2016-FRR Exam Details

-

Exam Code

:2016-FRR -

Exam Name

:Financial Risk and Regulation (FRR) Series -

Certification

:GARP Certifications -

Vendor

:GARP -

Total Questions

:342 Q&As -

Last Updated

:Jun 27, 2026

GARP 2016-FRR Online Questions & Answers

-

Question 181:

Alpha Bank determined that Delta Industrial Machinery Corporation has 2% change of default on a one- year no-payment of USD $1 million, including interest and principal repayment. The bank charges 3% interest rate spread to firms in the machinery industry, and the risk-free interest rate is 6%. Alpha Bank receives both interest and principal payments once at the end the year. Delta can only default at the end of the year. If Delta defaults, the bank expects to lose 50% of its promised payment. What interest rate should Alpha Bank charge on the no-payment loan to Delta Industrial Machinery Corporation?

A. 8%

B. 9%

C. 10%

D. 12% -

Question 182:

Rising TED spread is typically a sign of increase in what type of risk among large banks?

I. Credit risk

II. Market risk

III. Liquidity risk

IV.

Operational risk

A. I only

B. II only

C. I and IV

D. I, II, and III

I. Credit risk II. Market risk III. Liquidity risk IV. Operational risk -

Question 183:

How could a bank's hedging activities with futures contracts expose it to liquidity risk?

A. The futures hedge may not work due to the widening of basis which could result in a loss for the bank.

B. Prices may move such that a loss results on the hedge.

C. Since futures require margins which are settled every day, the bank could find itself scrambling for funds.

D. The bank could get exposed to liquidity risk since futures trade on an exchange. -

Question 184:

BetaFin, a financial services firm, does not have retail branches, but has fixed income, equity, and asset management divisions. Which one of the four following risk and control self-assessment (RCSA) methods fits the firm's operational risk framework the best?

A. RCSA questionnaire approach

B. RCSA workshop approach

C. RCSA loss data approach

D. RCSA scenario analysis approach -

Question 185:

In analyzing market option pricing dynamics, a risk manager evaluates option value changes throughout the entire trading day. Which of the following factors would most likely affect foreign exchange option values?

I. Change in the value of the underlying

II. Change in the perception of future volatility

III. Change in interest rates

IV.

Passage of time

A. I, II

B. I, II, III

C. II, III

D. I, II, III, IV

I. Change in the value of the underlying II. Change in the perception of future volatility III. Change in interest rates IV. Passage of time -

Question 186:

A bank has a large number of auto loans and would prefer to sell them to raise cash for more funding. However, selling individual auto loans is difficult. What could the bank do?

A. Package the loans into a securitized vehicle and sell the low risk portion of the portfolio.

B. Obtain a stronger credit rating so that the bank could borrow at a cheaper rate.

C. Set up a marketing team to sell individual loans to investors.

D. Merge with another bank. -

Question 187:

To manage its credit portfolio, Beta Bank can directly sell the following portfolio elements:

I. Bonds

II. Marketable loans

III.

Credit card loans

A. I

B. II

C. I, II

D. II, III

I. Bonds II. Marketable loans III. Credit card loans -

Question 188:

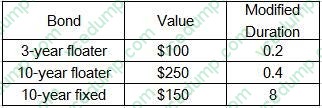

A portfolio consists of two floating rate bonds and one fixed rate bond.

Based on the information below, modified duration of this portfolio is

A. 2.64

B. 3.00

C. 4.28

D. 4.44 -

Question 189:

When operating in a heavily traded currency, a commercial and retail bank's treasury is likely to focus on cover operations. Which one of the following four commercial and retails treasury's operations is known as a cover operation?

A. Ensuring that the risks generated by the bank's business are mitigated in the market.

B. Managing the net interest rate risk in the banking book directly with market counterparties by operating a derivatives trading desk.

C. Effectively transferring the interest rate risk in the banking book to the investment bank at a fair transfer price.

D. Mitigating liquidity risk, or effectively managing the balance sheet and its funding. -

Question 190:

Except for the credit quality of the Credit Default Swap protection seller, the following relationship correctly approximates the yield on a risk-free instrument:

A. Bond + CDS

B. Bond + CDS + Market Spread

C. Bond - CDS

D. Bond - CDS - Market spread

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only GARP exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your 2016-FRR exam preparations and GARP certification application, do not hesitate to visit our Vcedump.com to find your solutions here.