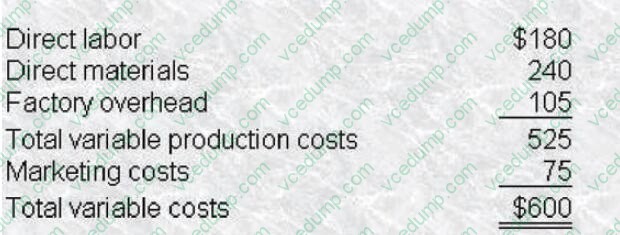

Madengrad Company manufactures a single electronic product called Precisionmix. This unit is a batch-density monitoring device attached to large industrial mixing machines used in flour, rubber, petroleum, and chemical manufacturing. Precisionmix sells for $900 per unit. The following variable costs are incurred to produce each Precisionmix device:

Madengrad's income tax rate is4O%, and annual fixed costs are $6,600,000. Except for an operating loss incurred in the year of incorporation, the firm has been profitable over the last 5 years.The annual sales volume required for Madengrad Company to break even is

A. 22,000 units.

B. 11,000units.

C. 8,400 units.

D. 13,888 units. -

Question 486:

Product A accounts for 75% of a company's total sales revenue and has a variable cost equal to 60% of its selling price. Product B accounts for 25% of total sales revenue and has a variable cost equal to 85% of its selling price. What is the breakeven point given fixed costs of $150,000?

A. $375,000

B. $444,444

C. $500,000

D. $545,455 -

Question 487:

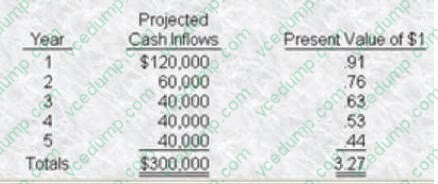

The Keego Company is planning a $200,000 equipment investment which has an estimated 5-year life with no estimated salvage value. The company has projected the following annual cash flows for the investment.

The net present value for the investment is

A. $18,800

B. $218,800

C. $100,000

D. $91,743 -

Question 488:

You have just purchased a 15-year, $ 1.000 par value bond. The coupon rate on this bond is 9% annually, with interest being paid each 6 months. If you expect to earn a 12% nominal rate of return on this bond, how much did you pay for it?

A. $642. 76

B. $793. 43

C. $875. 38

D. $950.75 -

Question 489:

Which attribute of the product mix corresponds to the number of product lines?

A. Depth

B. Consistency

C. Width

D. Length -

Question 490:

A manufacturer produces a product that sells for $10 per unit. Variable costs per unit are $6 and total fixed costs are $1 2. 000. At this selling price, the company earns a profit equal to 10% of total dollar sales By reducing its selling price to $9 per unit, the manufacturer can increase its unit sales volume by 25%. Assume that there are no taxes and that total fixed costs and variable costs per unit remain unchanged It the selling price were reduced to $9 per unit, the profit would be

A. $3,000

B. $4,000

C. $5,000

D. $6,000

Related Exams:

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only IMANET exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your IMANET-CMA exam preparations and IMANET certification application, do not hesitate to visit our Vcedump.com to find your solutions here.